Answered step by step

Verified Expert Solution

Question

1 Approved Answer

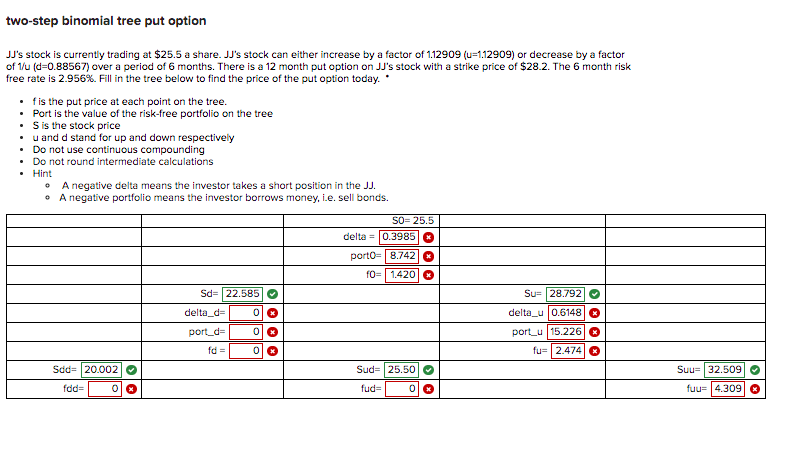

two-step binomial tree put option JU's stock is currently trading at $25.5 a share. JJ's stock can either increase by a factor of 1.12909 (u=1.12909)

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Cost Accounting A Managerial Emphasis

Authors: Charles T. Horngren, George Foster, Srikant M. Datar, Howard D. Teall, Foster Horngren, Data Horngren

3rd Canadian Edition

0130355801, 978-0130355805