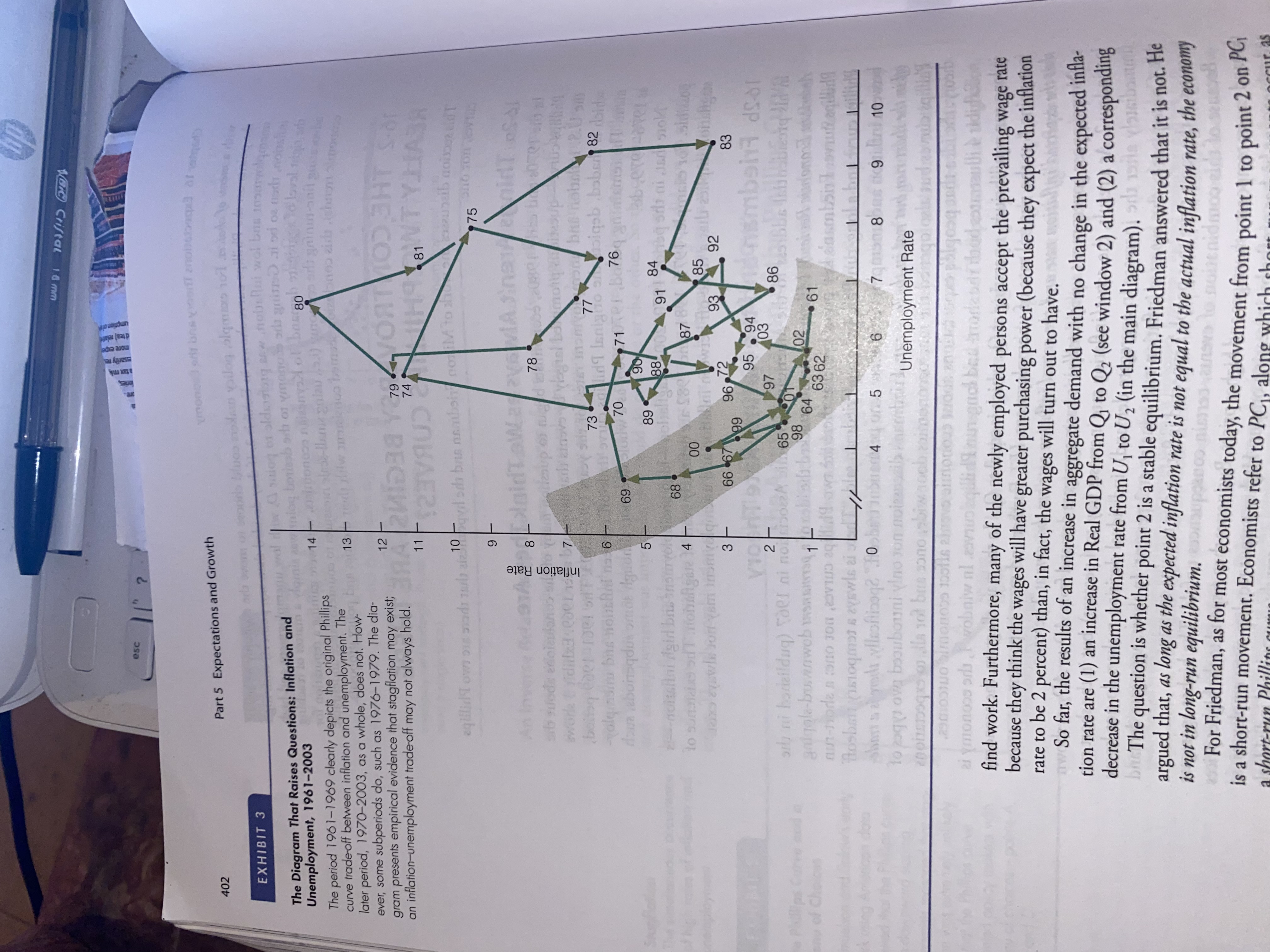

Using Exhibit 3 and Exhibit 4 in Chapter 16 as your guide, can someone help me draw a graph that shows the inflation rate, the unemployment rate, and different short run Phillips Curves based on different inflation expectations.The easiest way to complete this assignment is to scan Exhibit 3 and then draw a few short run Philips curves on it where it seems like the data indicates a group of years must have had consistent inflation expectations.If you want to follow a different strategy in completing the assignment, that's okay.

