Answered step by step

Verified Expert Solution

Question

1 Approved Answer

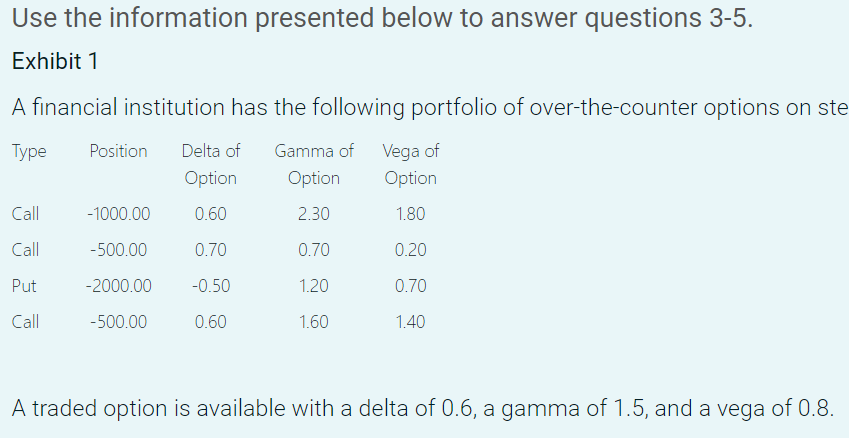

Use the information presented below to answer questions 3-5. Exhibit 1 A financial institution has the following portfolio of over-the-counter options on ste A traded

