Question

URGENT!!!! PLEASE HELP A month ago, DCP had been granted a 30-day exclusivity period to perform financial due diligence on AD Systems and had hired

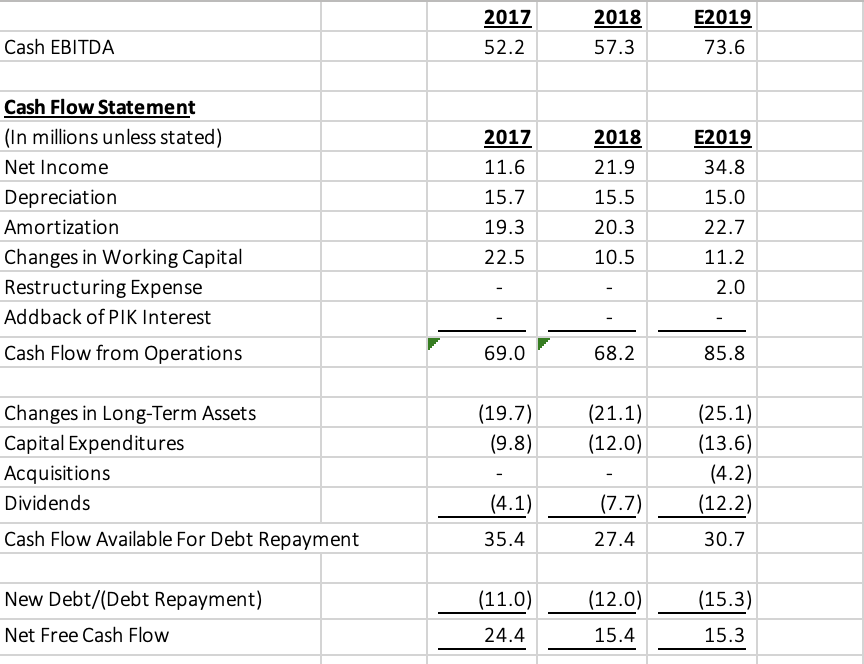

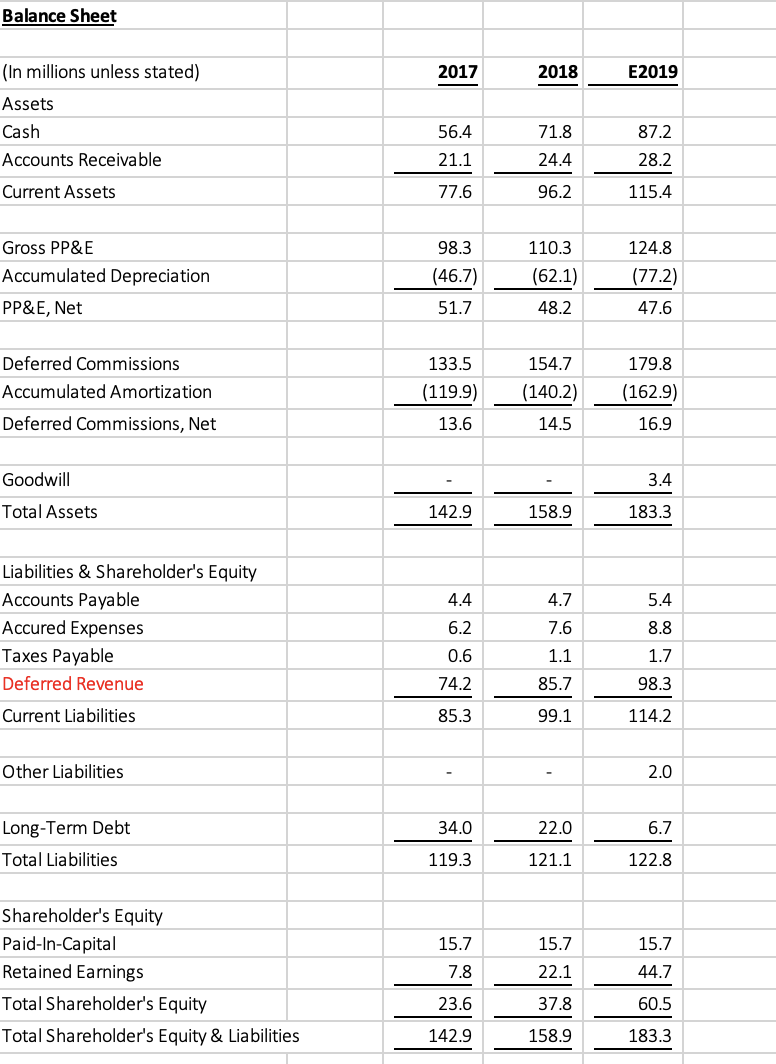

URGENT!!!! PLEASE HELP A month ago, DCP had been granted a 30-day exclusivity period to perform financial due diligence on AD Systems and had hired KPMG to perform the analysis. The exclusivity period had been granted based on the term sheet provided by DCP which stipulated that DCP would make a $65 million investment in ADS in exchange for newly issued convertible preferred shares. The parties had agreed on an enterprise value for ADS of 10x FYE 12/31/2019 expected cash EBITDA (a common non-GAAP metric in SaaS businesses). When calculating ADSs equity value and therefore the % ownership in ADS to be acquired for the $65 million, DCP had stipulated that the deferred revenue liability would be treated as a debt-like item and that the FYE 12/31/2019 expected cash EBITDA would be adjusted pursuant to a quality of earnings analysis. Among other items, Divaaliya had been provided with historical financial statements for FYE 12/31/2017 and 2018 as well as expected FYE 12/31/2019 financial statements.

Since then, Lucille Bluth had hired Joffreys, a leading tech investment banking firm, to advise her. Joffreys had insisted that it was market practice to treat deferred revenue as working capital rather than a debt-like item. Lucille now refused to move forward with the deal unless DCP made the corresponding adjustment to equity value.

Additionally, KPMG had completed its work and surfaced several relevant issues:

-The company had briefly entered the frozen banana business after taking over a bankrupt frozen banana stand in 2013. It sold this business on March 31, 2019, booking a profit of $7 million on the sale, which it reported as revenue in 2019. Frozen Banana had been generating $0.5 million of monthly cash EBITDA since ADS acquired it in 2016.

-ADS was on the verge of acquiring a software consulting business, Software Consulting Business. It expected closing to take place on September 30, 2019 and had included this business in the FYE 12/31/2019 expected financial statements for the period of ownership. Software Consulting Business had generated $0.45 million of monthly cash EBITDA throughout FY 2019 and was expected to continue doing so for the foreseeable future.

