Question

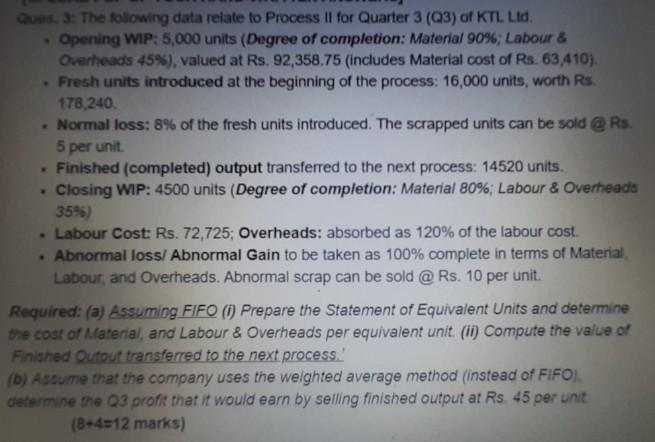

ues. 3: The following data relate to Process II for Quarter 3 (Q3) of KTL Ltd. W Opening WIP: 5,000 units (Degree of completion: Material

ues. 3: The following data relate to Process II for Quarter 3 (Q3) of KTL Ltd. W Opening WIP: 5,000 units (Degree of completion: Material 90%; Labour & Overheads 45%), valued at Rs. 92,358.75 (includes Material cost of Rs. 63,410). . Fresh units introduced at the beginning of the process: 16,000 units, worth Rs. 178,240. Normal loss: 8% of the fresh units introduced. The scrapped units can be sold @Rs. 5 per unit. Finished (completed) output transferred to the next process: 14520 units. Closing WIP: 4500 units (Degree of completion: Material 80%; Labour & Overheads 35%) . Labour Cost: Rs. 72,725; Overheads: absorbed as 120% of the labour cost. . Abnormal loss/ Abnormal Gain to be taken as 100% complete in terms of Material, Labour, and Overheads. Abnormal scrap can be sold @ Rs. 10 per unit. Required: (a) Assuming FIFO (i) Prepare the Statement of Equivalent Units and determine the cost of Material, and Labour & Overheads per equivalent unit. (ii) Compute the value of Finished Qutout transferred to the next process." (b) Assume that the company uses the weighted average method (instead of FIFO), determine the Q3 profit that it would earn by selling finished output at Rs. 45 per unit (8+4=12 marks)

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Principles Of Fraud Examination

Authors: Joseph T Wells

2nd Edition

0470128836, 9780470128831