Answered step by step

Verified Expert Solution

Question

1 Approved Answer

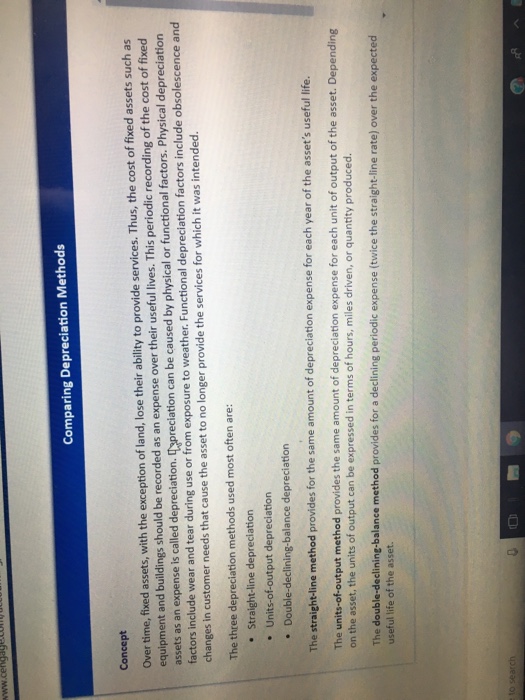

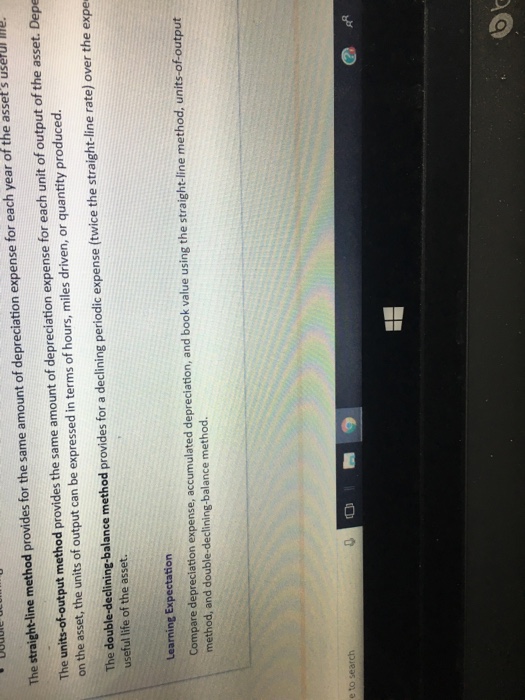

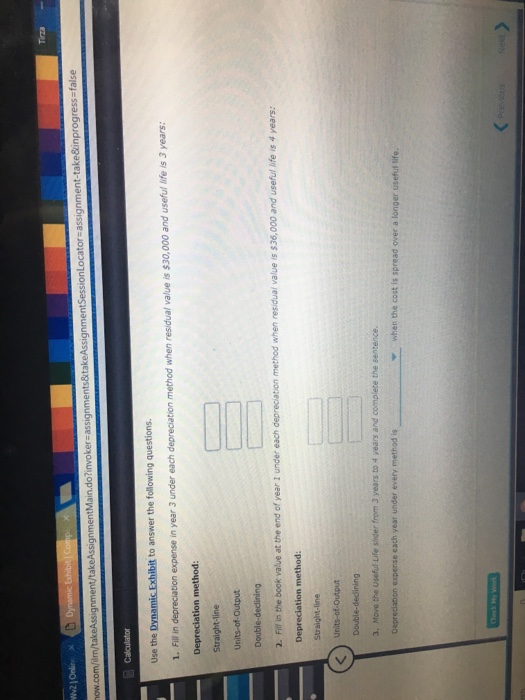

use the dynamic exhibit to answer the following questions. 1. Fill in depreciation expense in year 3 under each depreciation method when residual value is

use the dynamic exhibit to answer the following questions.

1. Fill in depreciation expense in year 3 under each depreciation method when residual value is 30,000 and useful life is 3 years

2. Fill in the book value at the end of year 1 under each depreciation method when residual value is 36,000 and useful life is 4 years

3. Move the useful life slider from 3 years to 4 years and complete the sentence

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

New Markets Tax Credit IRS Audit Technique Guide

Authors: Internal Revenue Service

1st Edition

1304112896, 978-1304112897