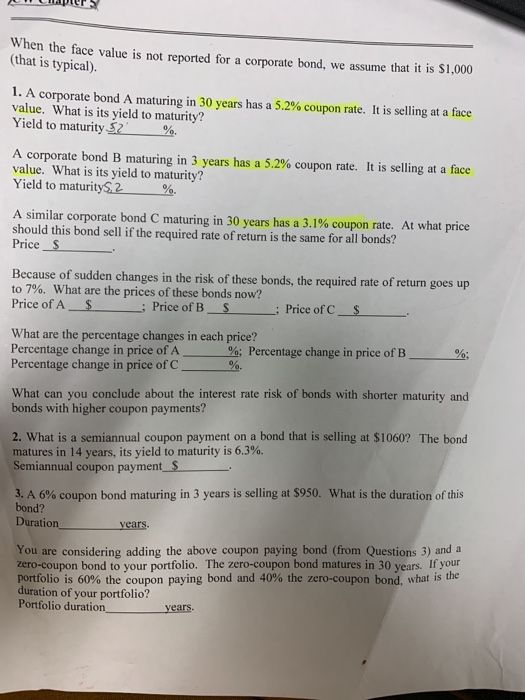

W piers en the face value is not reported for a corporate bond, we assume that it is $1,000 (that is typical). 1. A corporate bond A maturing in 30 years has a 5.2% coupon rate. It is selling at a face value. What is its yield to maturity? Yield to maturity $2 %. A corporate bond B maturing in 3 years has a 5.2% coupon rate. It is selling at a face value. What is its yield to maturity? Yield to maturity5.2 %. A similar corporate bond C maturing in 30 years has a 3.1% coupon rate. At what price should this bond sell if the required rate of return is the same for all bonds? Price $ Because of sudden changes in the risk of these bonds, the required rate of return goes up to 7%. What are the prices of these bonds now? Price of A $ ; Price of B_S : Price of C_ $ What are the percentage changes in each price? Percentage change in price of A_ %: Percentage change in price of B. Percentage change in price of C %; What can you conclude about the interest rate risk of bonds with shorter maturity and bonds with higher coupon payments? 2. What is a semiannual coupon payment on a bond that is selling at $1060? The bond matures in 14 years, its yield to maturity is 6.3%. Semiannual coupon payment_$ 3. A 6% coupon bond maturing in 3 years is selling at $950. What is the duration of this bond? Duration years. You are considering adding the above coupon paying bond (from Questions 3) and a 10-coupon bond to your portfolio. The zero-coupon bond matures in 30 ore If your portfolio is 60% the coupon paying bond and 40% the zero-coupon bond, what is the duration of your portfolio? Portfolio duration years. W piers en the face value is not reported for a corporate bond, we assume that it is $1,000 (that is typical). 1. A corporate bond A maturing in 30 years has a 5.2% coupon rate. It is selling at a face value. What is its yield to maturity? Yield to maturity $2 %. A corporate bond B maturing in 3 years has a 5.2% coupon rate. It is selling at a face value. What is its yield to maturity? Yield to maturity5.2 %. A similar corporate bond C maturing in 30 years has a 3.1% coupon rate. At what price should this bond sell if the required rate of return is the same for all bonds? Price $ Because of sudden changes in the risk of these bonds, the required rate of return goes up to 7%. What are the prices of these bonds now? Price of A $ ; Price of B_S : Price of C_ $ What are the percentage changes in each price? Percentage change in price of A_ %: Percentage change in price of B. Percentage change in price of C %; What can you conclude about the interest rate risk of bonds with shorter maturity and bonds with higher coupon payments? 2. What is a semiannual coupon payment on a bond that is selling at $1060? The bond matures in 14 years, its yield to maturity is 6.3%. Semiannual coupon payment_$ 3. A 6% coupon bond maturing in 3 years is selling at $950. What is the duration of this bond? Duration years. You are considering adding the above coupon paying bond (from Questions 3) and a 10-coupon bond to your portfolio. The zero-coupon bond matures in 30 ore If your portfolio is 60% the coupon paying bond and 40% the zero-coupon bond, what is the duration of your portfolio? Portfolio duration years