Answered step by step

Verified Expert Solution

Question

1 Approved Answer

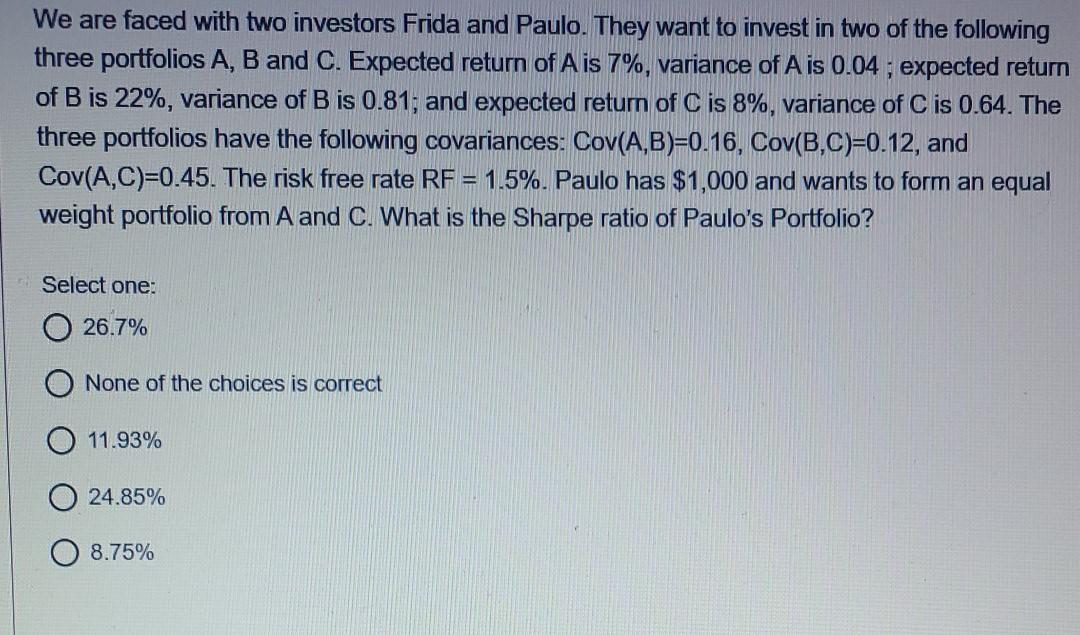

We are faced with two investors Frida and Paulo. They want to invest in two of the following three portfolios A, B and C. Expected

We are faced with two investors Frida and Paulo. They want to invest in two of the following three portfolios A, B and C. Expected return of Ais 7%, variance of Ais 0.04 ; expected return of B is 22%, variance of B is 0.81; and expected return of C is 8%, variance of C is 0.64. The three portfolios have the following covariances: Cov(A,B)=0.16, Cov(B,C)=0.12, and Cov(A,C)=0.45. The risk free rate RF = 1.5%. Paulo has $1,000 and wants to form an equal weight portfolio from A and C. What is the Sharpe ratio of Paulo's Portfolio? Select one: 26.7% None of the choices is correct 11.93% 0 24.85% 8.75%

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Management In Construction Contracting

Authors: Andrew Ross, Peter Williams

1st Edition

1405125063, 9781405125062