Answered step by step

Verified Expert Solution

Question

1 Approved Answer

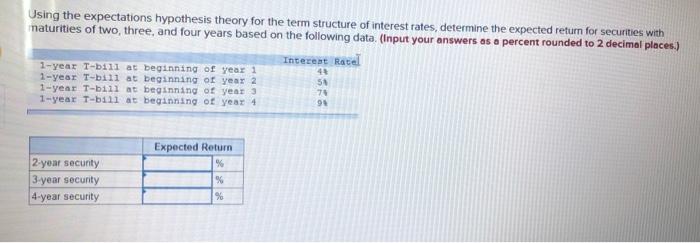

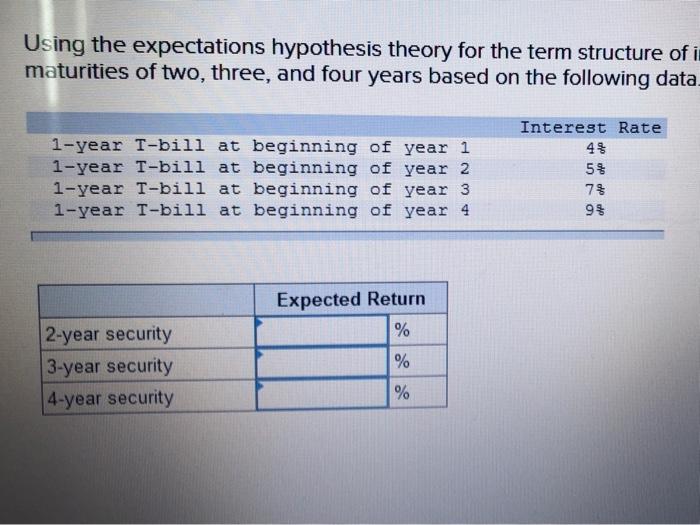

Using the expectations hypothesis theory for the term structure of interest rates, determine the expected return for securities with maturities of two, three, and four

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Chronic Regulatory Focus And Financial Decision Making Asset And Portfolio Allocation

Authors: Navin Kumar

1st Edition

9812876936, 978-9812876935