Using the talbes I attached, answer the question. Thank you

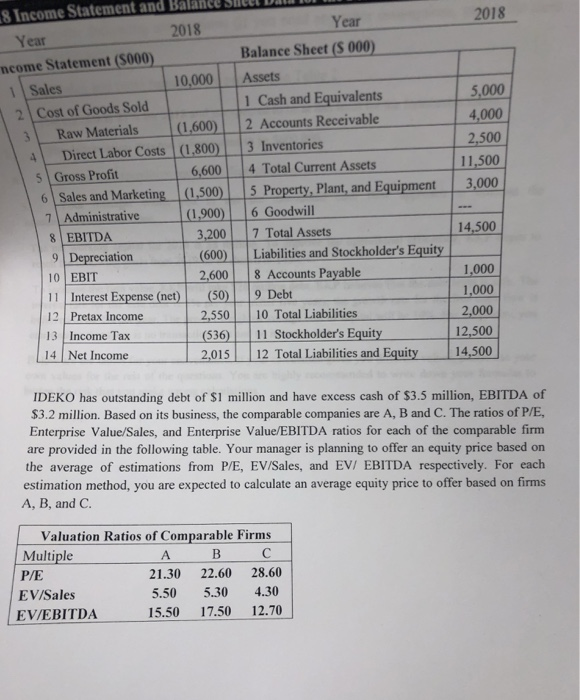

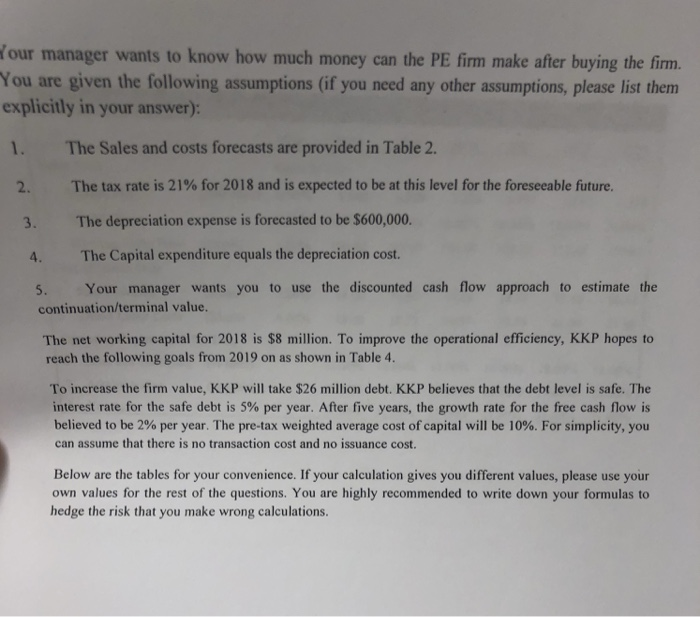

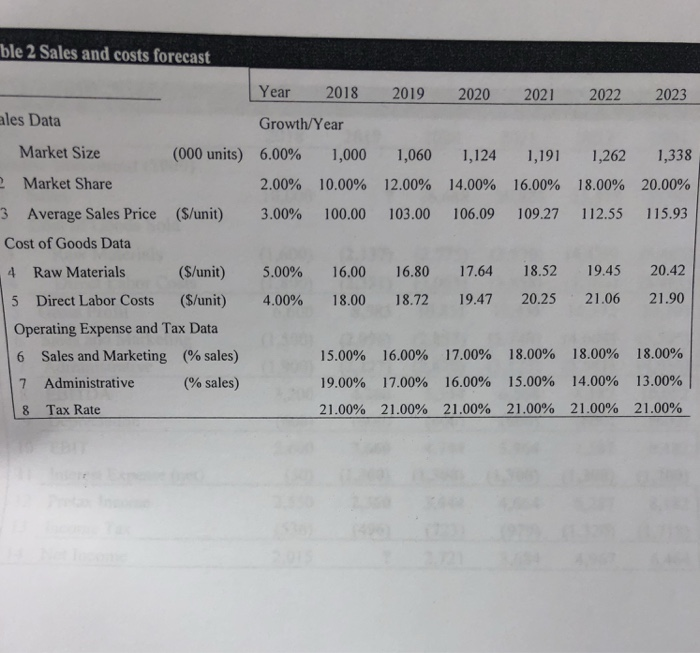

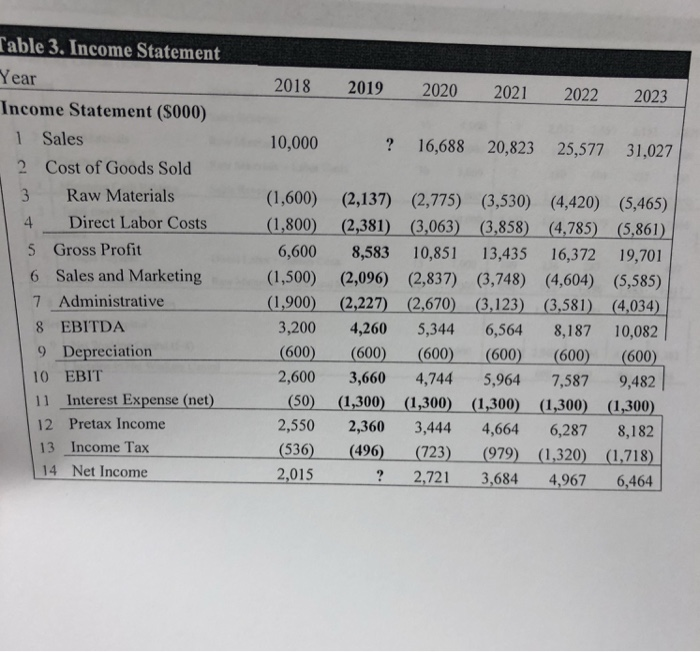

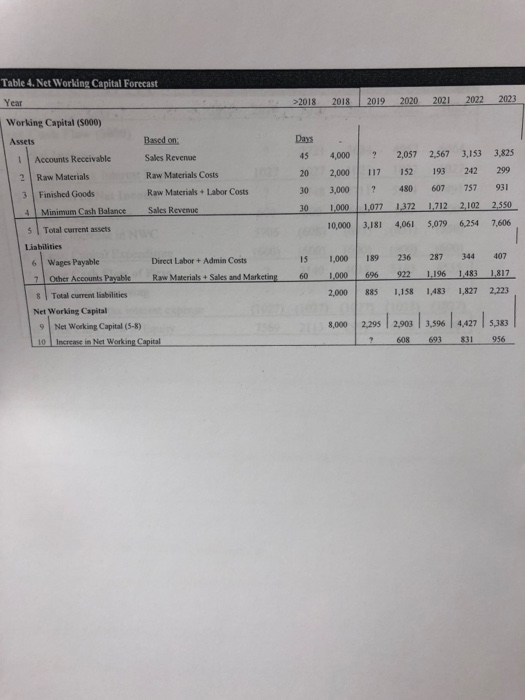

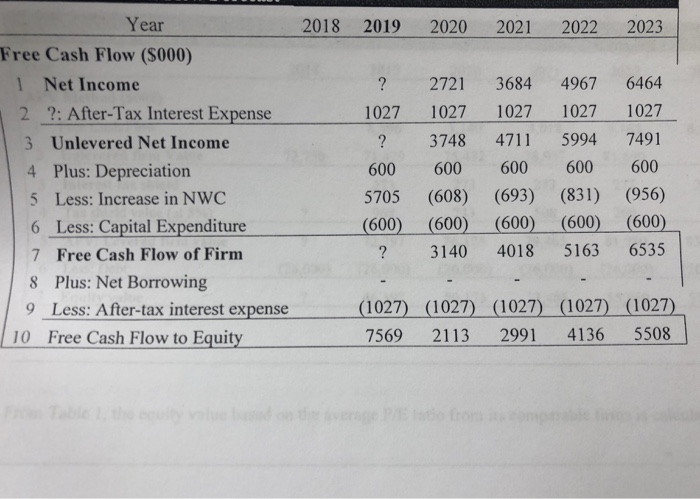

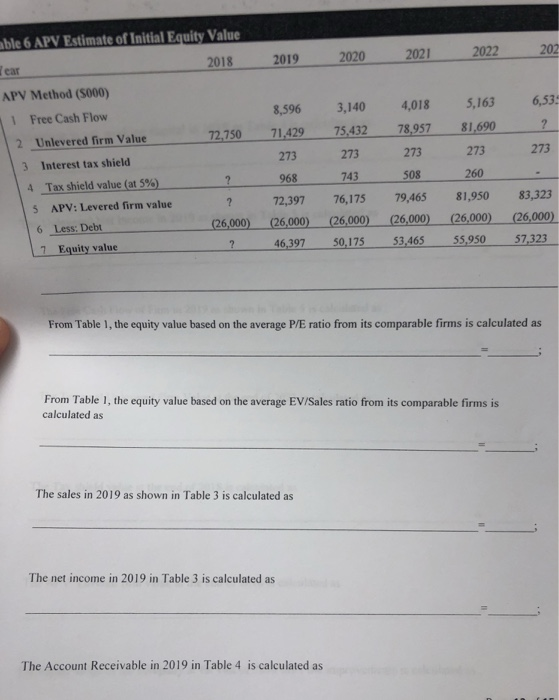

Income Statement and Balance Sleet DI 2018 Year 2018 Year Balance Sheet ($ 000) ncome Statement ($000 10,000Assets 1 | Sales 2 Cost of Goods Sold 5,000 4,000 2,500 11,500 1 Cash and Equivalents Raw Materials (1.600) 2 Accounts Receivable Direct Labor Costs | (1.800) | S Gross Profit 6 Sales and Marketing ,s0o) | 3 inventories 6,600 4 Total Current Assets Property, Plant, and Equipment 3,000 Administrative 8 EBITDA 9 Depreciation 10 EBIT 11 Interest Expense (net)(50) 9 Debt 12 | Pretax Income 13 Income Tax 14 Net Income 1.900) 6 Goodwill 3,200 7 Total Assets (600) Liabilities and Stockholder's Equity 2,600 8 Accounts Payable 14,500 1,000 1,000 2,000 12,500 2,550 10 Total Liabilities (536) 11 Stockholder's Equity 2.015 12 Total Liabilities and Equity 14,500 IDEKO has outstanding debt of S1 million and have excess cash of $3.5 million, EBITDA of $3.2 million. Based on its business, the comparable companies are A, B and C. The ratios of PE, Enterprise Value/Sales, and Enterprise Value/EBITDA ratios for each of the comparable firm are provided in the following table. Your manager is planning to offer an equity price based on the average of estimations from P/E, EV/Sales, and EV/ EBITDA respectively. For each estimation method, you are expected to calculate an average equity price to offer based on firms A, B, and C Valuation Ratios of Comparable Firms