Question

U.S. 10 Year Treasury Note Data from WSJ: Face value $1,000; Price 99 14/32; Coupon 2.25%. If you predict that the US government will default

U.S. 10 Year Treasury Note Data from WSJ: Face value $1,000; Price 99 14/32; Coupon 2.25%. If you predict that the US government will default on its debt, so you decide to sell this bond at the beginning of the 6th year you hold this bond at market price 101 8/32. How much money do you make for holding this bond for the past several years?

A

$130.31

B

$242.81

C

129.62

D

241.53

Suppose that a US 30-year Treasury bonds bid price is quoted as 115-28, its face value is $1,000, then we know that the actual bid price for this bond is:

A

$115.28

B

$1152.8

C

$1156.39

D

$1158.75

Suppose we know that the coupon for TAMIU bond is $50, and each TAMIU bond has face value of $1,000, maturity is November 15, 2017. With all the information we can calculate the coupon rate for the TAMIU bond is:

A

2%

B

3%

C

4%

D

5%

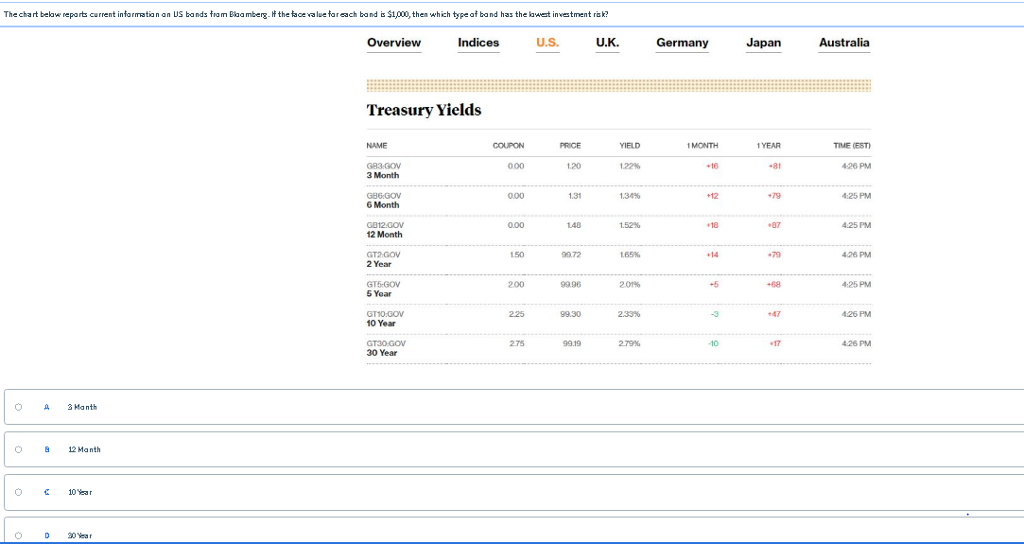

The cha rt below neparcurent informatia n an US ba nds fra m Boa mberg. hf the face value far each band s $1,000, then which type af ba nd has the kwet investment risk? U.K. Germany Japan Overview Indices U.S. Australia Treasury Yields 1 MONTH YEAR TIME (EST 0.00 1.20 426 PM 3 Month 0.00 1.31 +12 4:25 PM 6 Month 0.00 48 4.25 PM 12 Month 9372 426 PM 2 Year 200 4-25 PM GT5-GOV 5 Year 426 PM 10 Year 2 75 99.19 426 PM 30 Year O A anth 8 12 ManthStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Quantitative Finance: An Object-Oriented Approach In C++

Authors: Erik Schlogl, Dilip B. Madan

1st Edition

1584884797, 978-1584884798