Answered step by step

Verified Expert Solution

Question

1 Approved Answer

using the - Black Scholes Model - formual ,find the call option and put option find equation call and put option from BSM by use

using the - Black Scholes Model - formual ,find the call option and put option

find equation call and put option from BSM

by use BSM equation , find equation for ( call option and put option)

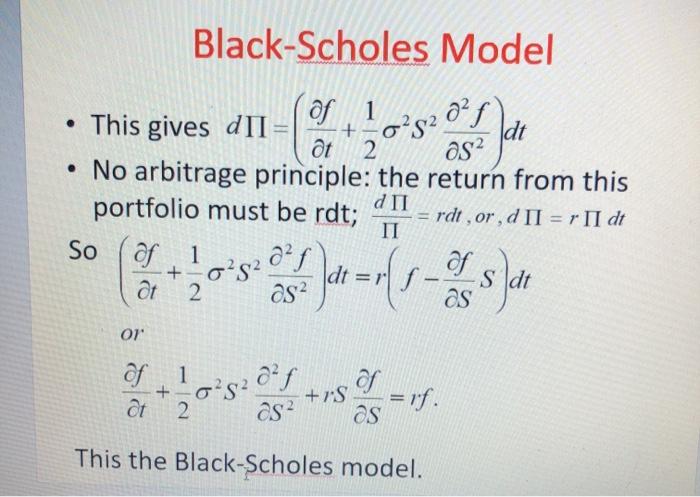

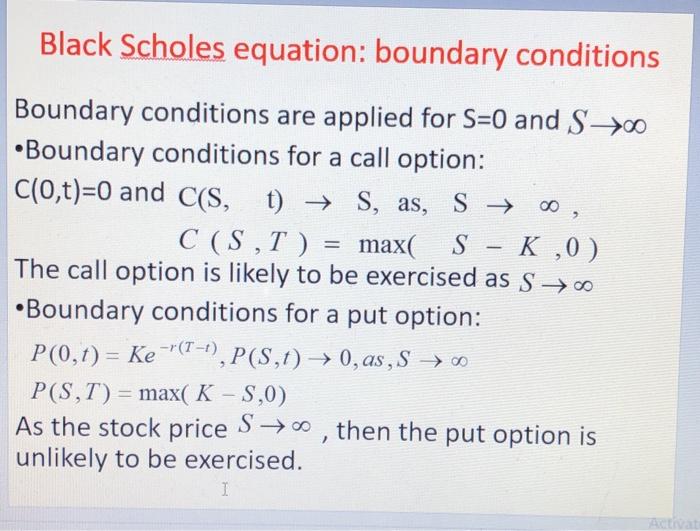

Black-Scholes Model This gives dII of 1 of +-oS at 2 as2 No arbitrage principle: the return from this d II portfolio must be rdt; = rdt, or, d II = r II dt IT So of 1 F Idt = rf S 2 as? as + 092027 at 01 of 1 at 2 + +7S as? = rf as This the Black-Scholes model. Black Scholes equation: boundary conditions Boundary conditions are applied for S=0 and S > Boundary conditions for a call option: C(0,t)=0 and C(S, t) + S, as, S 00, C (S, T ) = max( S - K ,0) The call option is likely to be exercised as S 700 Boundary conditions for a put option: P(0,t) = Ke=(T-1), P(S,1) 0,as, S >00 P(S,T) = max( K -5,0) As the stock price S00, then the put option is unlikely to be exercised. I Black-Scholes Model This gives dII of 1 of +-oS at 2 as2 No arbitrage principle: the return from this d II portfolio must be rdt; = rdt, or, d II = r II dt IT So of 1 F Idt = rf S 2 as? as + 092027 at 01 of 1 at 2 + +7S as? = rf as This the Black-Scholes model. Black Scholes equation: boundary conditions Boundary conditions are applied for S=0 and S > Boundary conditions for a call option: C(0,t)=0 and C(S, t) + S, as, S 00, C (S, T ) = max( S - K ,0) The call option is likely to be exercised as S 700 Boundary conditions for a put option: P(0,t) = Ke=(T-1), P(S,1) 0,as, S >00 P(S,T) = max( K -5,0) As the stock price S00, then the put option is unlikely to be exercised Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Renewable Energy Finance Funding The Future Of Energy

Authors: Charles W Donovan

2nd Edition

1786348594, 9781786348593