MultipleAB C P/E EV/Sales 21.30 22.60 28.60 5.50 5.30 4.30 15.50 17.50 12.70 EVEBITDA 15.50 1750 12.70 our manager wants to know how much money can the PE firm make after buying the firm. You are given the following assumptions (if you need any other assumptions, please list them explicitly in your answer): 1. The Sales and costs forecasts are provided in Table 2 2. The tax rate is 21% for 2018 and is expected to be at this level for the foreseeable future. 3 The depreciation expense is forecasted to be $600,000. 4. The Capital expenditure equals the depreciation cost 5. Your manager wants you to use the discounted cash flow approach to estimate the continuation/terminal value The net working capital for 2018 is $8 million. To improve the operational efficiency, KKP hopes to reach the following goals from 2019 on as shown in Table 4. To increase the firm value, KKP will take $26 million debt. KKP believes that the debt level is safe. The interest rate for the safe debt is 5% per year. After five years, the growth rate for the free cash flow is believed to be 2% per year. The pre-tax weighted average cost of capital will be 10%. For simplicity, you can assume that there is no transaction cost and no issuance cost. Below are the tables for your convenience. If your calculation gives you different values, please use your own values for the rest of the questions. You are highly recommended to write down your formulas to hedge the risk that you make wrong calculations. ble 2 Sales and costs forecast Year 2018 2019 2020 2021 2022 2023 Growth/Year les Data Market Size (000 units) 6.00% 1,000 1,060 1,124 1,191 1,262 1,338 2.00% 10.00% 12.00% 14.00% 16.00% 18.00% 20.00% 3 Average Sales Price ($/unit) 3.00% 100.00 