Use table C Mint-Case B: t 5 marks} Mariela understands TaxFree Savings Account (TFSA) but also understands that the available contribution room can be tricky

Use table C

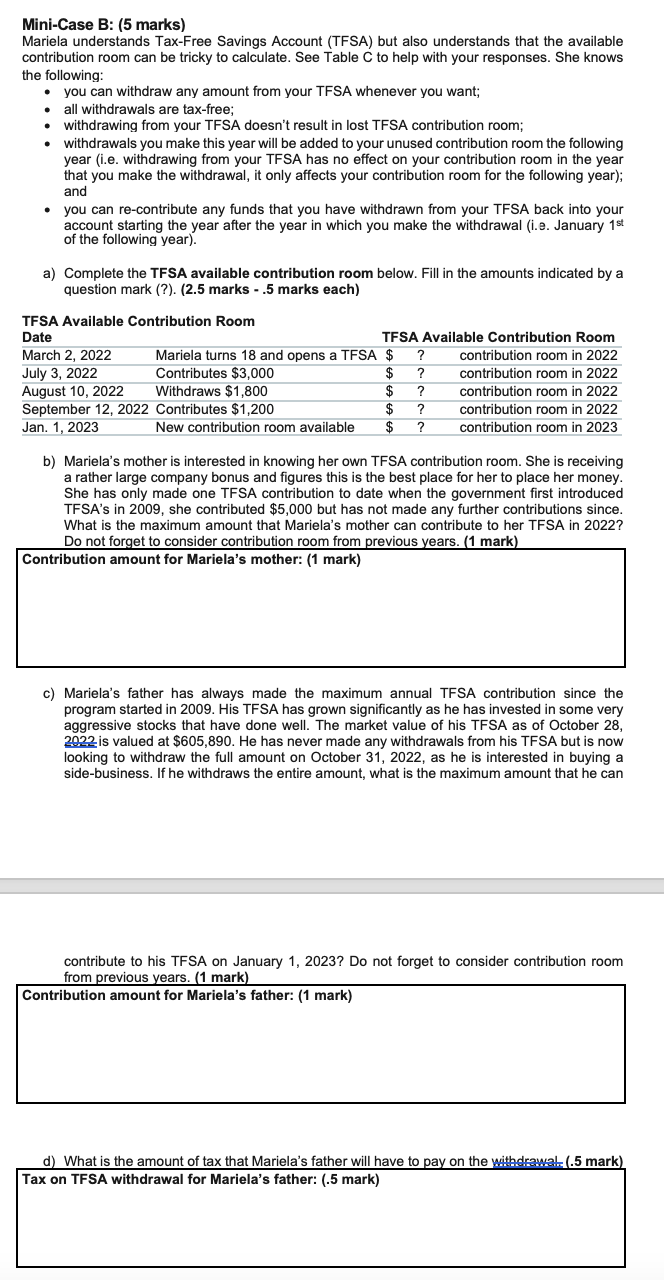

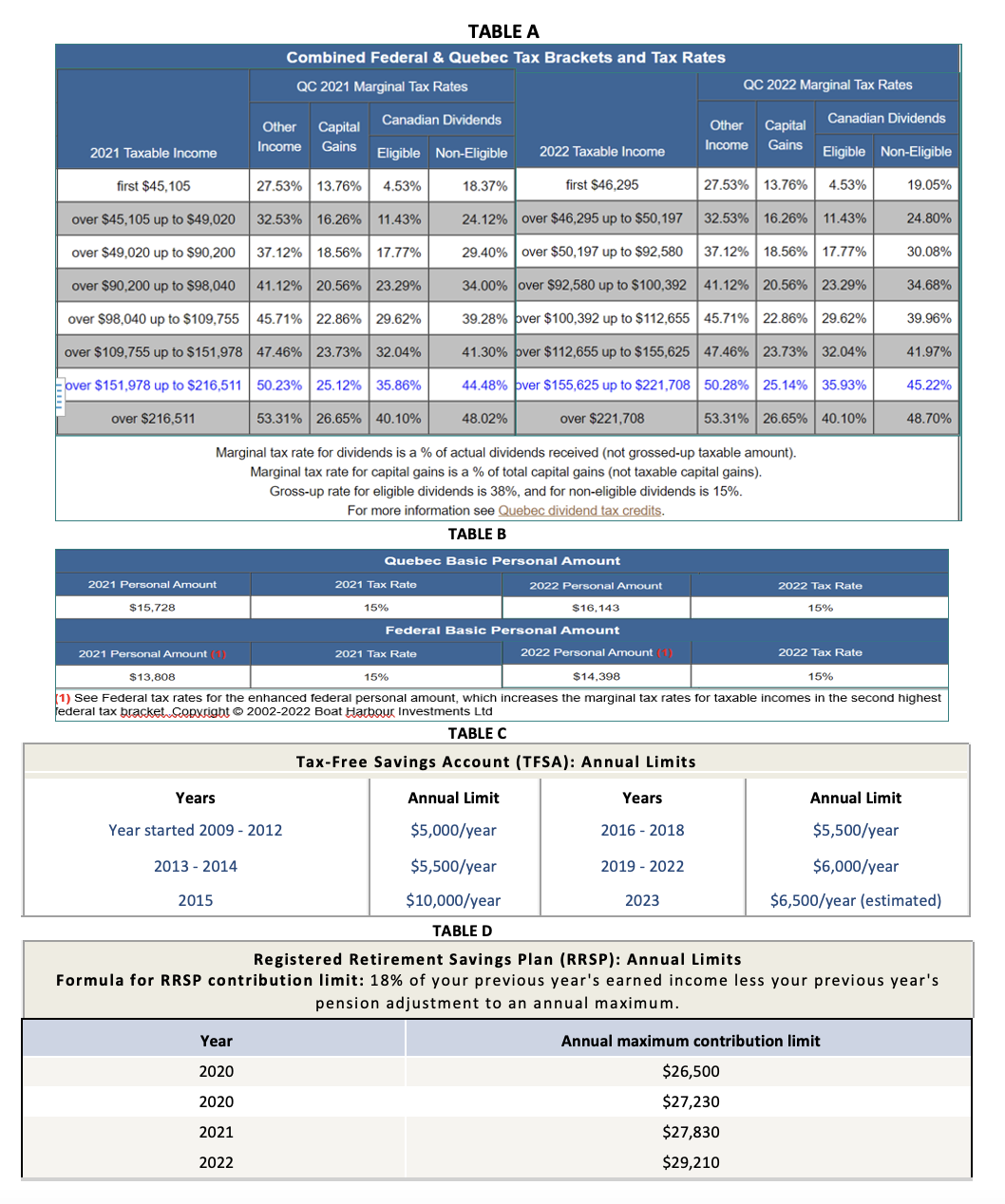

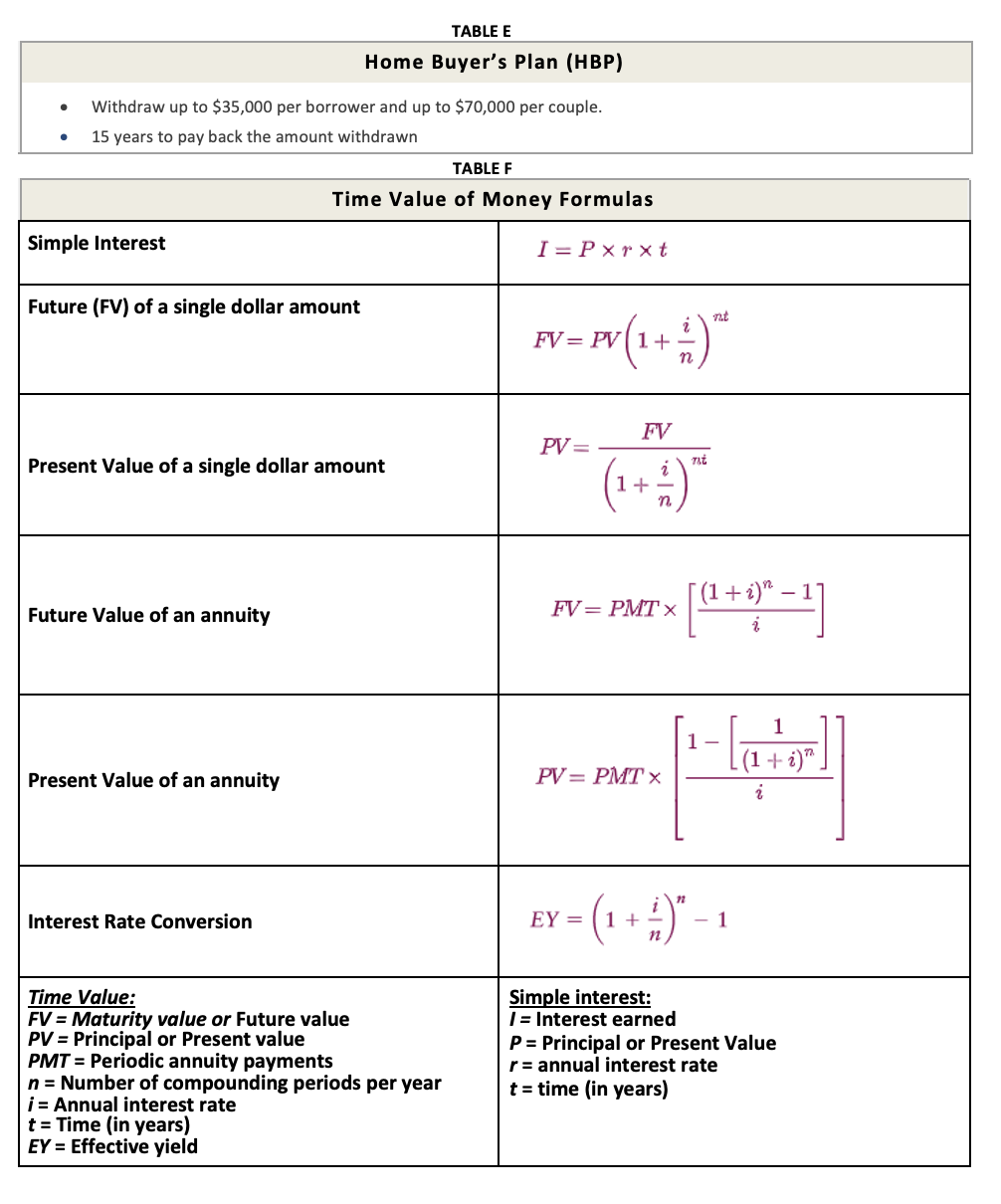

Mint-Case B: t 5 marks} Mariela understands TaxFree Savings Account (TFSA) but also understands that the available contribution room can be tricky to calculate. See Table C to help with your responses. She knows the following: o e o o a) you can withdraw any amount from your TFSA whenever you want; all withdrawals are tax-free; withdrawing from your TFSA doesn't result in lost TFSA contribution room: withdrawals you make this year will be added to your unused contribution room the following year (Le. withdrawing from your TFSA has no effect on your contribution room in the year that you make the withdrawal, it only affects your contribution room for the following year); and you can recontribute any funds that you have withdrawn from your TFSA back into your account starting the year after the year in which you make the withdrawal (Le. January 15' of the following year}. Complete the TFSA available contribution room below. Fill in the amounts indicated by a question mark {'n. {2.5 marks - .5 marks each) TF SA Available Contribution Room Date TF SA Available Contribution Room March 2, 2022 Mariela turns 18 and opens a TFSA $ '? contribution room in 2022 July 3, 2022 Contributes $3.000 $ ? contribution room in 2022 August 10, 2022 Withdraws $1.800 $ '? contribution room in 2022 September 12. 