Question

Use the following information for the remaining questions: Assume it is currently October, and the S&P 500 is currently at a level of 1898.20, and

Use the following information for the remaining questions: Assume it is currently October, and the S&P 500 is currently at a level of 1898.20, and S&P 500 e-mini futures with December expiration are trading at a contract price of 1892.75 and have a contract size of 50.

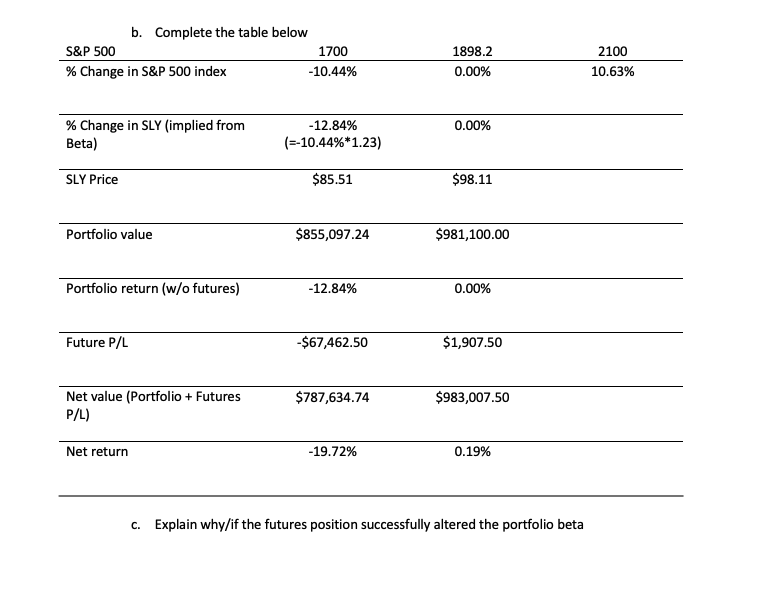

An investor currently holds 10,000 shares of SLY (SPDR S&P 600 small cap ETF, Beta=1.23, current price = $98.11/share, current portfolio value = $981,100.00). The investor wishes to temporarily increase the portfolio beta to 1.9 a. Determine the position that the investor should take in the futures market to alter the portfolio beta.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Public Finance And Public Policy

Authors: Jonathan Gruber

7th Edition

1319281109, 9781319281106