-In relation to the above acquisition, ADS expected to incur a restructuring expense of $2 million at closing, which the company and KPMG consider non-recurring. ADS had included this item as an operating expense in its Expected FY 2019 income statement and provided for it as a liability on its expected 12/31/2019 balance sheet. However, Maebe had neglected to identify this as a debt-like item in her pre Q of E valuation. The restructuring payments were expected to be made in 2020.

-ADS had performed a consulting assignment regarding the implementation of certain software services on behalf of the Venezuelan government. This assignment was a one-time project which contributed $3.3 million to ADSs cash EBITDA in 2019. Related to this contract, ADS now had $3.5 million in cash in a Venezuelan bank account, which it was unable to repatriate and should therefore be considered trapped or restricted.

-Lucilles four adult children had been drawing an aggregate of $4 million annually from the business, which the company had reported as an operating expense. Fortunately, these four were no longer involved in the business. DCPs term sheet had stipulated that any payments to family members not involved in the business would be discontinued at closing. However, under their employment contracts, Lucilles children were entitled to an aggregate $2 million severance payment in the event of a sale of the company.

-In addition, DCPs law firm, Over & Billings, believe that an ongoing patent dispute relating to ADSs use of a competitors technology was likely to be adjudicated against ADS. Their expected value for the settlement was $2.5 million which, in their view, would be paid sometime in 2021. No provision had been made for this in the ADSs financial statements. Finally, DCPs environmental consultant had found buried frozen banana waste on the companys owned headquarters which was threatening to leak into the water table. It estimated that the cost of cleaning the site would be $1 million. There was no provision for this in the companys financial statements.

QUESTION: Please bridge Maebes original calculation of net debt in 12/31/2019 to her post KMPG due diligence calculation of 12/31/2019 net debt, assuming, among other things, that she had originally treated deferred revenue as a DLI, but will now treat it as a working capital item.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Take The Trade A Floor Trade

Authors: Tony Wilson

1st Edition

979-8218195458