Answered step by step

Verified Expert Solution

Question

1 Approved Answer

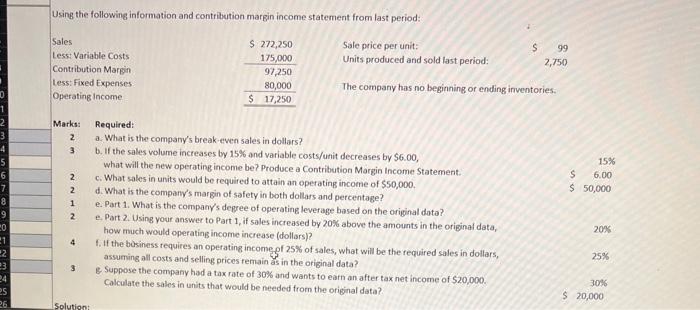

Using the following information and contribution margin income statement from last period: Sales Less: Variable Costs Contribution Margin Less: Fixed Expenses Operating Income Marks:

Using the following information and contribution margin income statement from last period: Sales Less: Variable Costs Contribution Margin Less: Fixed Expenses Operating Income Marks: Required: $ 272,250 175,000 97,250 80,000 $ 17,250 Sale price per unit: Units produced and sold last period: S 99 2,750 The company has no beginning or ending inventories. 1 2 3 2 a. What is the company's break-even sales in dollars? 4 3 5 b. If the sales volume increases by 15% and variable costs/unit decreases by $6.00, what will the new operating income be? Produce a Contribution Margin Income Statement. 6 2 c. What sales in units would be required to attain an operating income of $50,000. 7 2 d. What is the company's margin of safety in both dollars and percentage? 8 1 9 e. Part 1. What is the company's degree of operating leverage based on the original data? 2 20 1 4 2 3 3 24 25 26 Solution: e. Part 2. Using your answer to Part 1, if sales increased by 20% above the amounts in the original data, how much would operating income increase (dollars)? f. If the business requires an operating income of 25% of sales, what will be the required sales in dollars, assuming all costs and selling prices remain as in the original data? Suppose the company had a tax rate of 30% and wants to earn an after tax net income of $20,000. Calculate the sales in units that would be needed from the original data? 15% $ 6.00 $ 50,000 20% 25% 30% $ 20,000

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Intermediate Accounting

Authors: Elizabeth A. Gordon, Jana S. Raedy, Alexander J. Sannella

1st edition

978-0133251579, 133251578, 013216230X, 978-0134102313, 134102312, 978-0132162302