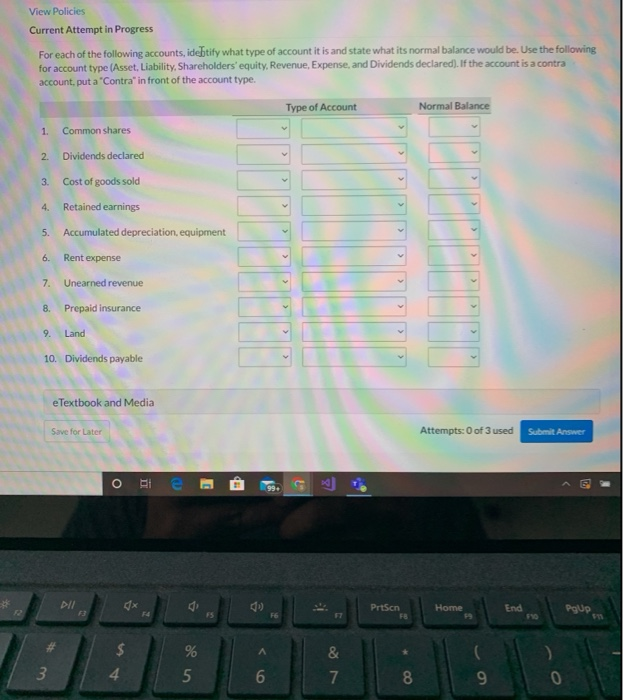

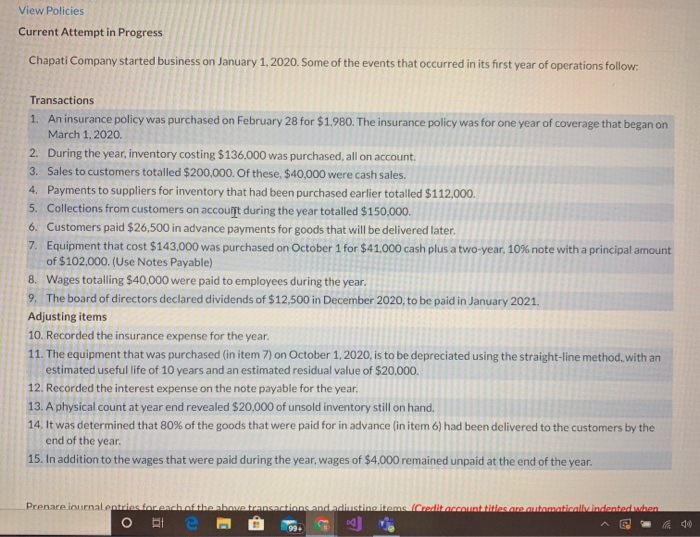

View Policies Current Attempt in Progress For each of the following accounts, ideftify what type of account it is and state what its normal balance would be. Use the following for account type (Asset, Liability, Shareholders' equity, Revenue, Expense, and Dividends declared). If the account is a contra account, put a 'Contra" in front of the account type. Type of Account Normal Balance 1. Common shares Dividends declared N 3 Cost of goods sold 4. Retained earnings 5. Accumulated depreciation, equipment 6. Rent expense 7. Unearned revenue 8. Prepaid insurance 9. Land 10. Dividends payable eTextbook and Media Save for Later Attempts: 0 of 3 used Submit Answer O I e 99+ Dll PrtScn FB Home End 74 FS F6 10 Poup om % 5 & 7 4 6 8 9 View Policies Current Attempt in Progress Chapati Company started business on January 1, 2020. Some of the events that occurred in its first year of operations follow: Transactions 1. An insurance policy was purchased on February 28 for $1.980. The insurance policy was for one year of coverage that began on March 1, 2020 2. During the year, inventory costing $136,000 was purchased, all on account. 3. Sales to customers totalled $200,000. Of these, $40,000 were cash sales. 4. Payments to suppliers for inventory that had been purchased earlier totalled $112,000. 5. Collections from customers on account during the year totalled $150,000. 6. Customers paid $26,500 in advance payments for goods that will be delivered later. 7. Equipment that cost $143,000 was purchased on October 1 for $41,000 cash plus a two-year, 10% note with a principal amount of $102,000. (Use Notes Payable) 8. Wages totalling $40,000 were paid to employees during the year. 9. The board of directors declared dividends of $12,500 in December 2020, to be paid in January 2021. Adjusting items 10. Recorded the insurance expense for the year. 11. The equipment that was purchased (in item 7) on October 1, 2020, is to be depreciated using the straight-line method with an estimated useful life of 10 years and an estimated residual value of $20,000. 12. Recorded the interest expense on the note payable for the year. 13. A physical count at year end revealed $20,000 of unsold inventory still on hand. 14. It was determined that 80% of the goods that were paid for in advance (in item 6) had been delivered to the customers by the end of the year. 15. In addition to the wages that were paid during the year, wages of $4,000 remained unpaid at the end of the year. Prepare ournal entries for each of the above transactions anddinsting items (Credit account titles are automaticallindented when ORL e