Answered step by step

Verified Expert Solution

Question

1 Approved Answer

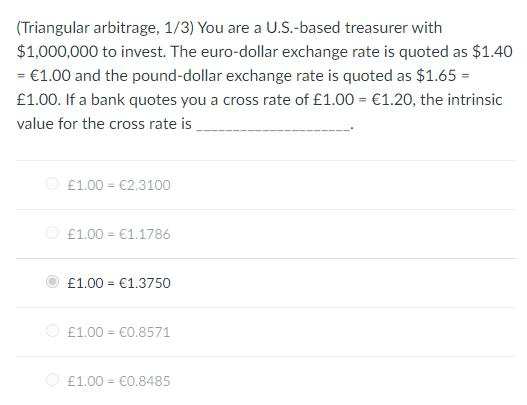

(Triangular arbitrage, 1/3) You are a U.S.-based treasurer with $1,000,000 to invest. The euro-dollar exchange rate is quoted as $1.40 = 1.00 and the

(Triangular arbitrage, 1/3) You are a U.S.-based treasurer with $1,000,000 to invest. The euro-dollar exchange rate is quoted as $1.40 = 1.00 and the pound-dollar exchange rate is quoted as $1.65 = 1.00. If a bank quotes you a cross rate of 1.00 = 1.20, the intrinsic value for the cross rate is 1.00 2.3100 1.00 1.1786 1.00 1.3750 = 1.00 0.8571 1.00 0.8485

Step by Step Solution

There are 3 Steps involved in it

Step: 1

I cannot see the image content If you want to know the intrinsic value calculation for ...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Fundamentals of corporate finance

Authors: Stephen Ross, Randolph Westerfield, Bradford Jordan

9th edition

978-0077459451, 77459458, 978-1259027628, 1259027627, 978-0073382395