Question

Tutorial Four (Week beginning Monday 25 th October 2021) (i) You are managing a separate portfolio dedicated to your retirement income. You do not wish

Tutorial Four (Week beginning Monday 25 th October 2021) (i) You are managing a separate portfolio dedicated to your retirement income. You do not wish to take excessive risk, and would prefer to limit the downside. What common option strategy would you enter into? (ii) Under what circumstances would an investor enter into (i) a covered call and (ii) a protective put? Describe the structure of both strategies and draw the associated payoff diagrams for both strategies. (iii) Explain why a butterfly spread option strategy is an appropriate strategy for a trader who feels significant price movements are unlikely. Describe the components of such a strategy and draw the associated payoff diagram. (iv) Apple is currently trading at $26. You expect that prices will increase but not rise above $28 per share. Options on Apple with strikes of $22.50, $25.00, $27.50, and $30 are available. What options portfolio would you construct from these options to incorporate your views? (v) A trader enters into a short position in a strangle options-based trading strategy What are the option components of this strategy? In entering this strategy what are the traders expectations about market conditions? If in contrast the trader enters into a short position in a strip what are the traders expectations about market conditions? How do expectations about market conditions differ in comparison to expectations for the strangle strategy? (vii) What gross payoff profile is obtained if an investor shorts a covered call and goes long a protective put? Assume a common exercise price for all options. What is the investors view of the movement of the share price if he/she holds this position? (January 2021, question 3d (25marks

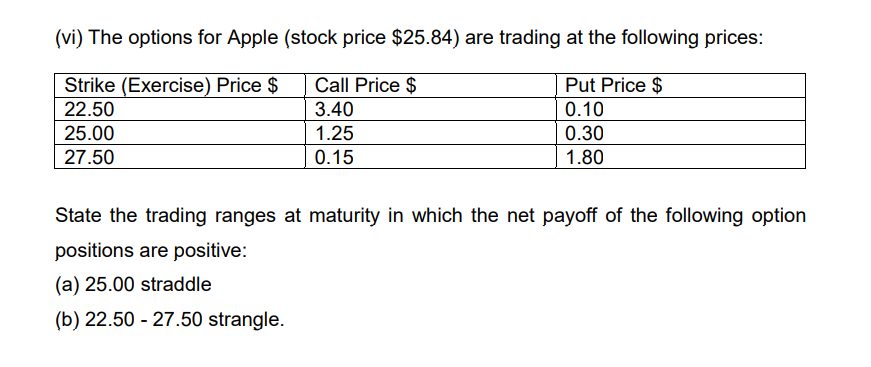

(vi) The options for Apple (stock price $25.84) are trading at the following prices: Strike (Exercise) Price $ 22.50 25.00 27.50 Call Price $ 3.40 1.25 0.15 Put Price $ 0.10 0.30 1.80 State the trading ranges at maturity in which the net payoff of the following option positions are positive: (a) 25.00 straddle (b) 22.50 - 27.50 strangle. (vi) The options for Apple (stock price $25.84) are trading at the following prices: Strike (Exercise) Price $ 22.50 25.00 27.50 Call Price $ 3.40 1.25 0.15 Put Price $ 0.10 0.30 1.80 State the trading ranges at maturity in which the net payoff of the following option positions are positive: (a) 25.00 straddle (b) 22.50 - 27.50 strangle

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Fiduciary Finance Investment Funds And The Crisis In Financial Markets

Authors: Martin Gold

1st Edition

1848448953, 9781848448957