Answered step by step

Verified Expert Solution

Question

1 Approved Answer

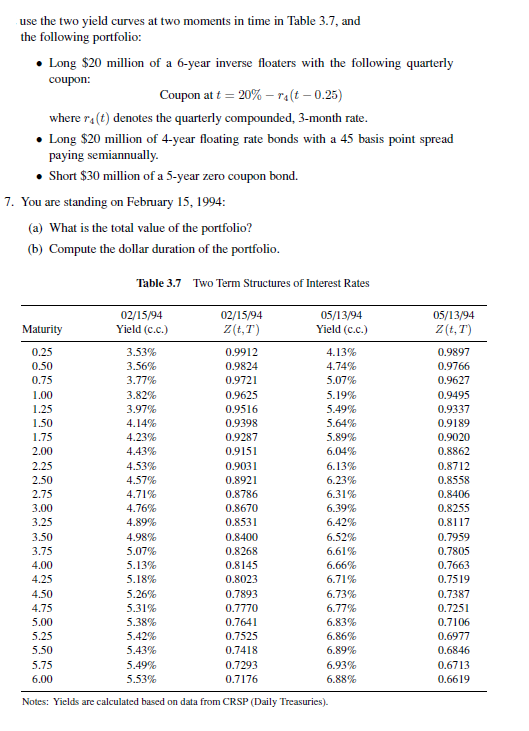

use the two yield curves at two moments in time in Table 3.7 , and the following portfolio: - Long $20 million of a 6-year

use the two yield curves at two moments in time in Table 3.7 , and the following portfolio: - Long \$20 million of a 6-year inverse floaters with the following quarterly coupon: Coupon at t=20%r4(t0.25) where r4(t) denotes the quarterly compounded, 3-month rate. - Long $20 million of 4-year floating rate bonds with a 45 basis point spread paying semiannually. - Short $30 million of a 5-year zero coupon bond. 7. You are standing on February 15, 1994: (a) What is the total value of the portfolio? (b) Compute the dollar duration of the portfolio. Table 3.7 Two Term Structures of Interest Rates Ivotes: rueas are caiculated dased on data Irom Cksr (vally reasuries). use the two yield curves at two moments in time in Table 3.7 , and the following portfolio: - Long \$20 million of a 6-year inverse floaters with the following quarterly coupon: Coupon at t=20%r4(t0.25) where r4(t) denotes the quarterly compounded, 3-month rate. - Long $20 million of 4-year floating rate bonds with a 45 basis point spread paying semiannually. - Short $30 million of a 5-year zero coupon bond. 7. You are standing on February 15, 1994: (a) What is the total value of the portfolio? (b) Compute the dollar duration of the portfolio. Table 3.7 Two Term Structures of Interest Rates Ivotes: rueas are caiculated dased on data Irom Cksr (vally reasuries)

use the two yield curves at two moments in time in Table 3.7 , and the following portfolio: - Long \$20 million of a 6-year inverse floaters with the following quarterly coupon: Coupon at t=20%r4(t0.25) where r4(t) denotes the quarterly compounded, 3-month rate. - Long $20 million of 4-year floating rate bonds with a 45 basis point spread paying semiannually. - Short $30 million of a 5-year zero coupon bond. 7. You are standing on February 15, 1994: (a) What is the total value of the portfolio? (b) Compute the dollar duration of the portfolio. Table 3.7 Two Term Structures of Interest Rates Ivotes: rueas are caiculated dased on data Irom Cksr (vally reasuries). use the two yield curves at two moments in time in Table 3.7 , and the following portfolio: - Long \$20 million of a 6-year inverse floaters with the following quarterly coupon: Coupon at t=20%r4(t0.25) where r4(t) denotes the quarterly compounded, 3-month rate. - Long $20 million of 4-year floating rate bonds with a 45 basis point spread paying semiannually. - Short $30 million of a 5-year zero coupon bond. 7. You are standing on February 15, 1994: (a) What is the total value of the portfolio? (b) Compute the dollar duration of the portfolio. Table 3.7 Two Term Structures of Interest Rates Ivotes: rueas are caiculated dased on data Irom Cksr (vally reasuries) Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Dividend Stocks For Dummies

Authors: Lawrence Carrel

1st Edition

0470466014, 978-0470466018