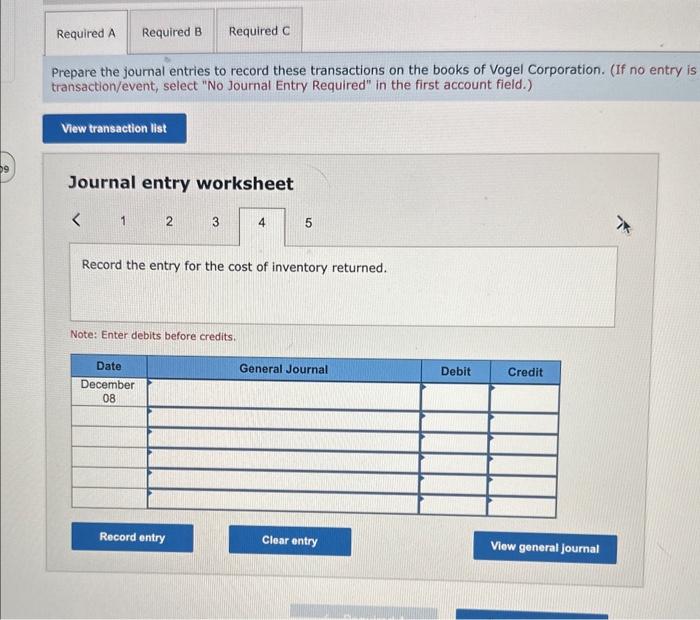

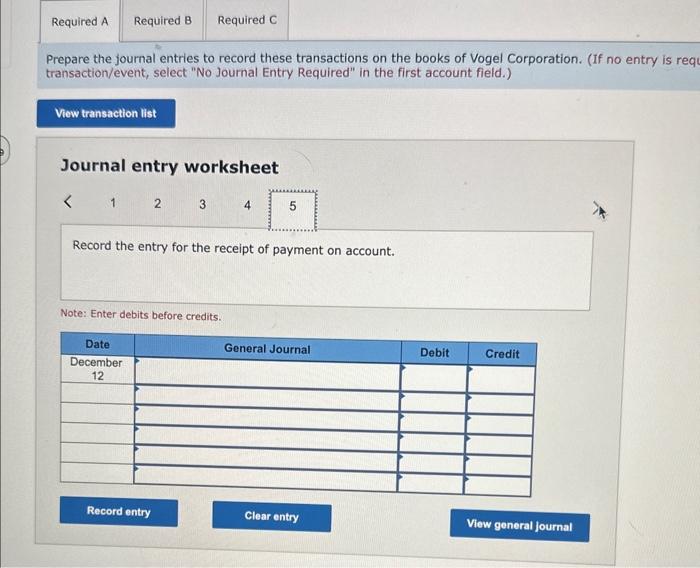

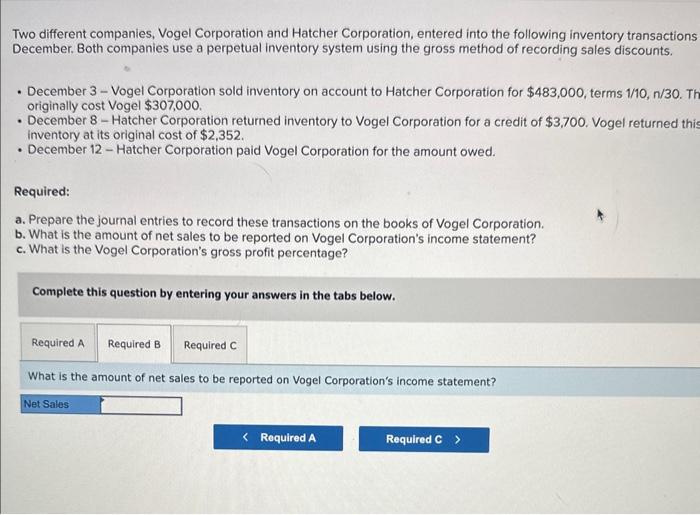

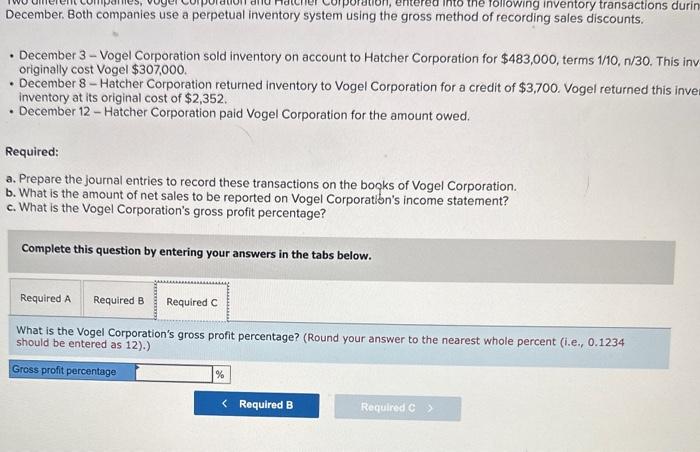

Two different companies, Vogel Corporation and Hatcher Corporation, entered into the following inventory transactions during December. Both companies use a perpetual inventory system using the gross method of recording sales discounts. - December 3 - Vogel Corporation sold inventory on account to Hatcher Corporation for $483,000, terms 1/10, n/30. This inventory originally cost Vogel $307,000. - December 8 - Hatcher Corporation returned inventory to Vogel Corporation for a credit of $3,700. Vogel returned this inventory to inventory at its original cost of $2,352. - December 12 - Hatcher Corporation paid Vogel Corporation for the amount owed. Required: a. Prepare the journal entries to record these transactions on the books of Vogel Corporation. b. What is the amount of net sales to be reported on Vogel Corporation's income statement? c. What is the Vogel Corporation's gross profit percentage? Complete this question by entering your answers in the tabs below. Prepare the journal entries to record these transactions on the books of vogel Corporation. (If no entry is required for a transaction/event, select "No Journal Entry Required" in the first account field.) Prepare the journal entries to record these transactions on the books of Vogel Corporation. (If no ent transaction/event, select "No Journal Entry Required" in the first account field.) Journal entry worksheet 5 Record the entry for sale of inventory on account. Note: Enter debits before credits. Prepare the journal entries to record these transactions on the books of Vogel Corporation. (If no entry is transaction/event, select "No Journal Entry Required" in the first account field.) Journal entry worksheet Record the entry for cost of inventory sold on account. Note: Enter debits before credits. Prepare the journal entries to record these transactions on the books of Vogel Corporation. (If no entry is require transaction/event, select "No Journal Entry Required" in the first account field.) Journal entry worksheet Record the entry for return of inventory sold on account. Note: Enter debits before credits. Prepare the joumal entries to record these transactions on the books of Vogel Corporation. (If no entry is transaction/event, select "No Journal Entry Required" in the first