Value Stream Mapping Current State Instructions

Create a current state map for the mailroom operation for categories 1-3 (page 6).

Start your value stream map with delivery of the mail to ING.

Additional information: ? Assume 1000 pieces of mail for your inventory calculations

? Receiving and transporting the mail to the mailrooms take 5 min each

? Creating the calculator tapes takes 5 minutes, in 20% of the cases the totals of the two tapes are different

? Manual verification takes 1 minute, totals are rarely wrong.

? Use a weighted average for the processing time of CIFing

? You do not have to calculate total lead time and processing time since some of the processes are performed at the same time, but you need to show the timeline.

? Show how you calculated your times

? Identify at least 2 improvement opportunities Image you would present your value stream map to your boss.

? Pencil is ok, sloppy is not !!!

? Spell-check your work ? If you make assumptions, write them down (or better ask me questions)

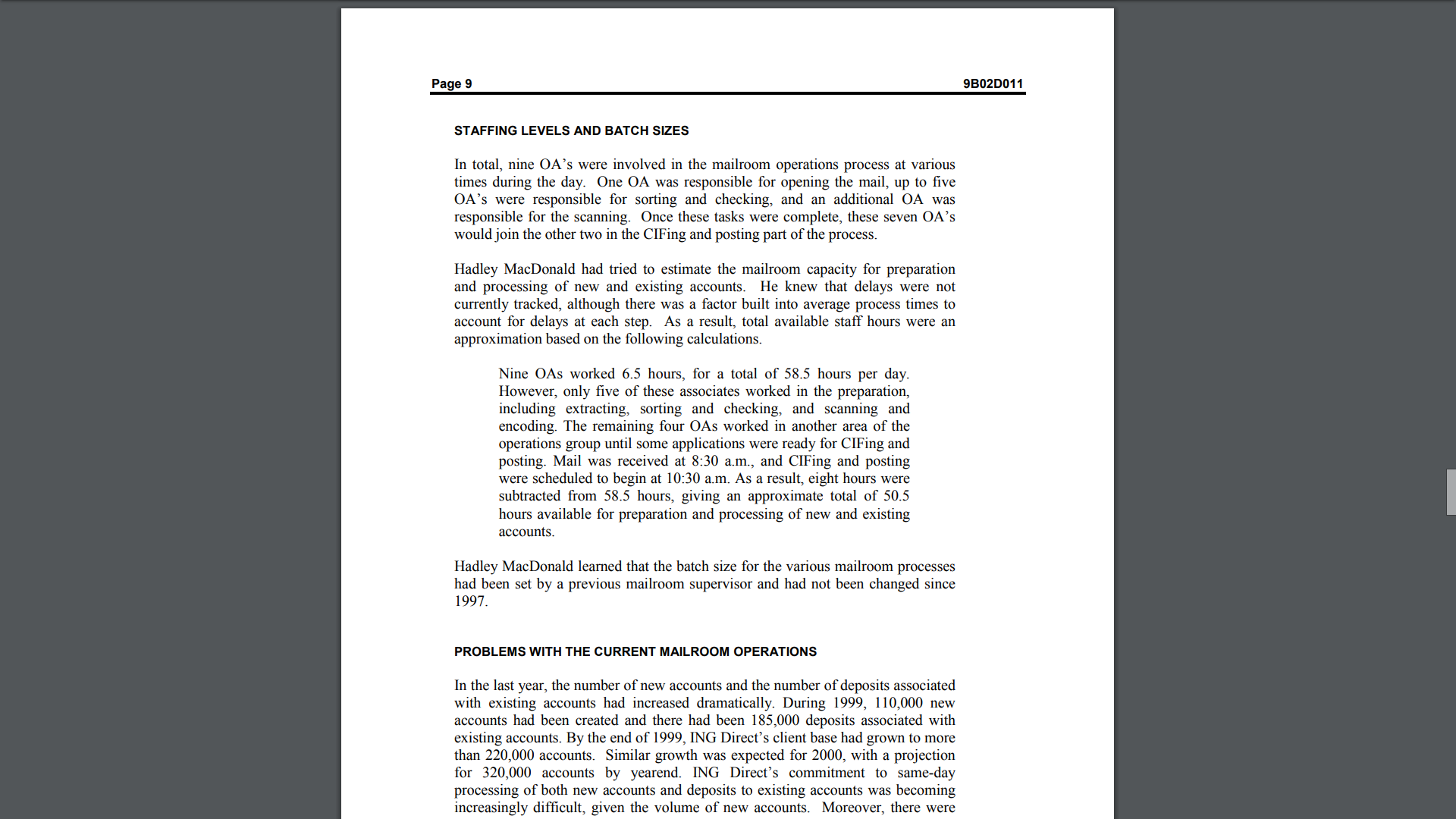

Page 6 9B02D011 Mail Extraction Once the mail was received in the mailroom, an operations associate (OA) fed the mail into the extractor and pre-sorted the mail into the following six categories. 1. Applications and cheques from standard fulfilment and direct mail clients, 2. Cheques from express enrolment clients, 3. Cheques from existing clients, 4. Free-standing inserts from other promotional efforts, 5. Marketing surveys, and 6. Loans. The same OA also performed a preliminary verification on all cheques and applications to ensure that there was no missing or obviously incorrect information. The first category, standard fulfillment and direct mail clients represented about 70 per cent of new clients, did not already have a customer information file (CIF); therefore, their applications would take longer to process. The second category was customers who had a CIF, which was created following a call to the 24-hour call centre or through the Internet. About one-third of the new applications with a CIF were Internet-generated. The last three categories were set aside to be handled by different groups. This process of mail extraction and preliminary verification took approximately 50 minutes per 1,000 pieces of mail. Sorting and Checking Shortly after the extraction process was started, the applications and cheques (i.e., first three categories) were passed to OAs for further sorting and quality checking. Up to five OAs performed these tasks simultaneously. As many as two OAs dealt with the applications and cheques for fulfillment of new clients, while up to three others processed cheques for existing clients. All cheques were sorted according to account type. New client applications within the first two categories were further sortedlonger to process, as the 0A would have to enter information for the secondary or joint account holder who might or might not have a CIF. Applications were grouped into batches of 50, and two calculator tapes of each batch were made to verify totals. During this additional sorting, applications underwent quality checking OAs checked for the client's SIN, telephone number, date of birth and deposit amount. They further checked the body and gure of all cheques and the information relating specically to the various account types (e.g.. customers opening a GIC account had to include the term of investment). The mailroom supervisor also Page 7 93020011 completed signature verication by matching the signature on the cheque with the signature on