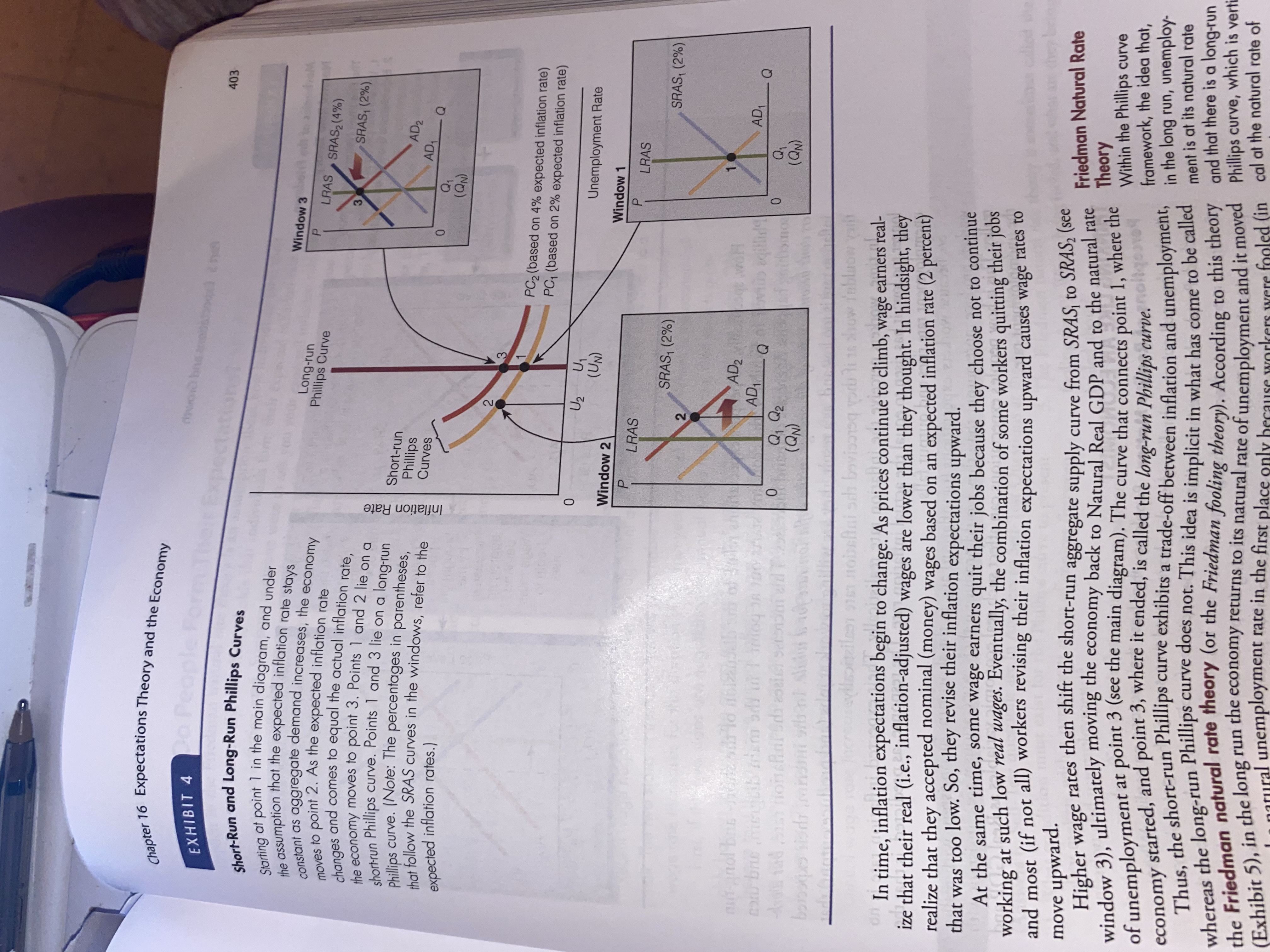

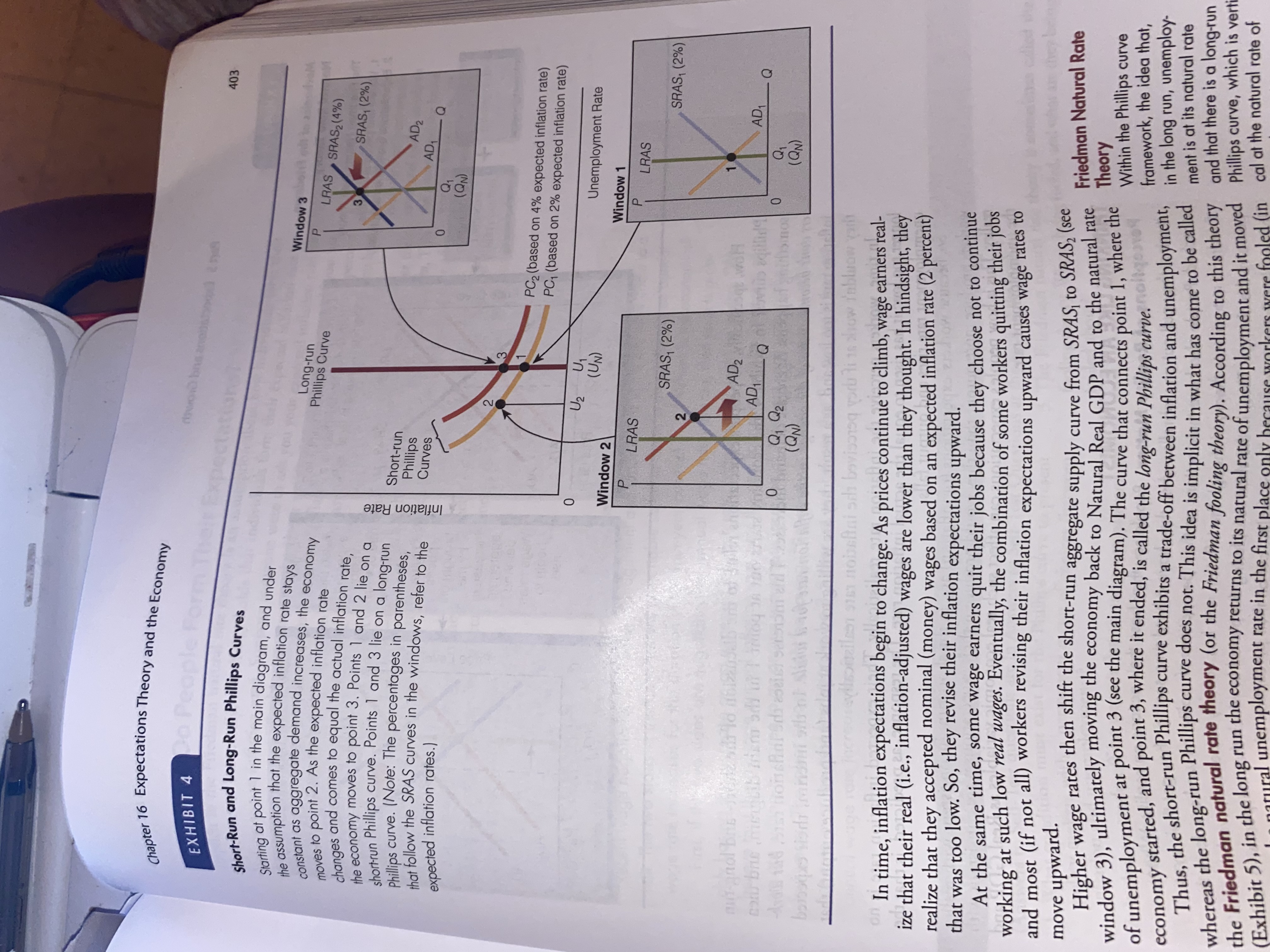

AGIC Cristal 1.8 mm esc 1 1" ? 402 Part 5 Expectations and Growth EXHIBIT 3 The Diagram That Raises Questions: Inflation and many wal log boylesb ofhi of ymonobe oth grind al ad on goth amongits Unemployment, 1961-2003 The period 1961-1969 clearly depicts the original Phillips sidi gainus-ball gue curve trade-off between inflation and unemployment. The 13 later period, 1970-2003, as a whole, does not. How- ever, some subperiods do, such as 1976-1979. The dia- gram presents empirical evidence that stagflation may exist; 12 an inflation-unemployment trade off may not always hold. 2NIDaa V 79.1 VOAT LOS SHT S.Or 11 74 23VAUD no iM to al 75 sho Ton davis 9 An Inverse Bela97/ PlaidToWard MASinew 8 arb sued's endolauionso s loup of me 78 Inflation Rate Bwork didibaseder 7 Viagirl Lo linesup 73 dT Lonly 77 -polqasim bus monthAl no 6 Vbigab .baber 82 doithe down deborraqdue omos Aguon 69 70 ver Ba76q gninismss 5 90 89 dabsero 2- -notisHai dgirl bris ansurge 88 91 84 bg silo ai Jan sick 68 to sunsleds sidT monadgare 4 00 87 leis evawle forf yam momly 85 192 3 66 67 96 83 VIC 95 94 numbshi dsol orh ni barizildaq) toel ni noi 2 97 86 65 andgale-buswnwob INsidingf 98 02 min-horde a tono son leaving aq fidd own Sully 63 62 . 61 fosbringislogmos sayswis ai 7qmoni 8 as a9 Bri 10 to pages ove boubouni vino son nolandally winsmassUnemployment Rate i ymonos sri I wobniw al asviolaquaidYoungnot bad forlabor loud commandline tidurhol find work. Furthermore, many of the newly employed persons accept the prevailing wage rate because they think the wages will have greater purchasing power (because they expect the inflation rate