Answered step by step

Verified Expert Solution

Question

1 Approved Answer

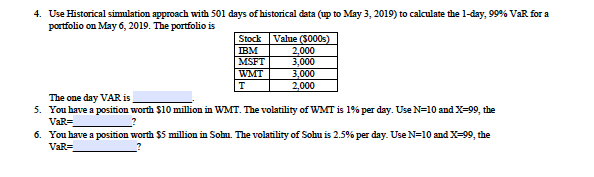

Use Historical simulation approach with 501 days of historical data (up to May 3, 2019) to calculate the 1-day, 99% VaR for a portfolio on

Use Historical simulation approach with 501 days of historical data (up to May 3, 2019) to calculate the 1-day, 99% VaR for a portfolio on May 6, 2019. The portfolio is

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Why The Poor Pay More How To Stop Predatory Lending

Authors: Gregory D. Squires

1st Edition

0313067902