Question

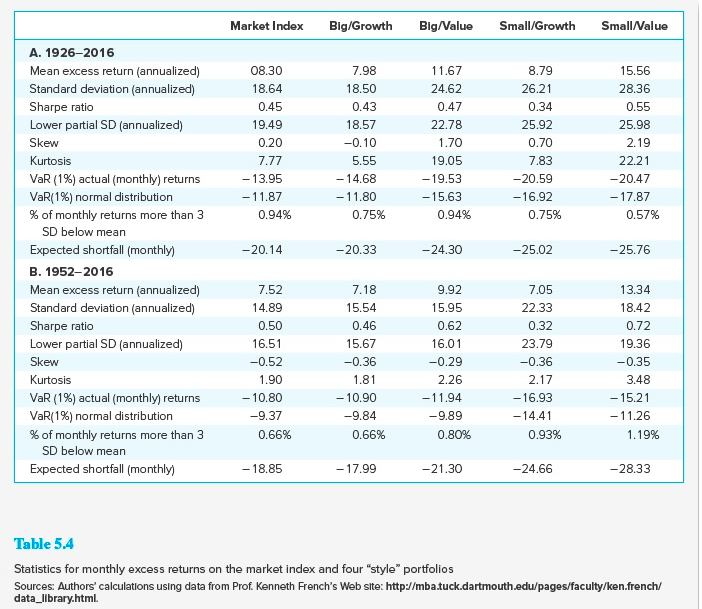

Using historical risk premiums over the 1926-2016 period as your guide, what would be your estimate of the expected annual HPR on the Big/Value portfolio

Using historical risk premiums over the 1926-2016 period as your guide, what would be your estimate of the expected annual HPR on the Big/Value portfolio if the current risk-free interest rate is 3%? Use Table 5.4. (Round your answer to 2 decimal places.)

Using historical risk premiums over the 1926-2016 period as your guide, what would be your estimate of the expected annual HPR on the Big/Value portfolio if the current risk-free interest rate is 3%? Use Table 5.4. (Round your answer to 2 decimal places.)

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Commodity Market Trading And Investment

Authors: Tom James

1st Edition

1137432802, 978-1137432803