2022 Contributes $1.200 $ ? contribution room in 2022 Jan. 1, 2023 New contribution room available 35 '? contribution room in 2023 b) Marie la's mother is interested in knowing her own TFSA contribution room. She is receiving a rather large company bonus and gures this is the best place for her to place her money. She has only made one TFSA contribution to date when the government rst introduced TFSA's in 2009. she contributed $5,000 but has not made any further contributions since. What is the maximum amount that Mariela's mother can contribute to her TFSA in 2022'? Do not foret to consider contribution room from erevious ears. 1 mark Contribution amount for Marlela's mother: {1 mark] a) Marie la's father has always made the maximum annual TFSA contribution since the program started in 2009. His TFSA has grown signicantly as he has invested in some very aggressive stocks that have done well. The market value of his TFSA as of October 28, aegis valued at $605,890. He has never made any withdrawals from his TFSA but is now looking to withdraw the full amount on October 31, 2022. as he is interested in buying a sidebusiness. If he withdraws the entire amount, what is the maximum amount that he can contribute to his TFSA on January 1, 2023? Do not forget to consider contribution room from urevious ears. 1 mark Contribution amount for Marlela's father: [1 mark} 0 What is the amount of tax that Mariela's father will have to l . on the ..'.::.r ......... .5 mark Tax on TFSA withdrawal for Marlela's father: (.5 mark) TABLE A Combined Federal & Quebec Tax Brackets and Tax Rates QC 2021 Marginal Tax Rates QC 2022 Marginal Tax Rates Canadian Dividends Other Capital Canadian Dividends Other Capital 2021 Taxable Income Income Gains 2022 Taxable Income Gains Eligible Non-Eligible Income Eligible Non-Eligible first $45,105 27.53% 13.76% 4.53% 18.37% first $46,295 27.53% 13.76% 4.53% 19.05% over $45,105 up to $49,020 32.53% 16.26% 11.43% 24.12% over $46,295 up to $50, 197 32.53% 16.26% 11.43% 24.80% over $49,020 up to $90,200 37.12% 18.56% 17.77% 29.40% over $50, 197 up to $92,580 37.12% 18.56% 17.77% 30.08% over $90,200 up to $98,040 41.12% 20.56% 23.29% 34.00% over $92,580 up to $100,392 41.12% 20.56% 23.29% 34.68% over $98,040 up to $109,755 45.71% 22.86% 29.62% 39.28% over $100,392 up to $112,655 45.71% 22.86% 29.62% 39.96% over $109,755 up to $151,978 47.46% 23.73% 32.04% 41.30% over $112,655 up to $155,625 47.46% 23.73% 32.04% 41.97% over $151,978 up to $216,511 50.23% 25.12% 35.86% 44.48% over $155,625 up to $221,708 50.28% 25.14% 35.93% 45.22% over $216,511 53.31% 26.65% 40.10% 48.02% over $221,708 53.31% 26.65% 40.10% 48.70% Marginal tax rate for dividends is a % of actual dividends received (not grossed-up taxable amount). Marginal tax rate for capital gains is a % of total capital gains (not taxable capital gains). Gross-up rate for eligible dividends is 38%, and for non-eligible dividends is 15%. For more information see Quebec dividend tax credits. TABLE B Quebec Basic Personal Amount 2021 Personal Amount 2021 Tax Rate 2022 Personal Amount 2022 Tax Rate $15,728 15% $16,143 15% Federal Basic Personal Amount 2021 