Answered step by step

Verified Expert Solution

Question

1 Approved Answer

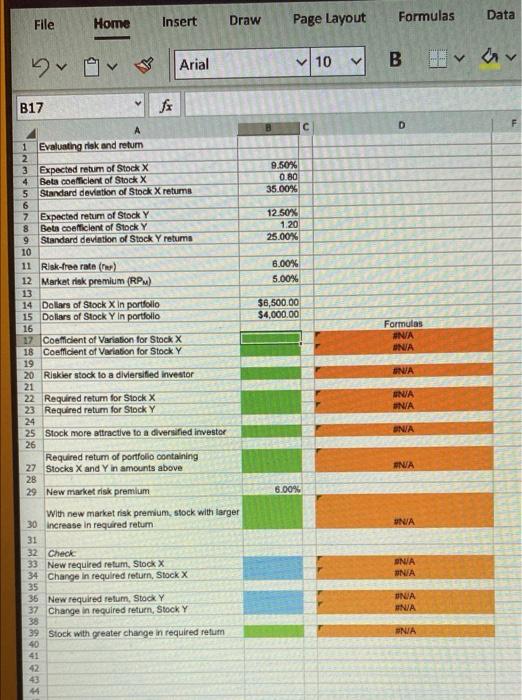

v File Data Home Insert Draw Formulas Page Layout Arial v V10 B B17 fi B D 9.50% 0.80 35.00% 12.50% 1.20 25.00% 6.00% 5.00%

v

File Data Home Insert Draw Formulas Page Layout Arial v V10 B B17 fi B D 9.50% 0.80 35.00% 12.50% 1.20 25.00% 6.00% 5.00% $6,500.00 $4,000.00 Formulas #NA ONA INA A 1 Evaluating risk and retum 2 3 Expected retum of Stock X 4 Beta coefficient of Stock X 5 Standard deviation of Stock X retums 6 7 Expected return of Stock Y 8 Bets coefficient of Stock Y 9 Standard deviation of Stock Y retums 10 11 Risk-free rata () 12 Market risk premium (RPM) 13 14 Dollars of Stock X in portfollo 15 Dollars of Stock Y in portfollo 16 17 Coeficient of Variation for Stock X 18 Coefficient of Variation for Stock Y 19 20 Riskler stock to a diversified investor 21 22 Required return for Stock X 23 Required return for Stock Y 24 25 Stock more attractive to a diversified investor a 26 Required return of portfolio containing 27 Stocks X and Y in amounts above 28 29 New market risk premium with new market risk premium, stock with larger 30 Increase in required retum 31 32 Check 33 New required retum, Stock X 34 Change in required return, Stock 35 36 New required retum. Stock Y 37 Change in required return, Stock Y 38 39 Stock with greater change in required retum 40 41 42 ENJA ONA ONA ANA 6.00% NA ONA #N/A UNA ENIA #NIA 44 Stock X has a 9.5% expected return, a beta coefficient of 0.8, and a 35% standard deviation of expected returns. Stock Y has a 12.5% expected return, a beta coefficient of 1.2, and a 25.0% standard deviation. The risk-free rate is 6%, and the market risk premium is 5%. The data has been collected in the Microsoft Excel Online file below. Open the spreadsheet and perform the required analysis to answer the questions below. X AR Den spreadsheet a. Calculate each stock's coefficient of variation, Round your answers to two decimal places. Do not round intermediate calculations. CV, - CV - b. Which stock is riskier for a diversified investor? 1. For diversified investors the relevant risk is measured by standard deviation of expected returns. Therefore, the stock with the higher standard deviation of expected returns is more risky. Stock X has the higher standard deviation so it is more risky than Stock Y. II. For diversified investors the relevant risk is measured by beta. Therefore, the stock with the lower beta is more risky. Stock X has the lower beta so it is more risky than Stock Y III. For diversified investors the relevant risk is measured by standard deviation of expected returns. Therefore, the stock with the lower standard deviation of expected returns is more risky. Stock Y has the lower standard deviation so it is more risky than Stock X IV. For diversified Investors the relevant risk is measured by beta. Therefore, the stock with the higher beta is less risky. Stock Y has the higher beta so it is less risky than Stock X V. For diversified investors the relevant risk is measured by beta. Therefore, the stock with the higher beta is more risky. Stock Y has the higher beta so it is more risky than Stock X. c. Calculate each stock's required rate of return. Round your answers to two decimal places. Fy d. On the basis of the two stocks' expected and required returns, which stock would be more attractive to a diversified Investor? e. Calculate the required return of a portfolio that has $6,500 invested in Stock X and $4,000 invested in Stock Y. Do not round intermedim calculations. Round your answer to two decimal places. 1. If the market risk premium increased to 6%, which of the two stocks would have the larger increase in its required retur Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Trading And Investing

Authors: John Teall

1st Edition

0123918804, 978-0123918802