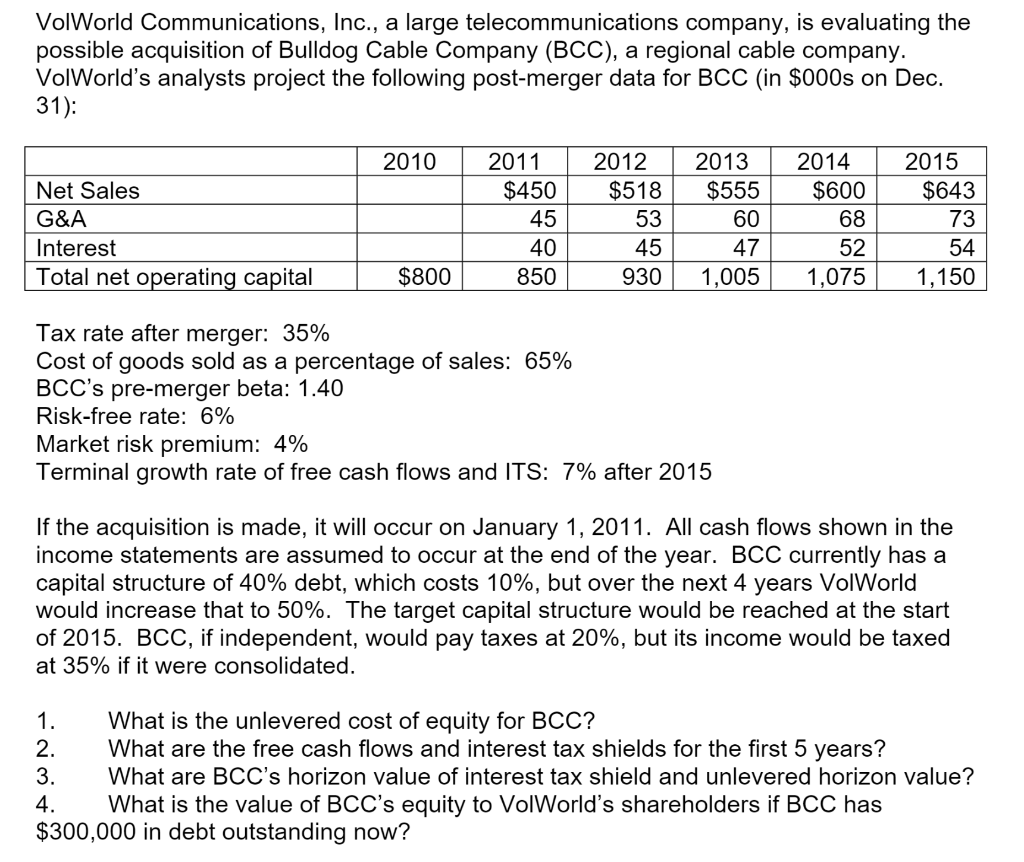

VolWorld Communications, Inc., a large telecommunications company, is evaluating the possible acquisition of Bulldog Cable Company (BCC), a regional cable company. VolWorld's analysts project the following post- merger data for BCC (in $000s on Dec. 31): 2010 Net Sales G&A Interest Total net operating capital 2011 $450 45 40 850 2012 $518 53 45 930 2013 $555 60 47 1,005 2014 $600 68 52 1,075 2015 $643 73 54 1,150 $800 Tax rate after merger: 35% Cost of goods sold as a percentage of sales: 65% BCC's pre-merger beta: 1.40 Risk-free rate: 6% Market risk premium: 4% Terminal growth rate of free cash flows and ITS: 7% after 2015 If the acquisition is made, it will occur on January 1, 2011. All cash flows shown in the income statements are assumed to occur at the end of the year. BCC currently has a capital structure of 40% debt, which costs 10%, but over the next 4 years VolWorld would increase that to 50%. The target capital structure would be reached at the start of 2015. BCC, if independent, would pay taxes at 20%, but its income would be taxed at 35% if it were consolidated. 1. What is the unlevered cost of equity for BCC? 2. What are the free cash flows and interest tax shields for the first 5 years? 3. What are BCC's horizon value of interest tax shield and unlevered horizon value? 4. What is the value of BCC's equity to VolWorld's shareholders if BCC has $300,000 in debt outstanding now? VolWorld Communications, Inc., a large telecommunications company, is evaluating the possible acquisition of Bulldog Cable Company (BCC), a regional cable company. VolWorld's analysts project the following post- merger data for BCC (in $000s on Dec. 31): 2010 Net Sales G&A Interest Total net operating capital 2011 $450 45 40 850 2012 $518 53 45 930 2013 $555 60 47 1,005 2014 $600 68 52 1,075 2015 $643 73 54 1,150 $800 Tax rate after merger: 35% Cost of goods sold as a percentage of sales: 65% BCC's pre-merger beta: 1.40 Risk-free rate: 6% Market risk premium: 4% Terminal growth rate of free cash flows and ITS: 7% after 2015 If the acquisition is made, it will occur on January 1, 2011. All cash flows shown in the income statements are assumed to occur at the end of the year. BCC currently has a capital structure of 40% debt, which costs 10%, but over the next 4 years VolWorld would increase that to 50%. The target capital structure would be reached at the start of 2015. BCC, if independent, would pay taxes at 20%, but its income would be taxed at 35% if it were consolidated. 1. What is the unlevered cost of equity for BCC? 2. What are the free cash flows and interest tax shields for the first 5 years? 3. What are BCC's horizon value of interest tax shield and unlevered horizon value? 4. What is the value of BCC's equity to VolWorld's shareholders if BCC has $300,000 in debt outstanding now