Answered step by step

Verified Expert Solution

Question

1 Approved Answer

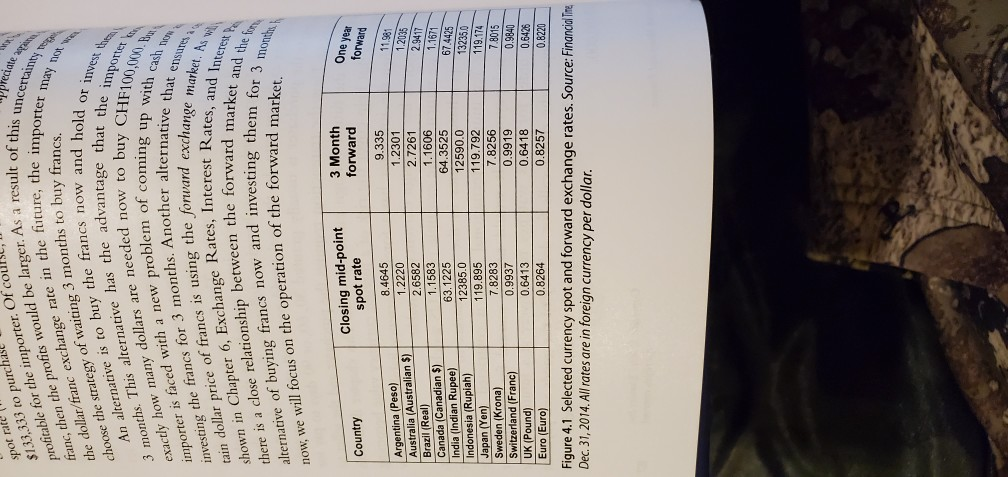

use the table and answer the problems $133,333 to purch profitable for the importer. Of coul franc , then the profits would be larger .

