Answered step by step

Verified Expert Solution

Question

1 Approved Answer

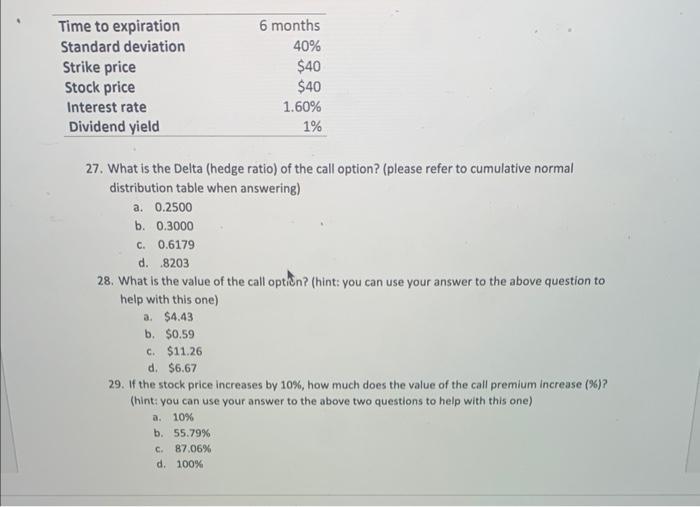

Time to expiration Standard deviation Strike price Stock price Interest rate Dividend yield 6 months 40% $40 $40 1.60% 1% 27. What is the

Time to expiration Standard deviation Strike price Stock price Interest rate Dividend yield 6 months 40% $40 $40 1.60% 1% 27. What is the Delta (hedge ratio) of the call option? (please refer to cumulative normal distribution table when answering) a. 0.2500 b. 0.3000 C. 0.6179 d. 8203 28. What is the value of the call option? (hint: you can use your answer to the above question to help with this one) a. $4.43 b. $0.59 c. $11.26 d. $6.67 29. If the stock price increases by 10%, how much does the value of the call premium increase (%)? (hint: you can use your answer to the above two questions to help with this one) a. 10 % b. 55.79% C. 87.06% d. 100 %

Step by Step Solution

★★★★★

3.41 Rating (160 Votes )

There are 3 Steps involved in it

Step: 1

Q27 c 06179 The delta of a call option is equal to the cumulative normal distribution of the standar...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Elementary Surveying An Introduction to Geomatics

Authors: Charles D. Ghilani, Paul R. Wolf

13th Edition

978-0132554343, 132554348, 978-0273751441