Question

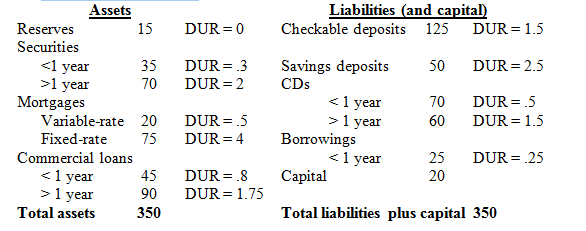

Use the following balance sheet (in millions of dollars) for a bank and assume that 20% of fixed-rate mortgages, 10 % of checkable deposits, and

Use the following balance sheet (in millions of dollars) for a bank and assume that 20% of fixed-rate mortgages, 10 % of checkable deposits, and 10% of savings deposits are rate-sensitive. Assume all variable-rate mortgages are rate-sensitive. DUR stands for duration

Consider assets and liabilities of less than a year to maturity to be rate-sensitive (one-year maturity bucket).

a. Calculate the repricing (funding) gap for a one-year maturity bucket.

b.Calculate the change in net interest income in the first year for a decrease in interest rate from 5% to 4% (be sure to note whether income increases or decreases).

c. Calculate the average duration of assets.

d. Calculate the average duration of liabilities.

e. Calculate the leverage-adjusted duration gap.

f. Calculate the change in net worth (capital) if the interest rate decreases from 5% to 4%?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Innovation Regulation And Crises In History

Authors: Harold James

1st Edition

0367669528, 978-0367669522