Answered step by step

Verified Expert Solution

Question

1 Approved Answer

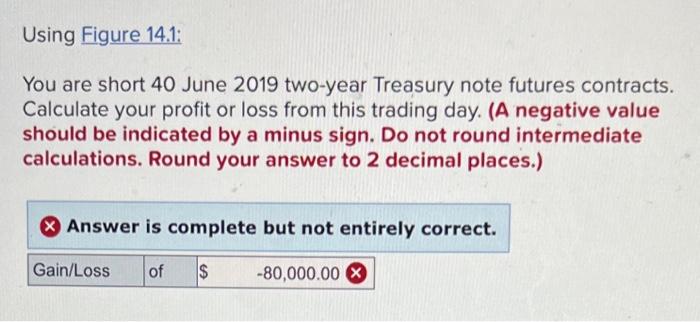

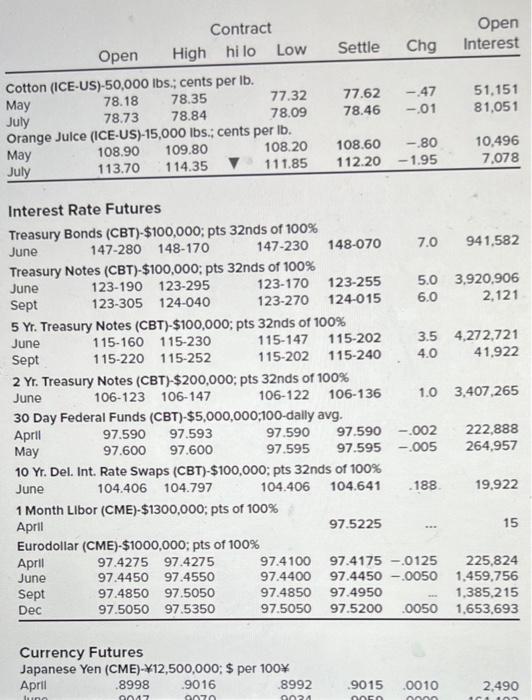

Using Figure 14.1: You are short 40 June 2019 two-year Treasury note futures contracts. Calculate your profit or loss from this trading day. (A negative

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Venture Capital Valuation

Authors: Lorenzo Carver

1st Edition

0470908289, 978-0470908280