Question

Triangular Arbitrage 1. You are given the following exchange rates, what is the implied rate for USD/EUR? S(t,EUR/GBP) = 1.1500, S(t,USD/GBP) = 1.3900 2. You

Triangular Arbitrage

1. You are given the following exchange rates, what is the implied rate for USD/EUR? S(t,EUR/GBP) = 1.1500, S(t,USD/GBP) = 1.3900

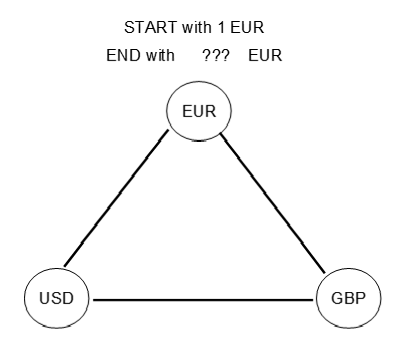

2. You are given the same rates as above. Another FX dealer offers you a rate for USD/EUR of 1.19. Is there a profit opportunity? Using the following figure, indicate all necessary transactions to answer this question. Assume for simplicity you have EUR 1 to invest. What is your return in %?

3. If you had GBP 1 to invest (instead of EUR 1 as under b.), would your relative return (in %) be different compared to b.?

START with 1 EUR END with??? EUR EUR USD GBP START with 1 EUR END with??? EUR EUR USD GBP

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started