Question

Two weeks later, you are assigned to the Quant team and you are asked by the team leader to generate a SGD discount factor table

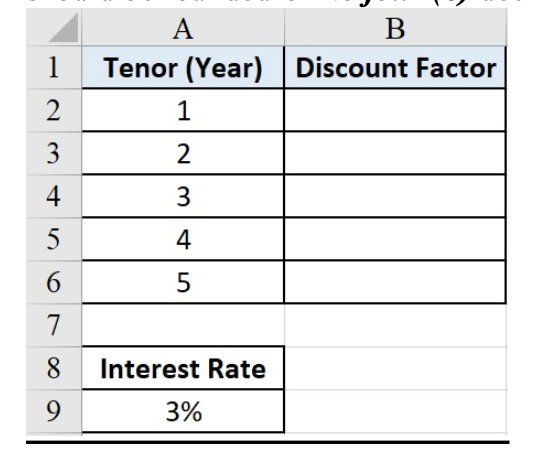

Two weeks later, you are assigned to the Quant team and you are asked by the team leader to generate a SGD discount factor table for 5 years. The cost of borrowing has increased to 3% yet the cost of borrowing curve continued to stay flat.

(a)

Solve for the discount factors using the formula approach. Show your use of the formula with the inputs (you may use the FORMULATEXT() function in Excel). All answers should be rounded-off to four (4) decimal places.

(b)

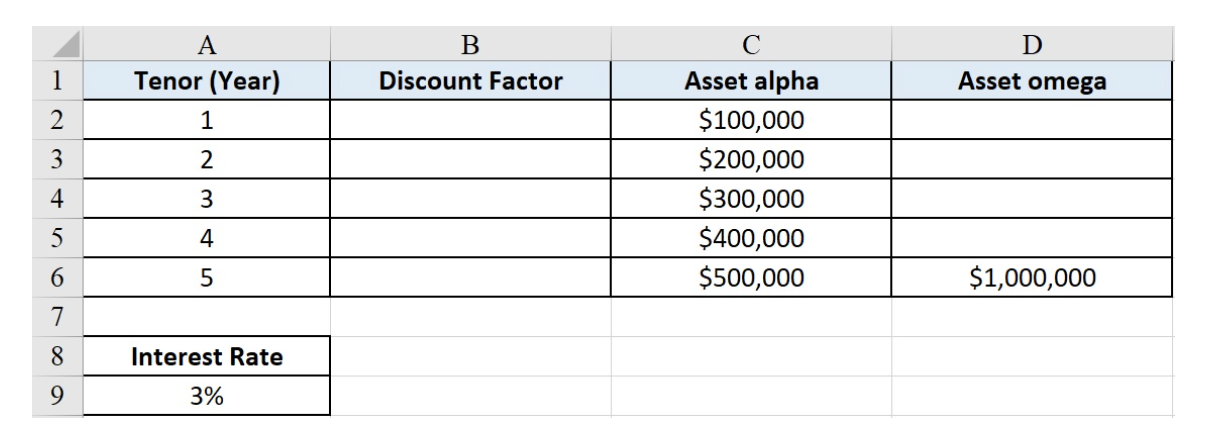

You are given a structured product to price. The structured product is a collection or combination of these two financial assets: Asset alpha and Asset omega, with predicted future cashflows as shown below.

With the Discount Factor Table you created in part (a), determine the price for the structured product. The final answer should be expressed up to two (2) decimal places.

A Tenor (Year) 1 B Discount Factor 1 2 3 2 3 4 5 4 6 5 7 8 Interest Rate 9 3% D 1 A Tenor (Year) 1 B Discount Factor Asset omega 2 3 2 Asset alpha $100,000 $200,000 $300,000 $400,000 $500,000 4 3 5 4 6 5 $1,000,000 7 8 Interest Rate 9 3%Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Offshore Finance And State Power

Authors: Andrea Binder

1st Edition

0192870122, 978-0192870124