to be 2 percent) than, in fact, the wages will turn out to have. nw So far, the results of an increase in aggregate demand with no change in the expected infla- tion rate are (1) an increase in Real GDP from Q, to Q2 (see window 2) and (2) a corresponding decrease in the unemployment rate from U, to U2 (in the main diagram). Sil mails b The question is whether point 2 is a stable equilibrium. Friedman answered that it is not. He argued that, as long as the expected inflation rate is not equal to the actual inflation rate, the economy is not in long-run equilibrium. For Friedman, as for most economists today, the movement from point I to point 2 on PC Phillis is a short-run movement. Economists refer to PC, along whichChapter 16 Expectations Theory and the Economy EXHIBIT 4 a People 403 Short-Run and Long-Run Phillips Curves starting at point 1 in the main diagram, and under the assumption that the that the expected inflation rate stays Window 3 constant as aggregate demand in hand increases, the economy Long-run moves to point 2. As the expected inflation rate Phillips Curve LRAS SRAS2 (4%) changes and comes to equal the actual inflation rate , the economy moves to point 3. Points 1 and 2 lie on a SRAS, (2%) shortrun Phillips curve. Points 1 and 3 lie on a long-run Phillips curve. (Note: The percentages in parentheses, Short-run Inflation Rate AD2 that follow the SRAS curves in the windows, refer to the Phillips Curves AD expected inflation rates.) 