the application. The entire process of sorting and checking took six person-hours per 1,000 mail pieces. Exceptions were separated during the OM process, prior to batching. All applications and cheques not received in good order (IGO) e.g., no signature on application, cheques stale-dated, or traveilers' cheque instead of personalized cheque - were set aside. All not in good order {NICO} items had to be returned to the client by mail. The number of exceptions was not tracked. Scannlng and Encoding oi Cheques Cheques were next sent to an OA at the NCR 7731 image transport machine for Scanning and Encoding of Cheques Cheques were next sent to an CA at the NCR 7731 image transport machine for imaging and encoding, The DA sent the cheque through the scanner but had to enter the deposit amount of each cheque manually in order to encode it The capacity of the NCR 7731 machine was 30 cheques per minute, although it took the 0A about '15 minutes to process one batch of 50 checks. Software that cost about $100,000 was available to fully automate the seaming and encoding step by the NCR 7731 using intelligent character recognition Manual verication of totals was also performed on the cheques Running batch totals were taken from the scanning machine and compared against the calculator totals run during sorting and checking If the totals balanced, the cheques were taken to the stamping bin for deposit. The cheques were sent to the bank for deposit, even though posting usually occurred much later in the day (posting occurred when a particular cheque was credited to that particular client's account) The NCR 7731 machine hosted a software program called INQUIRE, that held the cheque image, and therefore allowed it to he posted later the same day The CA simply had to sequence the batch number to retain the information for posting purposes. Batches of applications were logged and placed in a tray for ClFing and posting ClFing of New Applications ClFing was the process of either creating or updating the CIF', this process required the manual entry of all client data into the contact management system, called EDGE If the client already had a CIF, then the 0A would go to the look-up screen and enter the client's rst and last name and update the primary account holder's data If the account was a joint account, the 0A would enter the secondary account holder's rst and last name to ensure that no duplicates had already been entered in the system New or updated client relevant data was also entered Once the data entry was complete, the \"setup\" code was indicated to instruct all DA's Page 8 B 302 D01 1 that the client's account was active and ready for personal identication (PIN and password). If the client did not have a CIF, then one had to be created prior to data entry First, the 0A would input the client's rst and last name to verify that no duplicates had already been entered into the system, Joint account information was also entered, if applicable Once the data had been entered, the 0A would switch to the \"Prole" system (a generic banking system used worldwide) to create the new account, The DA would then enter the client's new C117. the product type, the currency code, Canadian or US, dollars, the relationship code (single, joint), and the branch code Once completed, the 0A would transfer the application m another 0A for posting of the cheque Process times for ClFing varied, depending on whether or not the creation of a CIF was required and further on the type of account requested by the client For single accounts requiring the creation