103.00 106.09 109.27 112.55 115.93 Market Share Cost of Goods Data ($/unit) 5.00% 16.00 16.80 17.64 18.52 19.45 20.42 5 Direct Labor Costs ($/unit) 4.00% 18.00 18.72 19.47 20.25 21.06 21.90 4 Raw Materials Operating Expense and Tax Data 6 Sales and Marketing (% sales) 7 Administrative 8 Tax Rate 15.00% 19.00% 21.00% 16.00% 17.00% 21.00% 17.00% 16.00% 21.00% 18.00% 15.00% 21.00% 18.00% 14.00% 21.00% 18.00% 13.00% 21.00% (% sales) Table 3. Income Statement Year Income Statement (S000) 2018 2019 2020 2021 2022 2023 1 Sales 2 Cost of Goods Sold 3 Raw Materials 4 Direct Labor Costs( 10,000 ? 16,688 20,823 25,577 31,027 (1,600) (2,137) (2,775) (3,530) (4,420) (5,465) (1,800) (2,381) (3,063) (3,858) (4,785) (5,861) 6,600 8,583 10,851 13,435 16,372 19,701 (1,500) (2,096) (2,837) (3,748) (4,604) (5,585) (1,900) (2,227) (2,670) (3,123) (3,581) (4,034) 3,200 4,260 5,344 6,564 8,187 10,082 (600) (600) (600) (600) (600) (600) 2,600 3,660 4,744 5,964 7,587 9,482 (50) (1.300) (L.300) (1.300) (1.300) (1.300 2,550 2,360 3,444 4,664 6,287 8,182 536) (496) (723) (979) (1.320) (1,718) 5 Gross Profit 6 Sales and Marketing 7 Administrative 8 EBITDA 9 Depreciation 10 EBIT 11 Interest Expense (aet) 12 Pretax Income 13 income Tax 14 Net Income 2,015 ? 2,721 3,684 4,967 6,464 Table 4. Net Working Capital Forecast Year Working Capital ($000) 2018 2018 2019 2020 2021 2022 2023 Days 4 4,0002,057 2,567 3,153 3,825 Assets Based on: Accoumis Recivale Sabes Revnu Raw Materials Costs Raw Materials+ Labor Costs Sales Revenue 20 2,000 117 152 193 242 299 30 3,000 480 607 757 931 30 1,000 1,077 1372 1,712 2102 2,550 10,000 3,181 4,061 5,079 6,254 7,606 2 Raw Materials 3 Finished Goods 4 Minimum Cash Balance 5 Total current assets