Answered step by step

Verified Expert Solution

Question

1 Approved Answer

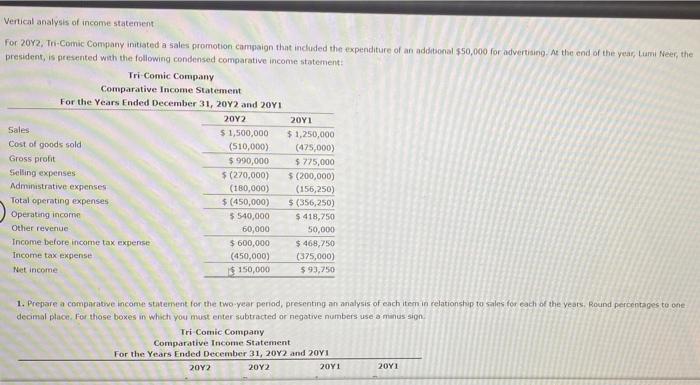

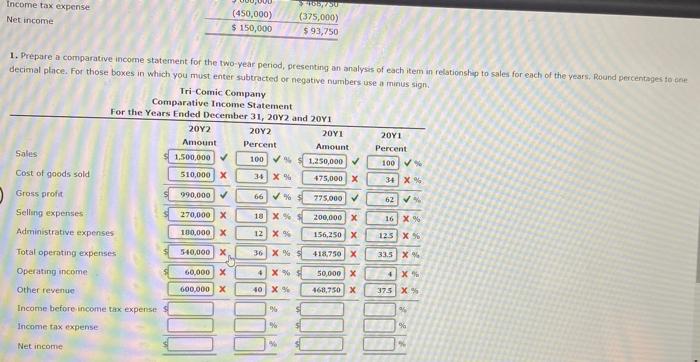

Vertical analysis of income statement For 2012, Tri-Comic Company initiated a sales promotion campaign that included the expenditure of an additional $50,000 for advertising. At

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Development Institutions Growth And Poverty Reduction

Authors: Basudeb Guha Khasnobis, George Mavrotas

2008 Edition

0230201776, 978-0230201774