`Using Excel solve the problem 7, page 204 of your textbook. Make sure all the data and calculation details are demonstrated in excel with explanation so anyone looking at your work can understand what has happened. Just submit your excel file.

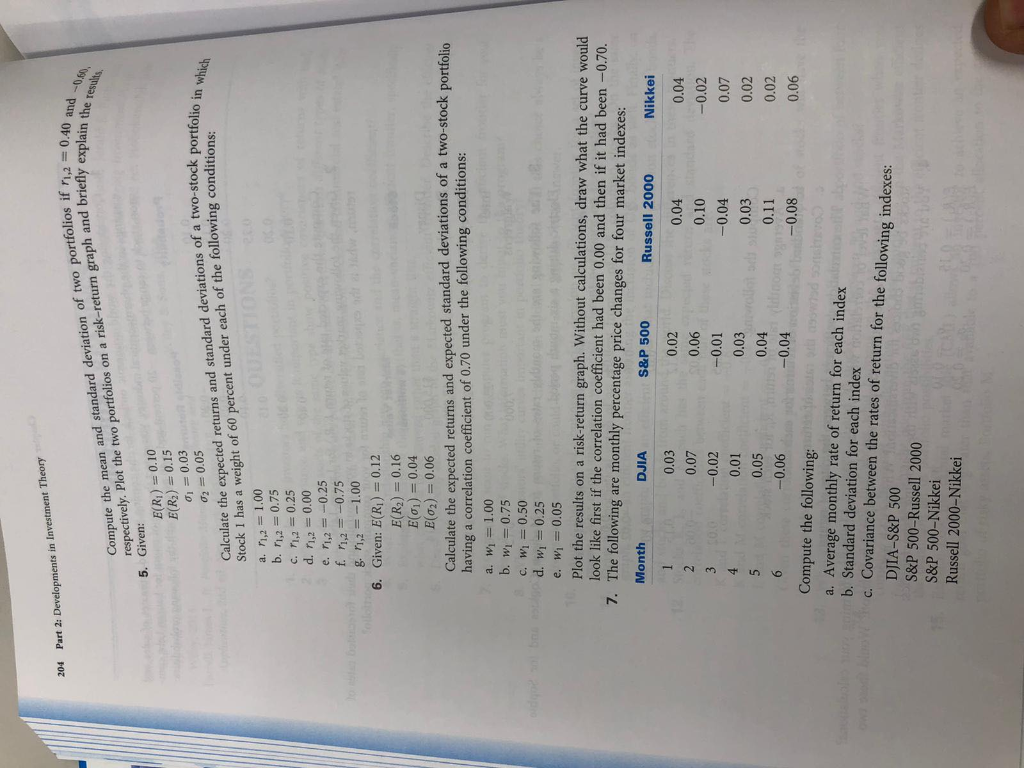

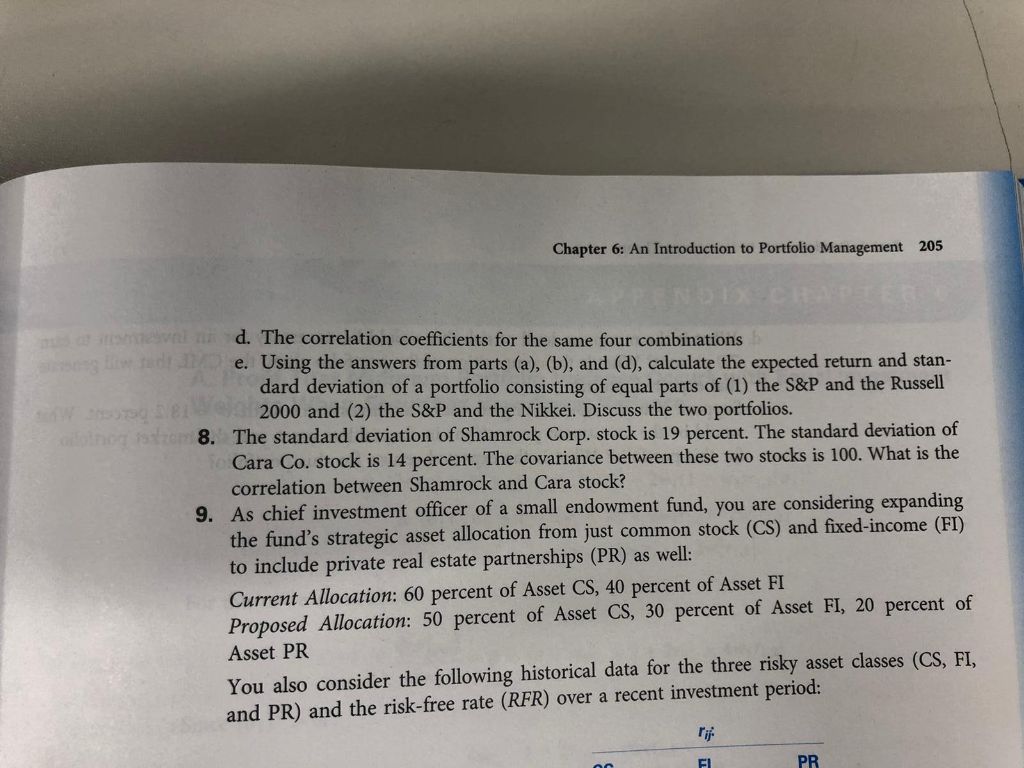

respectively . Plot the two portfolios on a risk - return graph and briefly explain the results Compute the mean and standard deviation of two portfolios if 11,2 = 0.40 and 0 . Calculate the expected returns and standard deviations of a two - stock portfolio in which Part 2: Developments in Investment Theory 204 5. Given: E(R) = 0.10 SE(R) = 0.15 01 = 0.03 02 = 0.05 Stock 1 has a weight of 60 percent under each of the following conditions: a. 1,2 = 1.00 b. 7,2 = 0.75 c. 71,2 = 0.25 1,2 = 0.00 e. "1,2 = -0.25 f. 71,2 = -0.75 8. 71,2 = -1.00 6. Given: E(RI) = 0.12 E(R2) = 0.16 d. 1 E(01) = 0.04 E(02) = 0.06 Calculate the expected returns and expected standard deviations of a two-stock portfolio having a correlation coefficient of 0.70 under the following conditions: a. W = 1.00 b. W = 0.75 c. W 0.50 d. w = 0.25 e. W = 0.05 Plot the results on a risk-return graph. Without calculations, draw what the curve would look like first if the correlation coefficient had been 0.00 and then if it had been -0.70. 