of a CIF (about 30 per cent of all new accounts), processing took 175 person-hours per batch of 50 applications For joint accounts requiring the creation of a CIF, about 40 per cent of all new accounts, processing times equalled 2.5 person-hours per batch of 50. Single accounts that already had a CIF (about 10 per cent of all new accounts), took 140 person-hours per batch of 50, Joint accounts with a CIF (about 20 per cent of all new accounts) took 1,75 person-hours per batch of 50, Posting of cheques Aer completion of all ClFing, the OA's would use the lNQUlRE system to post the cheques The posting of cheques required three primary steps: (1) open the CIF on the contact management system, (2) set up deposit details term, amount, interest management and maturity and (3) post transactions to client's accounts. To post a cheque, the 0A had to access the appropriate screen and then enter the cheque amount and the account number of the client, For new clients. external bank information held in the lNQUlRE system was also linked to the account holder, This step for new clients took approximately 125 person-hours per batch of 50, double the time it took to process deposits for existing clients Posting for existing clients was much simpler. as the client's external bank information was already linked, Thus, deposits for existing clients took half the time, Page 5 5 30: D01 1 STAFFING LEVELS AND BATCH SIZES In total, nine OA's were involved in the mailroom operations process at various times during the day. One 0A was responsible for opening the mail, up to ve OA's were responsible for sorting and checking, and an additional 0A was responsible for the seaming Once these tasks were complete, these seven OA's would join the other two in the ClFing and posting part of the process. Hadley MacDonald had tried to estimate the mailroom capacity for preparation and processing of new and existing accounts He knew that delays were not currently tracked, although there was a factor built into average process times to account for delays at each step As a result, total available staff hours were an approximation based on the following calculations Nine 0A5 worked 65 hours, for a total of 585 hours per day, However, only five of these associates worked in the preparation, including extracting, sorting and checking, and scanning and encoding. The remaining four OAs worked in another area of the operations group until some applications were ready for ClFing and posting, Mail was received at 8:30 a m,, and ClFing and posting were scheduled to begin at 10:30 am. As a result eight hours were subtracted from 585 hours, giving an approximate total of 505 hours available for preparation and processing of new and existing accounts, Hadley MacDonald learned that the batch size for the various mailroom processes had been set by a previous mailroom supervisor and had not been changed since 1997, PROBLEMS WITH THE CURRENT MAJLRDOM OPERA1|DNS In the last year, the number of new accounts and the number of deposits associated with existing accounts had increased dramatically During 1999, 110,000 new accounts had been created and there had been 185,000 deposits associated with existing accounts, By the end of 1999, ING Direct's client base had grown to more than 220,000 accounts, Similar growth was expected for 2000. with a projection for 320,000 accounts by yearend ING Direct's commitment to same-day processing of both new accounts and deposits to existing accounts was becoming increasingly difcult, given the volume of new accounts, Moreover, there were