Liabilities Direct Labor + Admin Costs S 1,000 89 236 287 344 7 6 Wages Payable Other Accounts Payable Raw Materials+ Sales and Marketing 60 1.000 696 922 1,196 1483 1817 2,000 885 1,158 1,483 1,827 2,223 Total current liabilities Net Working Capital 9 Net Werking Capital (5-8) 0 Increase in Net Working Capital 8,000 2,295 2,903 3,596 4,427 5383 7 608 693831 956 Year 2018 2019 2020 2021 2022 2023 Free Cash Flow ($000) ? 2721 3684 4967 6464 1027 1027 1027 1027 1027 3748 4711 5994 7491 600 600 600 600 600 5705 (608) (693) (831) (956) (600) (600) (600) 3140 4018 5163 6535 1 Net Income 2 ?: After-Tax Interest Expense 3 Unlevered Net Income 4 Plus: Depreciation 5 Less: Increase in NWC 6 Less: Capital Expenditure(600) (600 7 Free Cash Flow of Firm 8 Plus: Net Borrowing 9 Less: After-tax interest expense (1027) (1027) (1027) (1027) (1027) 7569 2113 2991 4136 5508 10 Free Cash Flow to Equity ble 6 APV Estimate of Initial Equity Value ear APV Method ($000) 2018 2019 2020 2021 2022 202 1 8,596 3,140 4,018 5,1636,53 Free Cash Flow 2 72,750 71,429 75,432 78,957 81,690 Unlevered firm Value 273 273 273273 273 Interest tax shield 3 4 743 Tax shield value (at 590 5 , 968 508 260 72,397 76,175 79,465 81,950 83,323 26,000) (26,000) (26,000) 26,000) (26,000)(26,000) 55,950 57.323 APV: Levered firm value 6 Less: Debt Equity value 46,397 50,175 53,465 From Table 1, the equity value based on the average P/E ratio from its comparable firms is calculated as From Table 1, the equity value based on the average EV/Sales ratio from its comparable firms is calculated as The sales in 2019 as shown in Table 3 is calculated as The net income in 2019 in Table 3 is calculated as The Account Receivable in 2019 in Table 4 is calculated as