Answered step by step

Verified Expert Solution

Question

1 Approved Answer

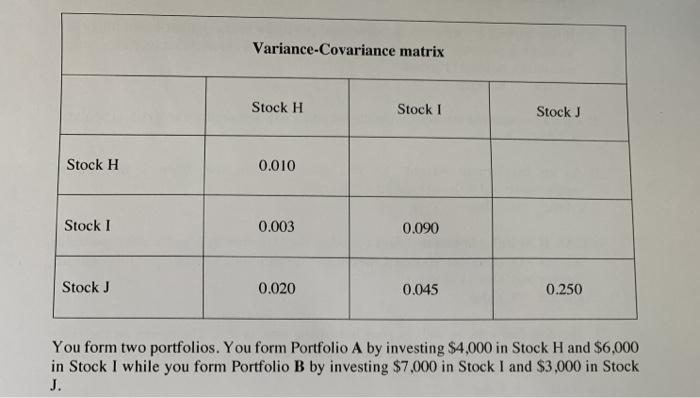

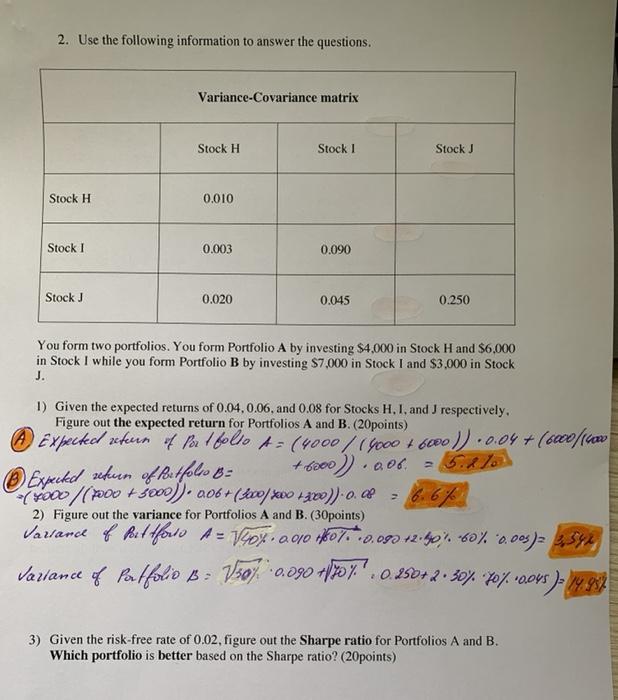

Variance-Covariance matrix Stock H Stock I Stock Stock H 0.010 Stock I 0.003 0.090 Stock J 0.020 0.045 0.250 You form two portfolios. You form

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Management In The Sport Industry

Authors: Matthew T Brown, Daniel Rascher, Mark S Nagel, Chad Mcevoy

1st Edition

1934432040, 978-1934432044