Answered step by step

Verified Expert Solution

Question

1 Approved Answer

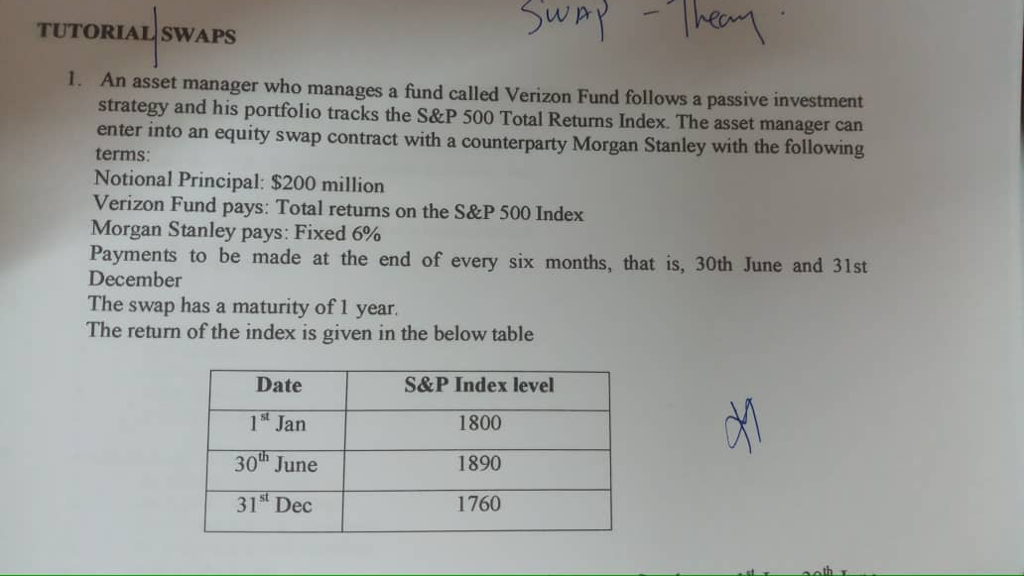

TUTORIAL SWAPS 1. An asset manager who manages a fund called Verizon Fund follows a passive investment strategy and his portfolio tracks the S&P 500

TUTORIAL SWAPS 1. An asset manager who manages a fund called Verizon Fund follows a passive investment strategy and his portfolio tracks the S&P 500 Total Returns Index. The asset manager can enter into an equity swap contract with a counterparty Morgan Stanley with the following terms Notional Principal: $200 million Verizon Fund pays: Total retums on the S&P 500 Index Morgan Stanley pays: Fixed 690 Payments to be made at the end of every six months, that is, 30th June and 31st December The swap has a maturity of 1 year The return of the index is given in the below table Date Jan 30t" June 31st Dec S&P Index level 1800 1890 1760 1

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Entrepreneurial Finance

Authors: Philip J. Adelman, Alan M. Marks

4th Edition

0132434792, 9780132434799