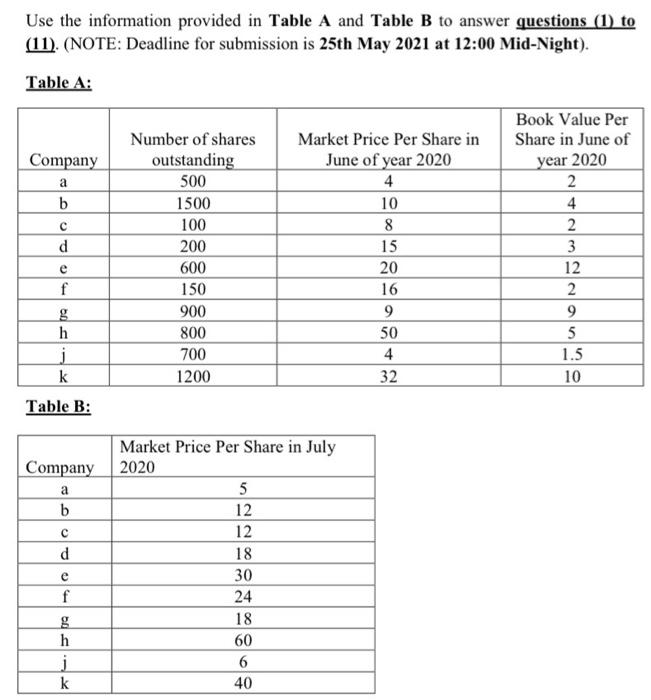

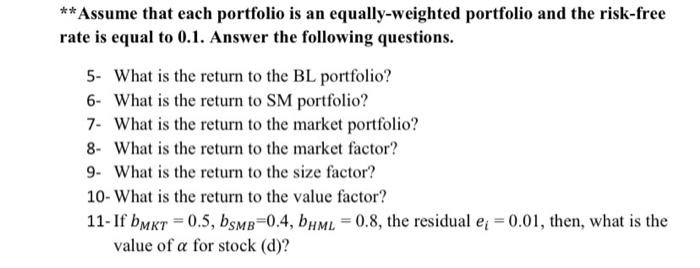

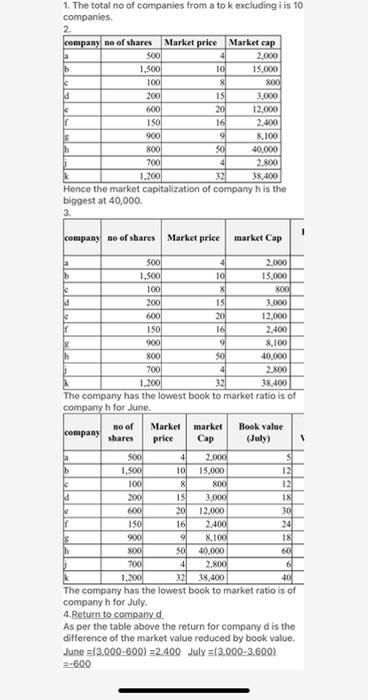

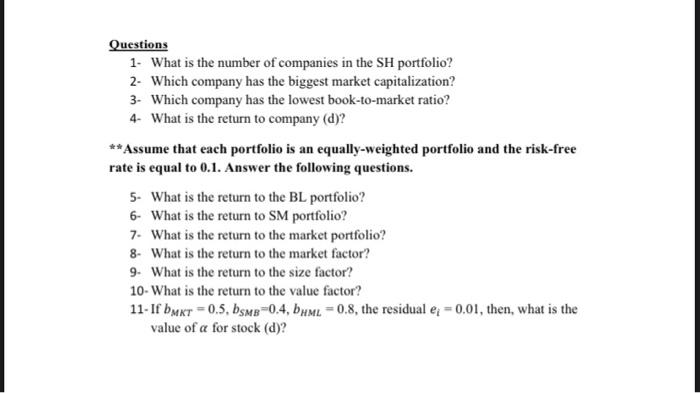

Use the information provided in Table A and Table B to answer questions (1) to (11). (NOTE: Deadline for submission is 25th May 2021 at 12:00 Mid-Night). Table A: Company a b d Number of shares outstanding 500 1500 100 200 600 150 900 800 700 1200 Market Price Per Share in June of year 2020 4 10 8 15 20 16 9 50 4 32 Book Value Per Share in June of year 2020 2 4 2 3 12 2 9 5 1.5 10 e f h j k Table B: Company a b Market Price Per Share in July 2020 5 12 12 18 30 d e 24 f g h j k 18 60 6 40 **Assume that each portfolio is an equally-weighted portfolio and the risk-free rate is equal to 0.1. Answer the following questions. 5. What is the return to the BL portfolio? 6- What is the return to SM portfolio? 7- What is the return to the market portfolio? 8- What is the return to the market factor? 9. What is the return to the size factor? 10- What is the return to the value factor? 11- If bmkt = 0.5, bsMB=0.4, bumL = 0.8, the residual ei = 0.01, then, what is the value of a for stock (d)? Questions 1. What is the number of companies in the SH portfolio? 2- Which company has the biggest market capitalization? 3- Which company has the lowest book-to-market ratio? 4- What is the return to company (d)? *Assume that each portfolio is an equally-weighted portfolio and the risk-free rate is equal to 0.1. Answer the following questions. 5- What is the return to the BL portfolio? 6- What is the return to SM portfolio? 7. What is the return to the market portfolio? 8. What is the return to the market factor? 9. What is the return to the size factor? 10. What is the return to the value factor? 11- If bakt = 0.5, bsme=0.4, bhme=0.8, the residual e = 0.01, then, what is the value of a for stock (d)? Use the information provided in Table A and Table B to answer questions (1) to (11). (NOTE: Deadline for submission is 25th May 2021 at 12:00 Mid-Night). Table A: Company a b d Number of shares outstanding 500 1500 100 200 600 150 900 800 700 1200 Market Price Per Share in June of year 2020 4 10 8 15 20 16 9 50 4 32 Book Value Per Share in June of year 2020 2 4 2 3 12 2 9 5 1.5 10 e f h j k Table B: Company a b Market Price Per Share in July 2020 5 12 12 18 30 d e 24 f g h j k 18 60 6 40 **Assume that each portfolio is an equally-weighted portfolio and the risk-free rate is equal to 0.1. Answer the following questions. 5. What is the return to the BL portfolio? 6- What is the return to SM portfolio? 7- What is the return to the market portfolio? 8- What is the return to the market factor? 9. What is the return to the size factor? 10- What is the return to the value factor? 11- If bmkt = 0.5, bsMB=0.4, bumL = 0.8, the residual ei = 0.01, then, what is the value of a for stock (d)? Questions 1. What is the number of companies in the SH portfolio? 2- Which company has the biggest market capitalization? 3- Which company has the lowest book-to-market ratio? 4- What is the return to company (d)? *Assume that each portfolio is an equally-weighted portfolio and the risk-free rate is equal to 0.1. Answer the following questions. 5- What is the return to the BL portfolio? 6- What is the return to SM portfolio? 7. What is the return to the market portfolio? 8. What is the return to the market factor? 9. What is the return to the size factor? 10. What is the return to the value factor? 11- If bakt = 0.5, bsme=0.4, bhme=0.8, the residual e = 0.01, then, what is the value of a for stock (d)