account field.) Journal entry worksheet Record the entry for the cost of inventory returned. Note: Enter debits before credits. Prepare the journal entries to record these transactions on the books of Vogel Corporation. (If no entry is req transaction/event, select "No Journal Entry Required" in the first account field.) Journal entry worksheet Record the entry for the receipt of payment on account. Note: Enter debits before credits. Two different companies, Vogel Corporation and Hatcher Corporation, entered into the following inventory transactions December. Both companies use a perpetual inventory system using the gross method of recording sales discounts. - December 3 - Vogel Corporation sold inventory on account to Hatcher Corporation for $483,000, terms 1/10,n/30. Ti originally cost Vogel $307,000. - December 8 - Hatcher Corporation returned inventory to Vogel Corporation for a credit of $3,700. Vogel returned thi inventory at its original cost of $2,352. - December 12 - Hatcher Corporation paid Vogel Corporation for the amount owed. Required: a. Prepare the journal entries to record these transactions on the books of Vogel Corporation. b. What is the amount of net sales to be reported on Vogel Corporation's income statement? c. What is the Vogel Corporation's gross profit percentage? Complete this question by entering your answers in the tabs below. What is the amount of net sales to be reported on Vogel Corporation's income statement? December. Both companies use a perpetual inventory system using the gross method of recording sales discounts. - December 3 - Vogel Corporation sold inventory on account to Hatcher Corporation for $483,000, terms 1/10, n/30. This inv originally cost Vogel $307,000. - December 8 - Hatcher Corporation returned inventory to Vogel Corporation for a credit of $3,700. Vogel returned this inve inventory at its original cost of $2,352. - December 12 - Hatcher Corporation paid Vogel Corporation for the amount owed. Required: a. Prepare the journal entries to record these transactions on the bogks of Vogel Corporation. b. What is the amount of net sales to be reported on Vogel Corporation's income statement? c. What is the Vogel Corporation's gross profit percentage? Complete this question by entering your answers in the tabs below. What is the Vogel Corporation's gross profit percentage? (Round your answer to the nearest whole percent (i.e., 0.1234 should be entered as 12).)