Question

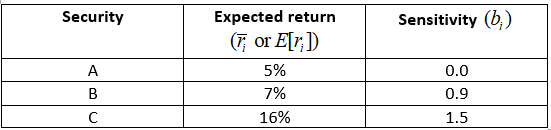

Use the information in the following table to answer questions 9 12. Assume a one-factor APT world. You have identified the expected returns and sensitivities

Use the information in the following table to answer questions 9 12. Assume a one-factor APT world. You have identified the expected returns and sensitivities for the following three large portfolios.

Using Excel, graph the 3 securities in expected return - sensitivity space. Based on your graph,

a. Which security is relatively underpriced?

b. Which security is relatively overpriced?

10. In a perfectly competitive market, the above risks and returns cannot exist for long. Describe the forces that bring about equilibrium.

11. What three conditions define an arbitrage portfolio?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Nurse Managers Guide To Budgeting And Finance

Authors: Al Rundio

2nd Edition

1940446589, 978-1940446585