Answered step by step

Verified Expert Solution

Question

1 Approved Answer

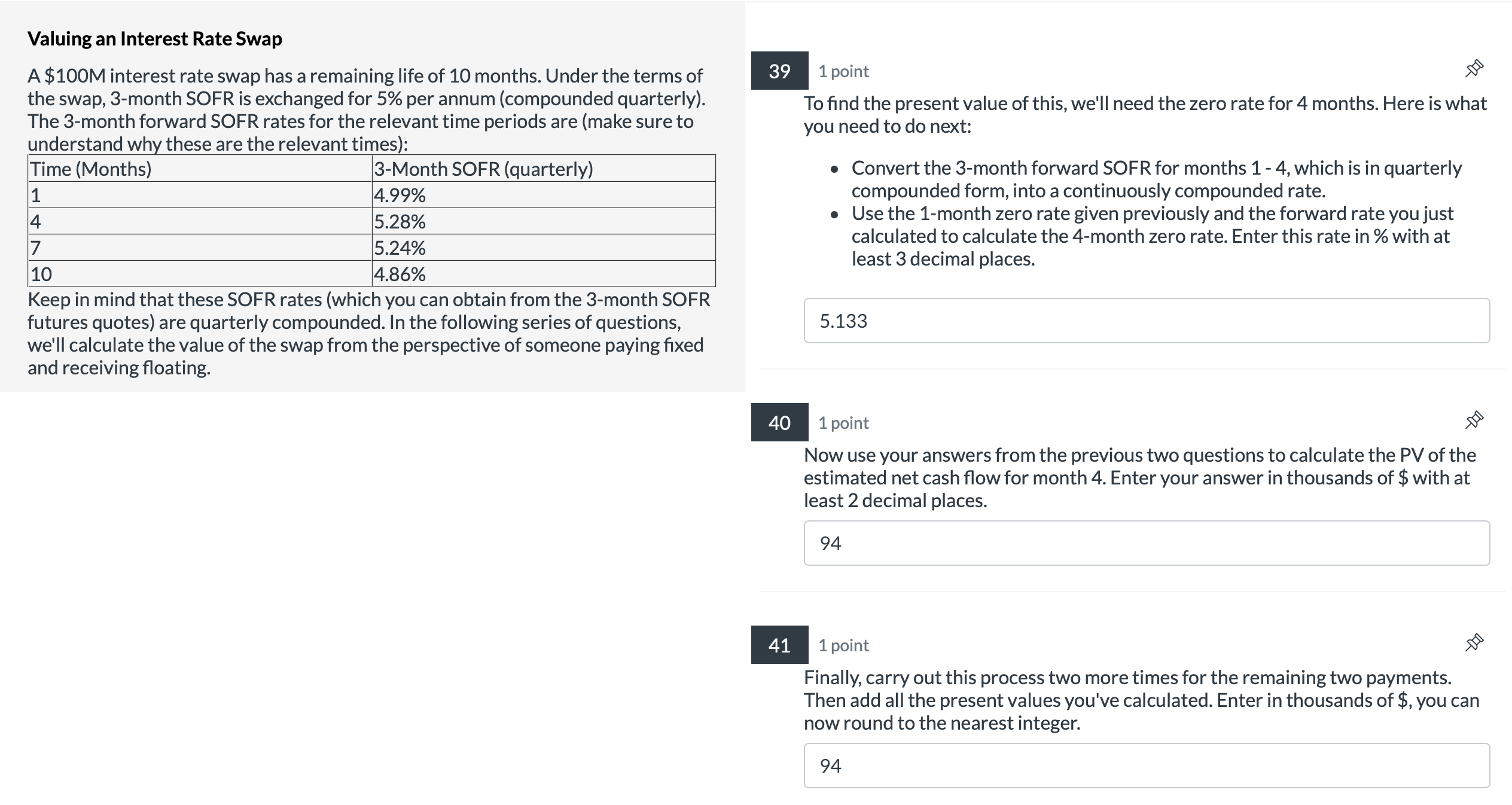

Valuing an Interest Rate Swap A $ 1 0 0 M interest rate swap has a remaining life of 1 0 months. Under the terms

Valuing an Interest Rate Swap

A $M interest rate swap has a remaining life of months. Under the terms of

the swap, month SOFR is exchanged for per annum compounded quarterly

The month forward SOFR rates for the relevant time periods are make sure to

understand why these are the relevant times:

Keep in mind that these SOFR rates which you can obtain from the month SOFR

futures quotes are quarterly compounded. In the following series of questions,

we'll calculate the value of the swap from the perspective of someone paying fixed

and receiving floating.

To find the present value of this, we'll need the zero rate for months. Here is what

you need to do next:

Convert the month forward SOFR for months which is in quarterly

compounded form, into a continuously compounded rate.

Use the month zero rate given previously and the forward rate you just

calculated to calculate the month zero rate. Enter this rate in with at

least decimal places.

Now use your answers from the previous two questions to calculate the PV of the

estimated net cash flow for month Enter your answer in thousands of $ with at

least decimal places.

Finally, carry out this process two more times for the remaining two payments.

Then add all the present values you've calculated. Enter in thousands of $ you can

now round to the nearest integer.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Multinational Finance

Authors: Kirt C. Butler

3rd Edition

0324177453, 978-0324177459