Answered step by step

Verified Expert Solution

Question

1 Approved Answer

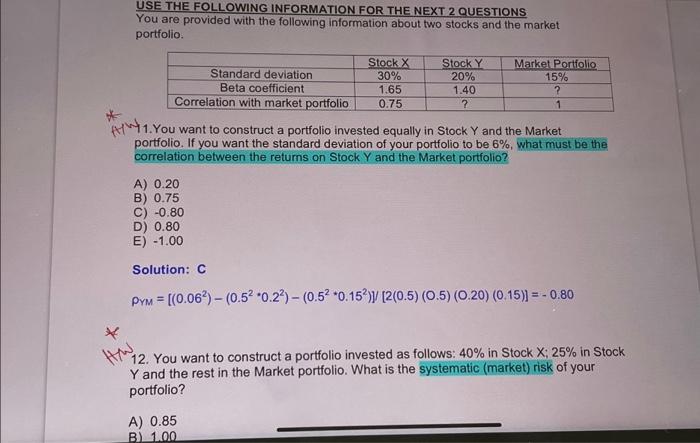

USE THE FOLLOWING INFORMATION FOR THE NEXT 2 QUESTIONS You are provided with the following information about two stocks and the market portfolio. * HAW

USE THE FOLLOWING INFORMATION FOR THE NEXT 2 QUESTIONS You are provided with the following information about two stocks and the market portfolio. * HAW Stock X 30% 1.65 Correlation with market portfolio 0.75 A) 0.20 B) 0.75 Standard deviation Beta coefficient Stock Y 20% 1.40 ? Market Portfolio 15% ? 1. You want to construct a portfolio invested equally in Stock Y and the Market portfolio. If you want the standard deviation of your portfolio to be 6%, what must be the correlation between the returns on Stock Y and the Market portfolio? A) 0.85 B) 1.00 1 C) -0.80 D) 0.80 E) -1.00 Solution: C PYM = [(0.062) - (0.52 *0.22) - (0.52 *0.152)]/[2(0.5) (0.5) (0.20) (0.15)] = -0.80 12. You want to construct a portfolio invested as follows: 40% in Stock X; 25% in Stock Y and the rest in the Market portfolio. What is the systematic (market) risk of your portfolio?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Robonomics Prepare Today For The Jobless Economy Of Tomorrow

Authors: John Crews

1st Edition

1530910463, 978-1530910465