Answered step by step

Verified Expert Solution

Question

1 Approved Answer

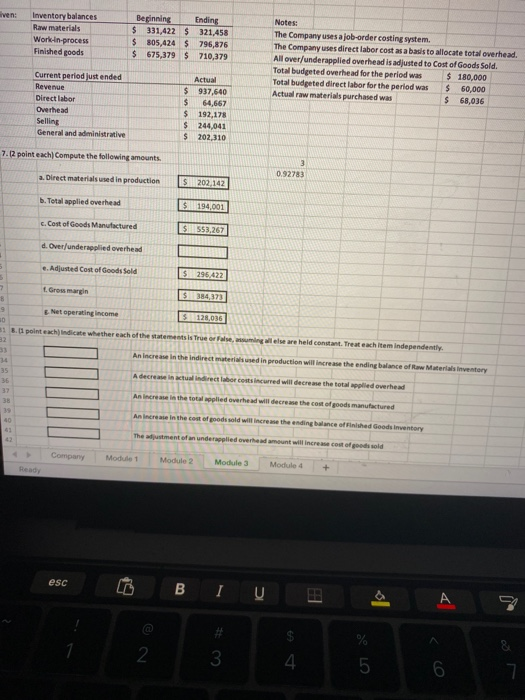

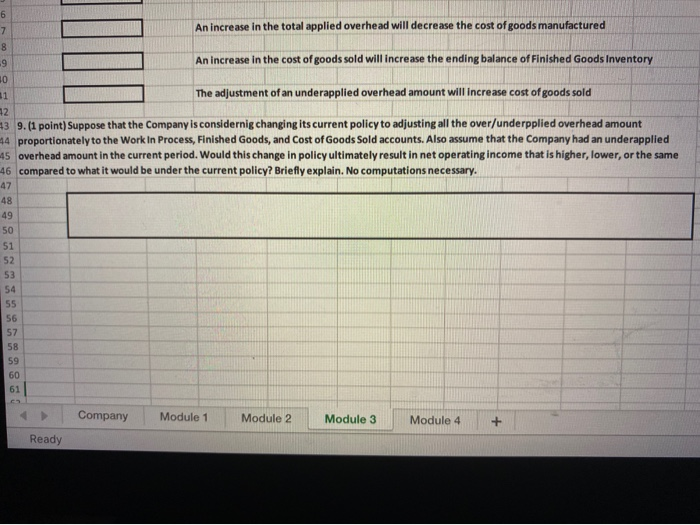

ven: Inventory balances Raw materials Work in process Finished goods Beginning Ending $ 331,4225 321,458 $ 805,424 $ 796,876 $ 675,379 $ 710,379 Notes: The

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Place Of Internal Audit And Management Control In Performance The Case Of The Bank

Authors: Hind Ben Khayat

1st Edition

6205968371, 978-6205968376