Answered step by step

Verified Expert Solution

Question

1 Approved Answer

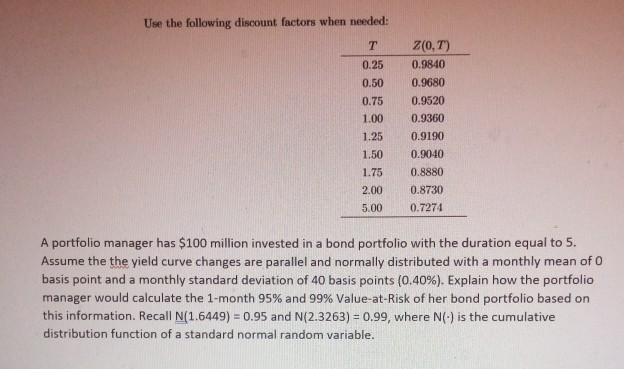

Use the following discount factors when needed: T 0.25 0.50 0.75 1.00 1.25 1.50 1.75 2.00 5.00 Z(0,7) 0.9840 0.9680 0.9520 0.9360 0.9190 0.9040 0.8880

Use the following discount factors when needed: T 0.25 0.50 0.75 1.00 1.25 1.50 1.75 2.00 5.00 Z(0,7) 0.9840 0.9680 0.9520 0.9360 0.9190 0.9040 0.8880 0.8730 0.7274 A portfolio manager has $100 million invested in a bond portfolio with the duration equal to 5. Assume the the yield curve changes are parallel and normally distributed with a monthly mean of O basis point and a monthly standard deviation of 40 basis points (0.40%). Explain how the portfolio manager would calculate the 1-month 95% and 99% Value-at-Risk of her bond portfolio based on this information. Recall N(1.6449) = 0.95 and N(2.3263) = 0.99, where N(-) is the cumulative distribution function of a standard normal random variable

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Ebay Tips And Tricks To Increase Your Ebay Sales

Authors: Jessica Wilson

1st Edition

1774854015, 978-1774854013