10 - Q Q1 (QN ) 3 PC2 (based on 4% expected inflation rate) PC, (based on 2% expected inflation rate) U2 U1 ( UN ) Unemployment Rate Window 2 Window 1 LRAS LRAS SRAS, (2%) SRAS, (2%) 2 AD2 AD wins egillisle AD -Q - Q 0 Q1 Q 2 (QN) ( QN ) eileen 9181 nobel how I'ablow yard In time, inflation expectations begin to change. As prices continue to climb, wage earners real- ize that their real (i.e., inflation-adjusted) wages are lower than they thought. In hindsight, they realize that they accepted nominal (money) wages based on an expected inflation rate (2 percent) that was too low. So, they revise their inflation expectations upward. At the same time, some wage earners quit their jobs because they choose not to continue working at such low real wages. Eventually, the combination of some workers quitting their jobs and most (if not all) workers revising their inflation expectations upward causes wage rates to move upward. Higher wage rates then shift the short-run aggregate supply curve from SRAS, to SRAS, (see window 3), ultimately moving the economy back to Natural Real GDP and to the natural rate Friedman Natural Rate of unemployment at point 3 (see the main diagram). The curve that connects point 1, where the Theory Within the Phillips curve economy started, and point 3, where it ended, is called the long-run Phillips curve. int, framework, the idea that, Thus, the short-run Phillips curve exhibits a trade-off between inflation and unemployment, in the long run, unemploy whereas the long-run Phillips curve does not. This idea is implicit in what has come to be called ment is at its natural rate the Friedman natural rate theory (or the Friedman fooling theory). According to this theory and that there is a long-run (Exhibit 5), in the long run the economy returns to its natural rate of unemployment and it moved Phillips curve, which is ver Iral unemployment rate in the first place only be poled (in cal at the natural rate of