Answered step by step

Verified Expert Solution

Question

1 Approved Answer

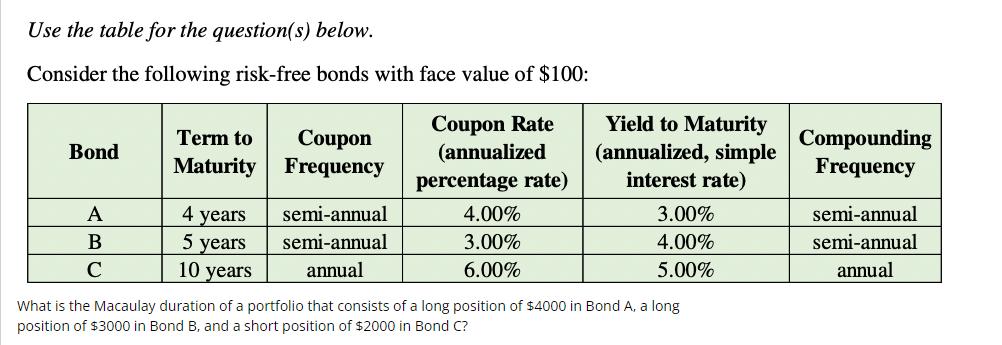

Use the table for the question(s) below. Consider the following risk-free bonds with face value of $100: Bond A B C Term to Coupon

Use the table for the question(s) below. Consider the following risk-free bonds with face value of $100: Bond A B C Term to Coupon Maturity Frequency 4 years 5 years 10 years semi-annual semi-annual annual Coupon Rate (annualized percentage rate) 4.00% 3.00% 6.00% Yield to Maturity (annualized, simple interest rate) 3.00% 4.00% 5.00% What is the Macaulay duration of a portfolio that consists of a long position of $4000 in Bond A, a long position of $3000 in Bond B, and a short position of $2000 in Bond C? Compounding Frequency semi-annual semi-annual annual

Step by Step Solution

There are 3 Steps involved in it

Step: 1

1 Calculate the present value of each bond For the semiannual bond with a 300 coupon rate and a face ...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Fixed Income Analysis

Authors: Barbara S. Petitt

5th Edition

1119850541, 978-1119850540