Personal Amount (1) 2021 Tax Rate 2022 Personal Amount (1) 2022 Tax Rate $13,808 15% $14,398 15% 1) See Federal tax rates for the enhanced federal personal amount, which increases the marginal tax rates for taxable incomes in the second highest federal tax bracket Copyright @ 2002-2022 Boat Harbour Investments Lid TABLE C Tax-Free Savings Account (TFSA): Annual Limits Years Annual Limit Year Annual Limit Year started 2009 - 2012 $5,000/year 2016 - 2018 $5,500/year 2013 - 2014 $5,500/year 2019 - 2022 $6,000/year 2015 $10,000/year 2023 $6,500/year (estimated) TABLE D Registered Retirement Savings Plan (RRSP): Annual Limits Formula for RRSP contribution limit: 18% of your previous year's earned income less your previous year's pension adjustment to an annual maximum. Year Annual maximum contribution limit 2020 $26,500 2020 $27,230 2021 $27,830 2022 $29,210TABLEE Home Buyer's Plan (HBP) - Withdraw up to $35,000 per borrower and up to $70,000 per couple. a 15 years to pay back the amount withdrawn TABLE F Time Value of Money Formulas Future (FV) of a single dollar amount Present Value of a single dollar amount Future Value of an annuity Present Value of an annuity Interest Rate Conversion Time Value: Simple interest: FV= Maturity value or Future value i: Interest earned PV= Principal or Present value p = Principal or Present Value PMT= Periodic annuity payments r = annual interest rate n = Number of compounding periods per year t = time (in years) if: Annual interest rate r = Time (in years) EY = Effective yield

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance