Answered step by step

Verified Expert Solution

Question

1 Approved Answer

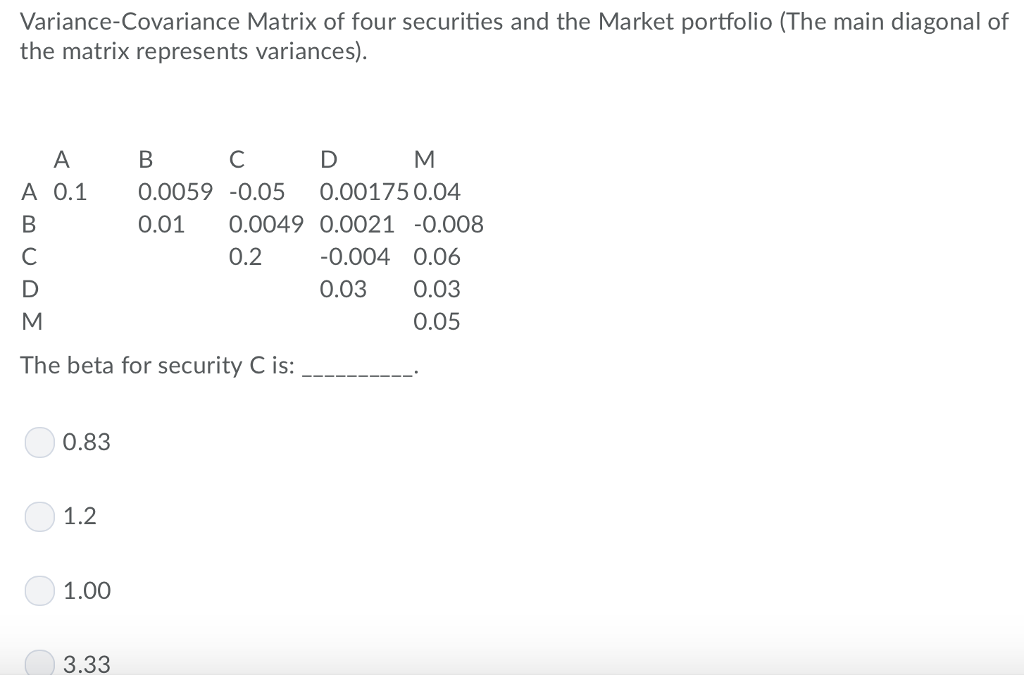

Variance-Covariance Matrix of four securities and the Market portfolio (The main diagonal of the matrix represents variances) A B A 0.1 0.0059 -0.05 0.001750.04 0.01

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Role Of Internal Auditing In A Federal Educational Institution Management Support And Decision Making Aid

Authors: Leonardo Gonçalves

1st Edition

6205061759, 978-6205061756