Answered step by step

Verified Expert Solution

Question

1 Approved Answer

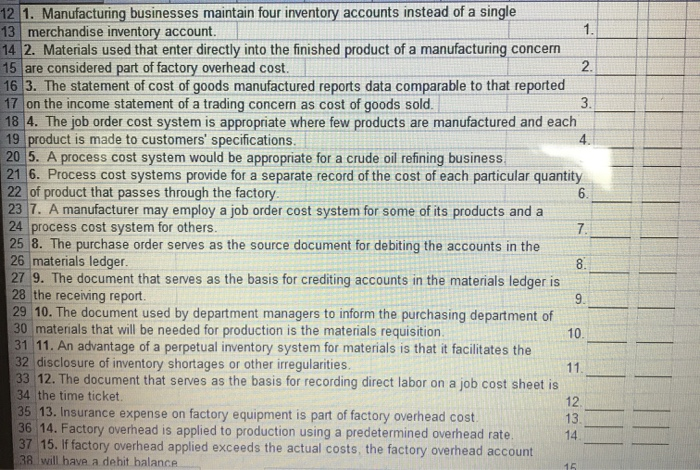

true or false? 12 1. Manufacturing businesses maintain four inventory accounts instead of a single 13 merchandise inventory account. 14 2. Materials used that enter

true or false?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Cornerstones of Financial and Managerial Accounting

Authors: Rich Jones, Mowen, Hansen, Heitger

1st Edition

9780538751292, 324787359, 538751290, 978-0324787351