7. The following are monthly percentage price changes for four market indexes: Month DJIA S&P 500 Russell 2000 Nikkei 0.03 0.02 0.04 0.04 2 0.07 0.06 -0.02 3 000 -0.02 -0.01 -0.04 0.07 4 0.01 0.03 0.03 0.02 5 0.05 0.04 0.11 0.02 6 -0.06 -0.04 -0.08 0.06 Compute the following: a. Average monthly rate of return for each index b. Standard deviation for each index DJIA-S&P 500 c. Covariance between the rates of return for the following indexes: S&P 500-Russell 2000 S&P 500-Nikkei Russell 2000-Nikkei 0.10 Chapter 6: An Introduction to Portfolio Management 205 vand. The correlation coefficients for the same four combinations gede. Using the answers from parts (a), (b), and (d), calculate the expected return and stan- dard deviation of a portfolio consisting of equal parts of (1) the S&P and the Russell OSOBA 2000 and (2) the S&P and the Nikkei. Discuss the two portfolios. hois 8. The standard deviation of Shamrock Corp. stock is 19 percent. The standard deviation of Cara Co. stock is 14 percent. The covariance between these two stocks is 100. What is the correlation between Shamrock and Cara stock? 9. As chief investment officer of a small endowment fund, you are considering expanding the fund's strategic asset allocation from just common stock (CS) and fixed-income (FI) to include private real estate partnerships (PR) as well: Current Allocation: 60 percent of Asset CS, 40 percent of Asset FI Proposed Allocation: 50 percent of Asset CS, 30 percent of Asset FI, 20 percent of Asset PR You also consider the following historical data for the three risky asset classes (CS, FI, and PR) and the risk-free rate (RFR) over a recent investment period: PR