Answered step by step

Verified Expert Solution

Question

1 Approved Answer

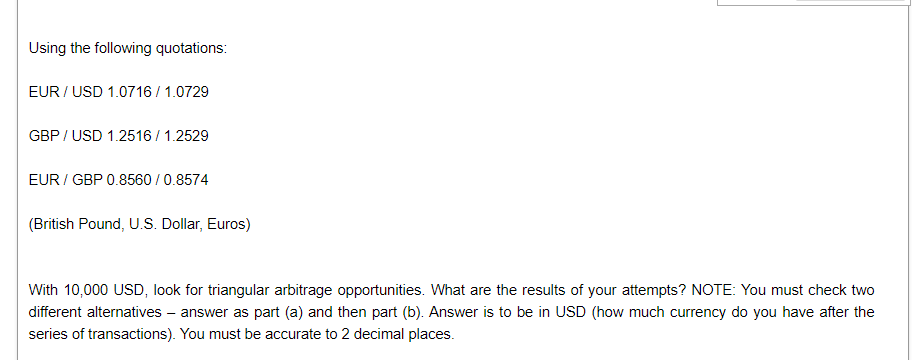

Using the following quotations: EUR/USD 1.0716/1.0729 GBP/USD 1.2516/1.2529 EUR/GBP 0.8560 / 0.8574 (British Pound, U.S. Dollar, Euros) With 10,000 USD, look for triangular arbitrage opportunities.

Using the following quotations: EUR/USD 1.0716/1.0729 GBP/USD 1.2516/1.2529 EUR/GBP 0.8560 / 0.8574 (British Pound, U.S. Dollar, Euros) With 10,000 USD, look for triangular arbitrage opportunities. What are the results of your attempts? NOTE: You must check two different alternatives - answer as part (a) and then part (b). Answer is to be in USD (how much currency do you have after the series of transactions). You must be accurate to 2 decimal places. An Australian exporting company is receiving 30m GBP in two years' time. The current spot rate is AUD/GBP 0.5756 / 0.5774. Australian investment interest rates are currently at 0.85% p.a. and U.K. interest rates are at 1.0% p.a. The net interest rate spread in both countries is 3.5% (read this as the borrowing rates are 3.5% higher than the given investment rates above). Design a money market hedge which will remove the FX risk faced by the Australian company, yet not altering the timing of the payment. Clearly state the AUD cash flow in the future

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Countering Terrorist Finance A Training Handbook For Financial Services

Authors: Tim Parkman, Gill Peeling

1st Edition

0566087251, 978-0566087257