Answered step by step

Verified Expert Solution

Question

1 Approved Answer

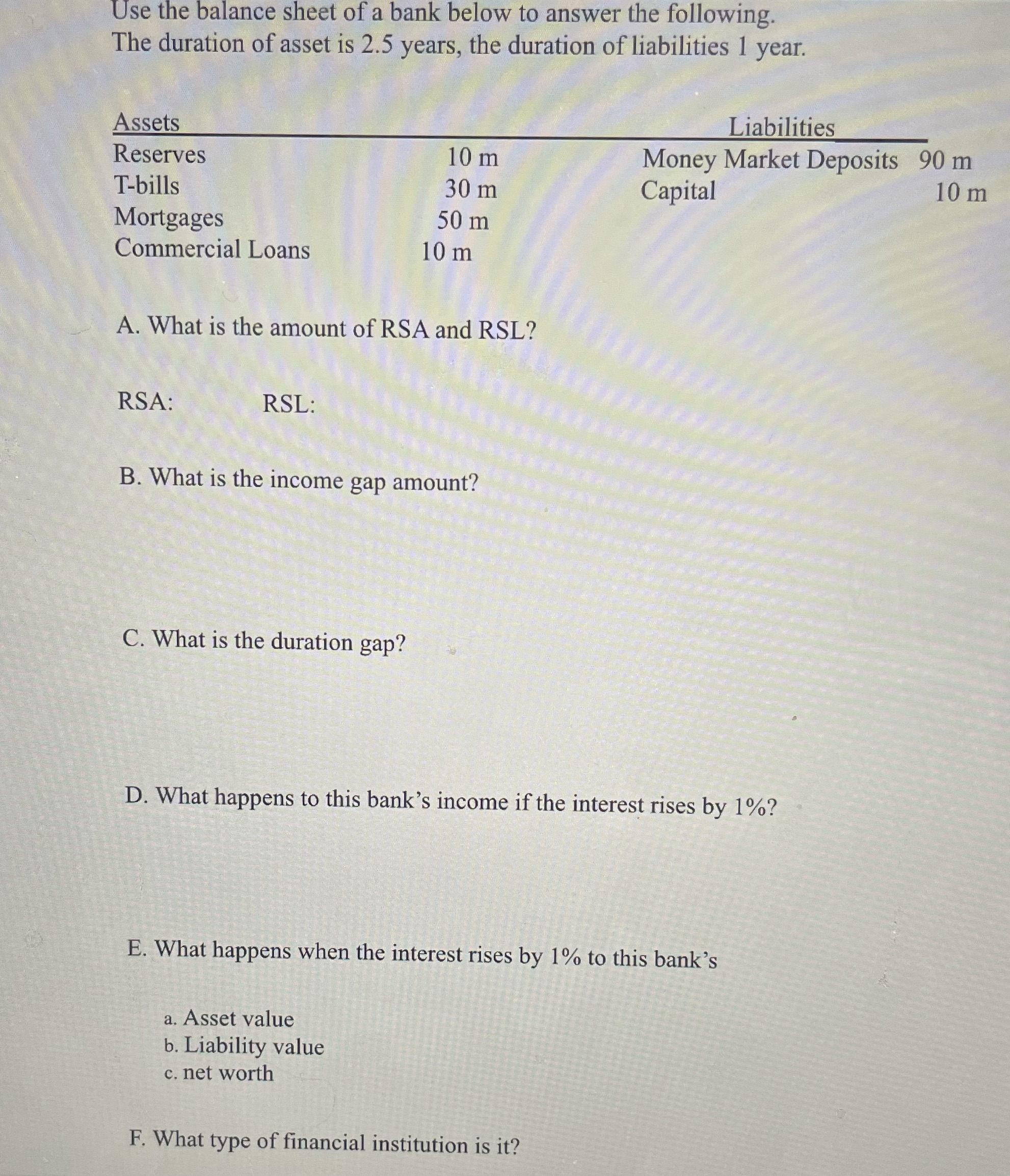

Use the balance sheet of a bank below to answer the following. The duration of asset is 2.5 years, the duration of liabilities 1

Use the balance sheet of a bank below to answer the following. The duration of asset is 2.5 years, the duration of liabilities 1 year. Liabilities Assets Reserves 10 m T-bills 30 m Money Market Deposits 90 m Capital 10 m Mortgages 50 m Commercial Loans 10 m A. What is the amount of RSA and RSL? RSA: RSL: B. What is the income gap amount? C. What is the duration gap? D. What happens to this bank's income if the interest rises by 1%? E. What happens when the interest rises by 1% to this bank's a. Asset value b. Liability value c. net worth F. What type of financial institution is it?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

A The amount of RSA RateSensitive Assets and RSL RateSensitive Liabilities can be calculated as foll...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Document Format ( 2 attachments)

661e815cefb62_880744.pdf

180 KBs PDF File

661e815cefb62_880744.docx

120 KBs Word File

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Money Banking and Financial Markets

Authors: Stephen Cecchetti, Kermit Schoenholtz

5th edition

77536320, 77536329, 1259746747, 978-1259746741