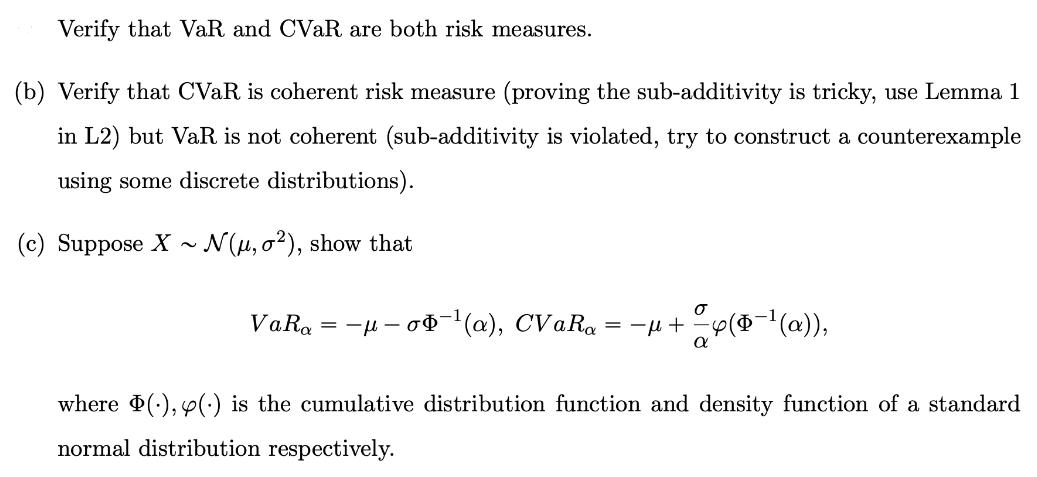

Verify that VaR and CVaR are both risk measures. (b) Verify that CVaR is coherent risk measure (proving the sub-additivity is tricky, use Lemma

Verify that VaR and CVaR are both risk measures. (b) Verify that CVaR is coherent risk measure (proving the sub-additivity is tricky, use Lemma 1 in L2) but VaR is not coherent (sub-additivity is violated, try to construct a counterexample using some discrete distributions). (c) Suppose XN(, o2), show that VaRa = --(a), CVaRa = = + y($(a)), where (), y() is the cumulative distribution function and density function of a standard normal distribution respectively.

Step by Step Solution

3.35 Rating (164 Votes )

There are 3 Steps involved in it

Step: 1

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Authors: Philippe Jorion

3rd edition

0070700427, 71464956, 978-0071464956