use the table and answer the problems

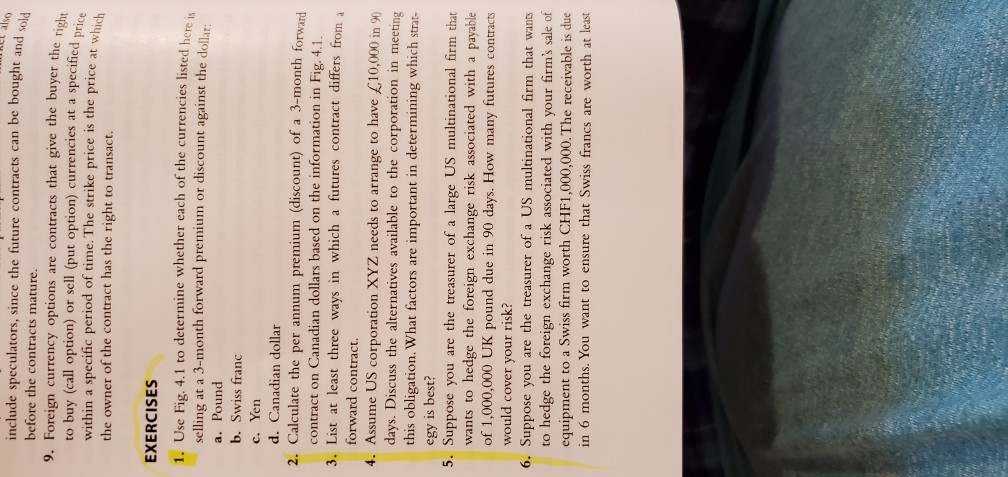

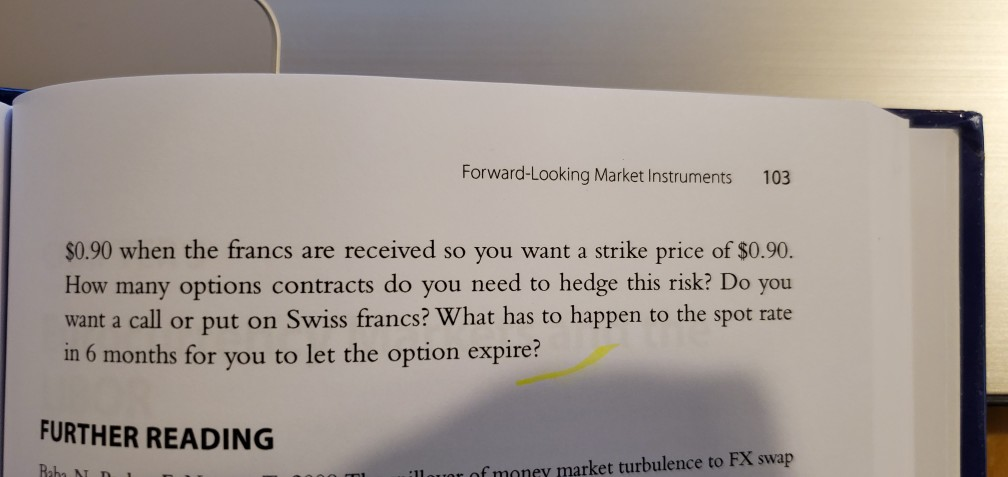

$133,333 to purch profitable for the importer. Of coul franc , then the profits would be larger . As a result of this uncertas the dollar / franc exchange rate in the future , the importer may to 3 months . This alternative has the advantage that the importer An alternative is to buy the francs now and hold or investeem investing the francs for 3 months . Another alternative that importer is faced with a new problem of coming up with cask tain dollar price of francs is using the forward exchange market . A there is a close relationship between the forward market and the shown in Chapter 6 , Exchange Rates , Interest Rates , and Intereste alternative of buying francs now and investing them for 3 months exactly how many dollars are needed now to buy CHF100.W . now , we will focus on the operation of the forward market . spot rate reciate the choose the strategy of waiting 3 months to buy francs. ense Closing mid-point spot rate 3 Month forward Country One year forward 11.981 1.2035 2.9417 1.1671 67.4425 132350 119.174 7.8015 0.9840 0.6426 8.4645 9.335 Argentina (Peso) Australia (Australian $) 1.2220 1.2301 2.6582 2.7261 Brazil (Real) Canada Canadian $) 1.1583 1.1606 India (Indian Rupee) 63.1225 64.3525 Indonesia (Rupiah) 12385.0 12590.0 Japan (Yen) 119.895 119.792 Sweden (Krona) 7.8283 7.8256 Switzerland (Franc) 0.9919 UK (Pound) 0.6413 0.6418 Euro (Euro) 0.8264 0.8257 0.8220 Figure 4.1 Selected currency spot and forward exchange rates. Source: Financial Time Dec 31, 2014. All rates are in foreign currency per dollar. 0.9937 also include speculators, since the future contracts can be bought and sold before the contracts mature. 9. Foreign currency options are contracts that give the buyer the right to buy (call option) or sell (put option) currencies at a specified price within a specific period of time. The strike price is the price at which the owner of the contract has the right to transact. EXERCISES 1. Use Fig. 4.1 to determine whether each of the currencies listed here is selling at a 3-month forward premium or discount against the dollar: a. Pound b. Swiss franc c. Yen d. Canadian dollar 2. Calculate the per annum premium (discount) of a 3-month forward contract on Canadian dollars based on the information in Fig. 4.1. 3. List at least three ways in which a futures contract differs from a forward contract. 4. Assume US corporation XYZ needs to arrange to have 10,000 in 90 days. Discuss the alternatives available to the corporation in meeting this obligation. What factors are important in determining which strat- egy is best? 5. Suppose you are the treasurer of a large US multinational firm that wants to hedge the foreign exchange risk associated with a payable of 1,000,000 UK pound due in 90 days. How many futures contracts would cover your risk? 6. Suppose you are the treasurer of a US multinational firm that wants to hedge the foreign exchange risk associated with your firm's sale of equipment to a Swiss firm worth CHF1,000,000. The receivable is due in 6 months. You want to ensure that Swiss francs are worth at least Forward-Looking Market Instruments 103 $0.90 when the francs are received so you want a strike price of $0.90. How many options contracts do you need to hedge this risk? Do you want a call or put on Swiss francs? What has to happen to the spot rate in 6 months for you to let the option expire? FURTHER READING Raha N D ill out of money market turbulence to FX swapStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Accounting The Impact On Decision Makers

Authors: Gary A Porter, Curtis L Norton

8th Edition

1111534861, 9781111534868