Answered step by step

Verified Expert Solution

Question

1 Approved Answer

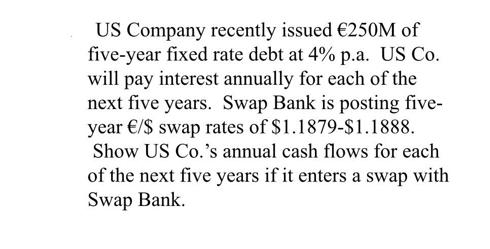

US Company recently issued 250M of five-year fixed rate debt at 4% p.a. US Co. will pay interest annually for each of the next

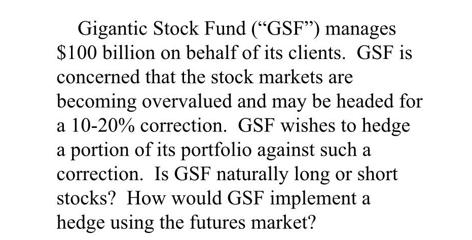

US Company recently issued 250M of five-year fixed rate debt at 4% p.a. US Co. will pay interest annually for each of the next five years. Swap Bank is posting five- year /$ swap rates of $1.1879-$1.1888. Show US Co.'s annual cash flows for each of the next five years if it enters a swap with Swap Bank. Gigantic Stock Fund ("GSF") manages $100 billion on behalf of its clients. GSF is concerned that the stock markets are becoming overvalued and may be headed for a 10-20% correction. GSF wishes to hedge a portion of its portfolio against such a correction. Is GSF naturally long or short stocks? How would GSF implement a hedge using the futures market?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

US Companys Annual Cash Flows with Swap Bank US Company issued 250 million of fiveyear fixedrate deb...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Fundamentals Of Corporate Finance

Authors: Jonathan Berk, Peter DeMarzo, Jarrad Harford

5th Edition

0135811600, 978-0135811603