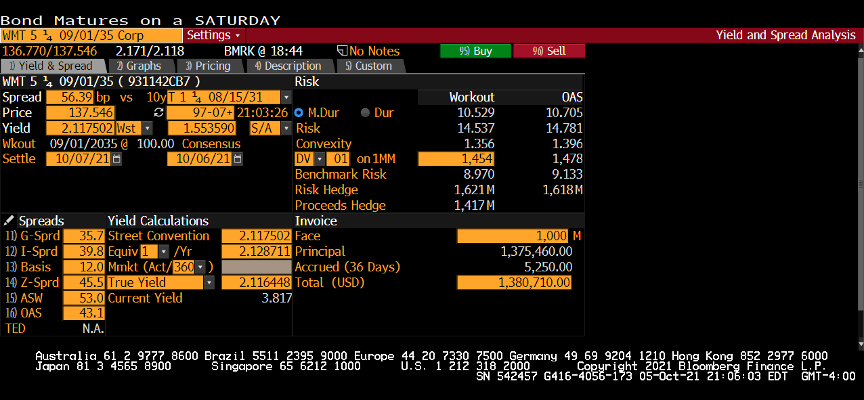

Question

Using the Bloomberg YAS screen below, answer the following questions. (1) Compute the Macaulay duration using the modified duration. (2) What is the DV01 of

Using the Bloomberg YAS screen below, answer the following questions.

(1) Compute the Macaulay duration using the modified duration.

(2) What is the DV01 of the bond for $1,000 par value?

(3) What is the approximate dollar price change for a 50-basis-point decrease in yields for $1,000 par value? You can use the modified duration only.

(4) What is the approximate percentage change in price for a 50-basis-point increase in yields for $1,000 par value? You can use the modified duration only.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Economics Of Money Banking And Financial Markets

Authors: Frederic S. Mishkin

6th Edition

0321113624, 978-0321113627