Answered step by step

Verified Expert Solution

Question

1 Approved Answer

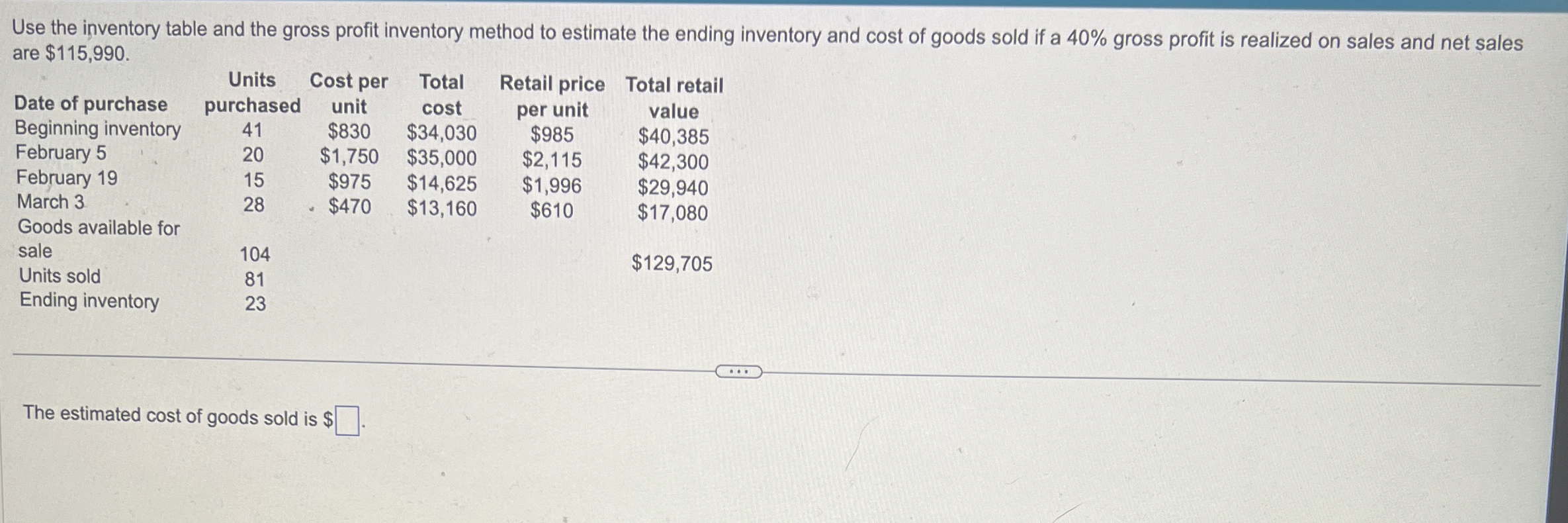

Use the inventory table and the gross profit inventory method to estimate the ending inventory and cost of goods sold if a 4 0 %

Use the inventory table and the gross profit inventory method to estimate the ending inventory and cost of goods sold if a gross profit is realized on sales and net sales are $

tableDate of purchase,tableUnitspurchasedtableCost perunittableTotalcosttableRetail priceper unittableTotal retaivalueBeginning inventory,$$$$

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Audit Quality And Financial Statements Fraud Detection

Authors: Asma Al-znaimat, Mohammad Al- Dahiyat

1st Edition

3659537888, 978-3659537882