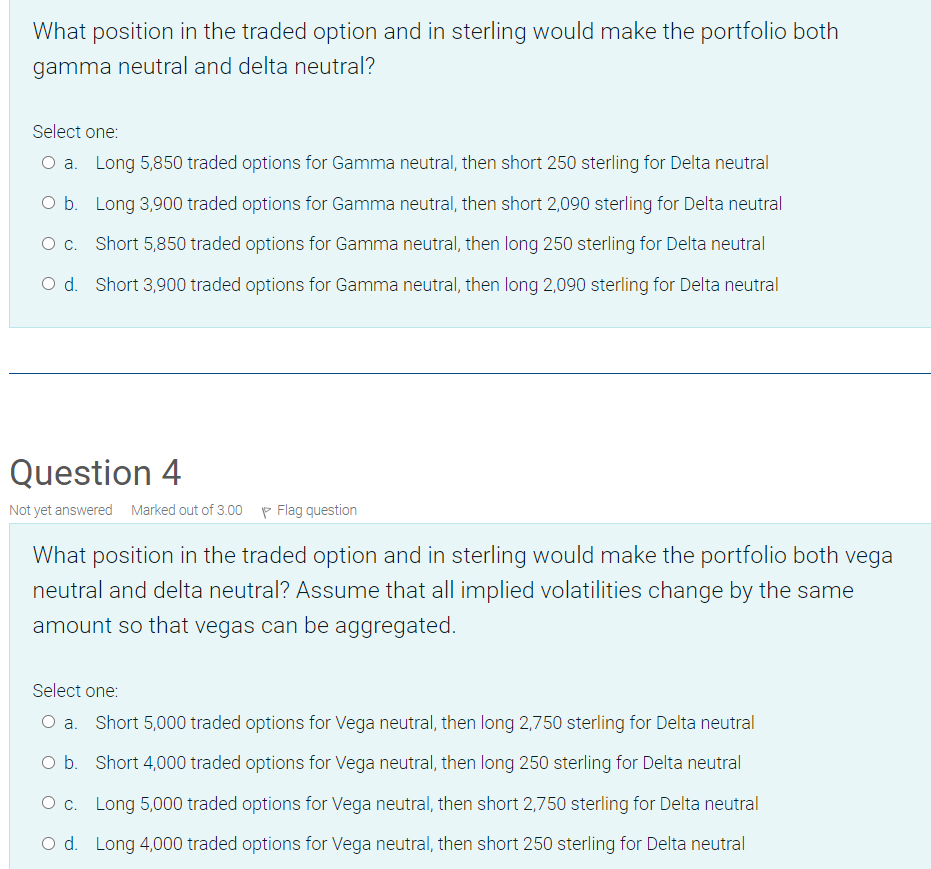

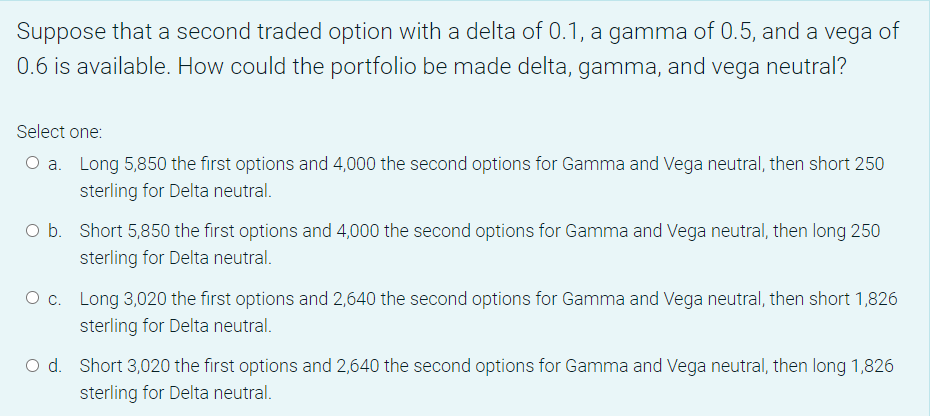

Use the information presented below to answer questions 3-5. Exhibit 1 A financial institution has the following portfolio of over-the-counter options on ste A traded option is available with a delta of 0.6 , a gamma of 1.5 , and a vega of 0.8 . What position in the traded option and in sterling would make the portfolio both gamma neutral and delta neutral? Select one: a. Long 5,850 traded options for Gamma neutral, then short 250 sterling for Delta neutral b. Long 3,900 traded options for Gamma neutral, then short 2,090 sterling for Delta neutral c. Short 5,850 traded options for Gamma neutral, then long 250 sterling for Delta neutral d. Short 3,900 traded options for Gamma neutral, then long 2,090 sterling for Delta neutral Question 4 ot yet answered Marked out of 3.00 p Flag question What position in the traded option and in sterling would make the portfolio both vega neutral and delta neutral? Assume that all implied volatilities change by the same amount so that vegas can be aggregated. Select one: a. Short 5,000 traded options for Vega neutral, then long 2,750 sterling for Delta neutral b. Short 4,000 traded options for Vega neutral, then long 250 sterling for Delta neutral c. Long 5,000 traded options for Vega neutral, then short 2,750 sterling for Delta neutral d. Long 4,000 traded options for Vega neutral, then short 250 sterling for Delta neutral Suppose that a second traded option with a delta of 0.1 , a gamma of 0.5 , and a vega of 0.6 is available. How could the portfolio be made delta, gamma, and vega neutral? Select one: a. Long 5,850 the first options and 4,000 the second options for Gamma and Vega neutral, then short 250 sterling for Delta neutral. b. Short 5,850 the first options and 4,000 the second options for Gamma and Vega neutral, then long 250 sterling for Delta neutral. c. Long 3,020 the first options and 2,640 the second options for Gamma and Vega neutral, then short 1,826 sterling for Delta neutral. d. Short 3,020 the first options and 2,640 the second options for Gamma and Vega neutral, then long 1,826 sterling for Delta neutral

Use the information presented below to answer questions 3-5. Exhibit 1 A financial institution has the following portfolio of over-the-counter options on ste A traded option is available with a delta of 0.6 , a gamma of 1.5 , and a vega of 0.8 . What position in the traded option and in sterling would make the portfolio both gamma neutral and delta neutral? Select one: a. Long 5,850 traded options for Gamma neutral, then short 250 sterling for Delta neutral b. Long 3,900 traded options for Gamma neutral, then short 2,090 sterling for Delta neutral c. Short 5,850 traded options for Gamma neutral, then long 250 sterling for Delta neutral d. Short 3,900 traded options for Gamma neutral, then long 2,090 sterling for Delta neutral Question 4 ot yet answered Marked out of 3.00 p Flag question What position in the traded option and in sterling would make the portfolio both vega neutral and delta neutral? Assume that all implied volatilities change by the same amount so that vegas can be aggregated. Select one: a. Short 5,000 traded options for Vega neutral, then long 2,750 sterling for Delta neutral b. Short 4,000 traded options for Vega neutral, then long 250 sterling for Delta neutral c. Long 5,000 traded options for Vega neutral, then short 2,750 sterling for Delta neutral d. Long 4,000 traded options for Vega neutral, then short 250 sterling for Delta neutral Suppose that a second traded option with a delta of 0.1 , a gamma of 0.5 , and a vega of 0.6 is available. How could the portfolio be made delta, gamma, and vega neutral? Select one: a. Long 5,850 the first options and 4,000 the second options for Gamma and Vega neutral, then short 250 sterling for Delta neutral. b. Short 5,850 the first options and 4,000 the second options for Gamma and Vega neutral, then long 250 sterling for Delta neutral. c. Long 3,020 the first options and 2,640 the second options for Gamma and Vega neutral, then short 1,826 sterling for Delta neutral. d. Short 3,020 the first options and 2,640 the second options for Gamma and Vega neutral, then long 1,826 sterling for Delta neutral Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Selling Professional And Financial Services Handbook

Authors: Scott Paczosa, Chuck Peruchini

1st Edition

1118728149, 978-1118728147